With a good majority of consumer staples companies having reported their quarterly results, below we give a round-up of our highest conviction ideas on the long and short sides over the intermediate term TREND.

Looking back at the quarter it’s interesting to note that while some things changed versus Q2 most remained the same. Here’s our update:

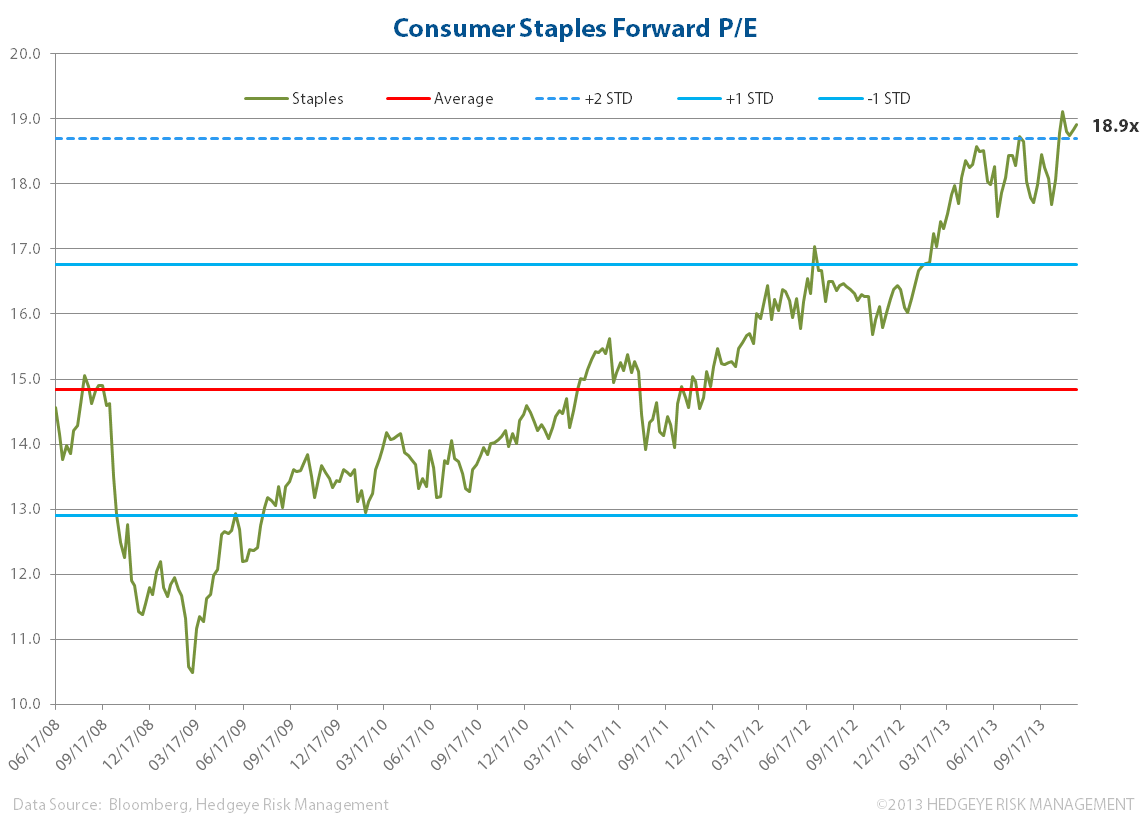

- Valuation remained elevated: the Consumer Staples sector remains richly valued, with P/E at 18.9x, or two standard deviations above the five year mean of just under 15x (see valuation charts below).

- The Fed’s Easy Policy: the reversal of our Q3 Theme call of #RatesRising has encouraged investment back into the yield chasing Consumer Staples sector. We expect this development to continue into the remaining weeks of the year and into the beginning of next year. From our purview, we expect Yellen to remain the ueber dove on policy and push out any QE taper expectations to at least late in Q1 2014.

- The Macro Is Still Impactful: food and beverage companies such as KO, KRFT, K, and GIS (to name a few), continued to site a challenged macro environment, be it continued weakness in Southern Europe and slower growth in the emerging market (China and Brazil in particular). Spirits and tobacco companies have cited lower demand due to a hangover of weaker economic and consumer confidence across geographies.

- Policy Impacts: looking at the spirits companies, for example, China recently banned public funded gift giving during/for the Chinese New Year. This stands to greatly impact companies like Remy, Pernod, DEO, and LVMH. For tobacco companies with international exposure we continue to hear how excise tax hikes will erode future earnings. PM cited weakness due to such hikes in the Philippines and Russia in particular. CCE has also long been a company to cite the impact of French excise tax hikes (and as a crutch to broader demand weakness).

- Organic Is the Growth: for yet another quarter we remain interested in investing behind higher growth organic companies. BNNY is included in our high conviction long list below, and we like the prospects of HAIN and Boulder Brands (BDBD), at a price, as a play to the evolving organic (and gluten-free) movement.

- M&A Speculation Continues: interestingly there’s been no new news around PEP and MDLZ since the noisier activism witnessed last quarter.

- Revenue Misses: of the Consumer Staples companies in the S&P500 that have reported results, on revenue just 15 Beat and 23 Missed, or 39% beat, which is tied with Materials for the worst performance of the 9 S&P500 sectors). On EPS, 26 Beat and 12 Missed, or 68% beat, putting Consumer Staples at the mid to lower range of the pack. In fact, Consumer Staples underperformed the broad S&P500 (revenues beat 54%, and EPS beat 75%).

As a point of reference, directly below we’ve included the price performance of our highest conviction stocks following last quarter’s reported results (Q2). The price performance is somewhat arbitrary, as the entry price reflects the date of this report’s release last quarter (8/14/13) and not our specific entry point targets (the closing reports are based on yesterday’s close), however the numbers provide a reference point for our calls.

Q2 Top Longs: LO (43.52 – 51.54, +18.4%), HSY (96.09 – 97.72, +1.7%), TSN (31.80 – 31.65, -0.5%), SAM (211.70 – 246.20, +16.3%)

Q2 Top Shorts: PM (88.18 – 85.50, +3.0%), DPS (45.86 – 48.47, -5.7%), CCE (38.37 – 42.16, -9.9%), K (65.42 – 60.88, +6.9%), KMB (96.78 – 108.22, -11.8%)

Highest Conviction Stocks Following Reported Q3 2013 Results

Long Ideas

- LO – we expect Lorillard to continue to see outperformance on strong demand for its full-flavored offerings and dominate share of menthol, both contributing to volume outperformance versus the industry (in the quarter LO’s +3.5% versus industry’s avg. -4%). Gross profit margins improved 80bps to 37.1% in the quarter as domestic retail share of the menthol market reached 40.4%, an increase of 0.8 share points versus the prior-year quarter, and the company rolled out Newport Gold, a non-menthol compliment to Red in the quarter. Electronic cigarettes continue to garner huge interest from the investor community. Despite only representing ~ 1% of the portfolio, LO was the first Big Tobacco company to market with Blu in April 2012, and in the quarter took leading market share from 40% to 49%! Further, the company became an international e-cig dealer through its purchase of UK-based SKYCIG in October 2013.

- SAM – it’s hard to argue with Boston Beer’s results. We remain committed to this stock, but are closely managing its up-on-a-rope price level (up +17% since we published a similar note highlighting our bullish conviction on SAM last quarter). The company ever so slightly lowered its FY 2013 guidance range by 5 cents in the quarter to $5.05 – $5.35, and we see good runway in 2014 on balanced comps, continued support from Twisted Tea and Angry Orchard, and broad interest in the craft segment, in which SAM continues to be a favored, recognized brand. We expect the company’s increased cap-ex spend to build brewery capacity (including a new bottling and can line, announced last quarter) to boost 2014 shipping volumes and reverse recent bottle necks resulting from overcapacity and the higher costs associated with using third party breweries.

- HSY – Hershey’s reported another strong quarter, furthering our bullish outlook on the stock since last quarter, through solid core brand performance with momentum building going into the holiday season. Net sales were driven squarely by volume (Volume +6.1%; Net Price +0.5%; FX -0.5%) in the quarter. Similar to SAM, we’re bullish on its intermediate to longer term strategy to build to grow: it announced plans to invest $250MM in cap-ex to build a new plant in Malaysia (to supply markets in Asia and assist existing capacity in China). Heading into year-end, the company reiterated its expectations for FY 2013 net sales of 7%, with no change to the input cost outlook, revised up its FY Gross Margins expectations to 240 to 250 bps vs a previous estimate of 220 to 230, and said it sees a more favorable tax rate and earlier Chinese New Year offsetting an increased marketing spend in Q4. We’re bullish on HSY’s performance across retail channels and its determination to grow its international business, in particular China to its second largest business, and believe the additional cap-ex spend will allow it to enhance its manufacturing scale in China (currently it has a manufacturing JV facility) and across Asia.

- BNNY – the company reported strong top and bottom line fiscal Q2 2014 results, yet saw some gross margin pressure from frozen pizza results. Despite some unevenness in the quarter we remain bullish on the company as its 2H outlook stands to benefit from product roll-out, COGS and SG&A efficiencies, including from its acquisition of Safeway’s manufacturing plant in Missouri, where the company has been producing over 50% of its snacks business since inception in 2002 (again, spending to grow similar to SAM and HSY). Over recent weeks the stock saw underperformance around a CFO shake-up and a secondary offering of 2.5MM common stock shares. We however remain long term bulls on Annie’s based on the company’s advantaged organic portfolio, strong retail positioning for growth, and easier top line and gross margin comparisons going into the back half of its fiscal year.

Short Ideas

- PM – Philip Morris’s headwinds are a continuation of last quarter’s: FX hits, large volume declines (-5.7%, a deceleration vs last quarter’s -3.9% and underperformance vs the industry) on weakness in core geographies (including the EU down -7% to -8% in 2014), increased excise taxes in key geographies like Russia (hit to volume est. -9% to -11%) and the Philippines (no guidance, could be larger than Russia), and an uptick in illicit trade. The company announced plans to accelerate the launch of an electronic cigarette to mid-2014 versus previous guidance of 2016/7. While we applaud PM’s desire to keep up with its peers in the e-cig category (which as mentioned has captured huge investor attention) but it comes at an incremental $100MM price tag, which could also drag on results. For now, for the third straight quarter this year the company revised down its FY EPS guidance, to $5.35-5.40 vs prior guidance of $5.43-5.53.

- CPB – Are you into catching falling knives? The stock is down over -18% since its summer high of $48. In our minds CPB has failed to turn around its portfolio since it offered up big restructuring plans at CAGNY in FEB 2012, however the stock wouldn’t tell such a negative story over this period. Management lowered its 2014 FY guidance in the quarter; we expect US Simple Meals and US Beverages to continue to underperform expectations next quarter, and margins to be hit as CPB plans to increase its marketing spend and accelerate the launch of 8 new products. We see more difficult comps ahead and no clearance on the value proposition of its strategy to offer more premium soups given a still strapped U.S. and global consumer. We think there’s more room to run on the short side.

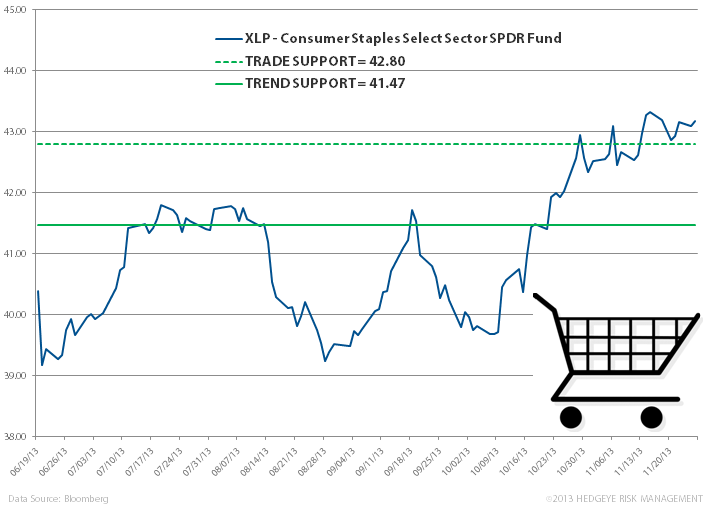

Our quantitative real-time set-up for Consumer Staples (etf: XLP) is bullish, trading above its intermediate term TREND line.

Matthew Hedrick

Associate