This note was originally published at 8am on November 18, 2013 for Hedgeye subscribers.

“If we’re in a bubble, it’s the weirdest bubble I have ever seen, where everybody hates everything.”

-Mark Andreesen

From both a US economic growth and stock market perspective (not one and the same thing), there was a lot of truth in Andreesen’s general statement – if he said it precisely a year ago (he said it on May 1, 2012 with the SP500 at 1406).

A full year ago today, the US economy was tracking 0.14% in the 4th quarter of 2012, US Treasury Yields were a full 100 basis points lower (10yr = 1.70%, all-time lows), and the SP500 was at 1360. So if you bought what everyone hated (growth), and shorted what everyone was clinging too (Gold and Bonds), you crushed it.

Does that make today a bubble? Or was there a bubble back then in fear? Up +32.2% from November 16th, 2012 is the SP500 a bubble? Barrons says “Yes” (in a few names), but “No” (in most names)” and our new central planning diva, Janet Yellen, says “No” (anywhere)… So I’ll agree with Andreesen - there are plenty of weird bubbles; some of the weirdest markets have ever seen.

Back to the Global Macro Grind…

Most pundits and politicians who have never forewarned you of a bubble live in their own conflicted and compromised bubble. Most “market-equilibrium” people think bubbles are measured by “valuation.” And most market-practitioners call bubbles things that start to make lower-highs versus their all-time highs in price.

Well, maybe not most market-practitioners. But that’s how this one thinks. And yes, I’m perfectly happy to be in my own little bubble as a write about bubbles from my hotel room on the Santa Monica, California coastline this morning!

At the end of the day, calling something that’s up a “bubble” is about as useful as having another leg in a one-legged butt kicking contest. If you are going to run around trying to make news calling things bubbles, you better be short them, publicly, with timestamps.

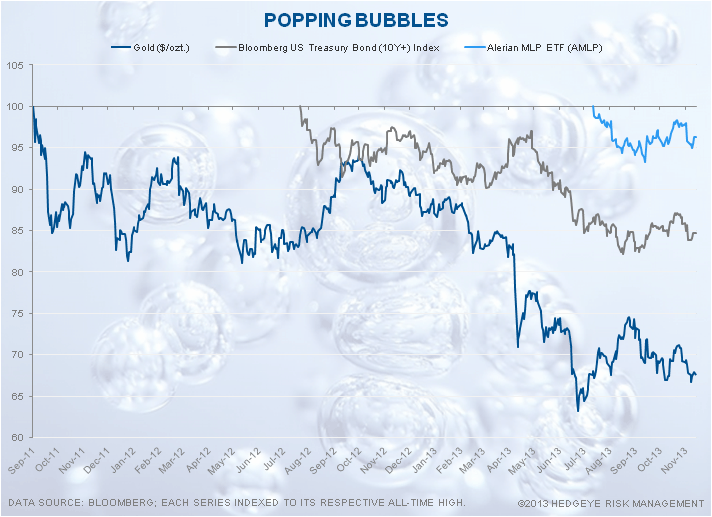

To review what we have been calling the Bernanke Bubbles for the last year:

- Gold

- Bonds

- MLPs

MLPs are master limited partnerships. If you don’t know what those are, don’t worry about it. We’ll boil it down for you – they are the sub-asset class of equities that look most like a bond that slow-growth Yield Chasing investors have found tax refuge in.

All 3 of these bubbles have 3 things in common:

- They had almost bullet proof storytelling narratives that lasted on the order of 1-3 decades

- Their asset prices confirmed the storytelling (making higher-highs) until they all topped in 2011-2012

- They’re now all making a series of lower-highs as interest rates make a series of higher-lows

Now, as you all know, all-time is a long time. So this concept of US 10yr Treasury Bond Yields making an all-time low when US Growth expectations were bottoming in November 2012 can make for some exciting causal relationships.

The relationship between interest rates and 0%-rates-forever-bubbles isn’t weird at all. It makes perfect sense. That’s why the upside down of repressed growth expectations (US Growth Stocks) have bubbled up to bring the US stock market to all-time highs:

From a US stock market “Style Factor” perspective, check out the score:

- LOW YIELD (i.e. GROWTH) stocks = +40.4% YTD

- Top 25% EPS GROWERS (by SP500 quartile) = +37.2% YTD

- HIGH BETA stocks = +35.8% YTD

As my boy Jesse Pinkman would say, that growth stuff is “awesome!”

At the same time, the slow-growth-end-of-the-world-fear trade score for 2013 YTD is:

- US Equity Volatility Fear Index (VIX) = crashing -32.4% YTD

- Gold = crashing -23.6% YTD

- UST 10yr Bonds Yields = +54% YTD

In other words, there was this Weird Bubble in fear-mongering that consensus got sucked into last year that popped as everyone trying to call the top in a said “US stock market bubble” ended up being a bubble themselves.

US stock market bears hate that. Another way to measure their “hate” is how well short-interest has performed in 2013. As a “Style Factor”, High Short Interest stocks in the SP500 are currently +31.8% YTD, outperforming the SP500 by +570 basis points.

And that’s why I’ve been so quick to cover “growth” shorts throughout October. Holding the bag on a bubble of fear isn’t exactly how I roll. Neither is holding onto the long side of bubbles (like Gold and Bonds) that are still very much in crash mode.

My holding period on Gold was 72 hours. And I’m not going to apologize for that. I had my catalyst (Yellen being who she is) and I booked that small gain on the event day. I cut my “crazy eights” exposure to both US stocks and bonds in half on that too.

Bubble or no bubble. Weird or not weird. Mr. Macro Market couldn’t care less what we think about markets. He is designed to punish the largest amount of people (consensus) at the most inopportune time. So #GetActive out there, and keep moving.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.66-2.81%

SPX 1773-1803

VIX 11.91-14.35

USD 80.54-81.39

Brent 106.04-108.69

Gold 1260-1308

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer