Happy Thanksgiving! You never know, as you dive into your second helping of mashed potatoes and gravy, the topic at the table could well be electronic cigarettes!

Below we want to provide recent updates and developments in the category. In our work we continue to express great excitement in the growth prospects for the e-cigs, despite its current diminutive size (~ 1% of the tobacco market). That said, we expect consumer interest in and investment behind e-cigs to grow, especially following “Big Tobacco’s” entrance into the category. We think innovation will be a critical component to drive trial and adoption, as improvements in the form, function, and performance of next generation e-cigs meet the combustible cigarette experience. However, with respect to innovation, and the broader size and shape of the category, much depends on the details of pending regulation from the FDA (more below).

In terms of excitement and interest in the category, just last week Wells Fargo and Morgan Stanley held the first annual e-cig industry conferences, in which both management teams from Big Tobacco and select private manufacturers were featured, including NJOY, Victory, and Ballantyne Brands, which we’ve held conferences calls with in recent months. We believe the interest in this new disruptive category is built on:

- A “reasonable person’s” belief that e-cigs are less harmful than traditional combustible cigarettes.

- Attractiveness as a mimic to smoking behavior (hand-to-mouth) with step-down levels of nicotine, and currently priced at a discount to traditional cigs.

- E-cigs are a bridge to meet changing consumer desires (the consumption of healthier products and social awareness of the stigma of cigarette smoking).

- Estimates for the e-cig category to double in the U.S. in the years ahead, from sales of $150MM in 2011, $500MM in 2012 ($300MM across retail channels and $200MM over the internet), and estimates of around $1-2B in 2013.

- A huge runway of smokers (more than 40MM in the U.S.).

- A giant global opportunity (the global tobacco industry is worth $800B annually).

- Big Tobacco’s desire to make up for declining volume trends of traditional cigarettes

We expect that these factors will encourage investors to overweight e-cig results in gauging broader company performance as we look out to the coming quarters.

Investment Position: Our preferred Big Tobacco play remains Lorillard (LO), given its leading share in the e-cig category (~50%) and advantaged cigarette portfolio. We expect LO to continue to see outperformance on strong demand for its full-flavored offerings and dominate share of menthol (~85% of its portfolio), both of which are contributing to volume outperformance versus the industry (in the quarter LO’s vol. +3.5% versus industry’s avg. -4%). The company continues to push gross profit margins higher, improving 80bps to 37.1% in the quarter as domestic retail share of menthol rose.

LO was the first Big Tobacco company to market through the acquisition of “Blu” branded e-cigs (in April 2012 for $135MM) and saw strong sales growth of 11% quarter-over-quarter (+350% year-over-year) to $63MM. LO CEO Murray Kessler’s e-cig strategy appears to forgo short-term profits for long term gains: he sold e-cigs at break-even in the quarter and was able to boost Blu’s market share to 49% from 40% last quarter. We expect similar trends as LO tries to capture brand loyalty. Over time, we do think that e-cigs can be margin-enhancing to the combined cigarette category. Further, the company became an international e-cig dealer through its purchase of UK-based SKYCIG in October 2013 for £30MM in cash, plus an additional £30MM to be paid in 2016 based on the achievement of certain financial benchmarks. SKYCIG is a three year old company with ~ 300,000 users in the UK (there exists around ~ 10MM smokers in the country) that also happens to have nearly identical branding to Blu.

A Changing Marketplace

- Big Tobacco Is All In – Altria (MO) and Reynolds American (RAI) issued their own e-cig in Q3 of this year, under the brands MarkTen and VUSE, respectively, each in individual test-state markets. Both have plans for national distribution – targeting mid 2014 – and both are competing with Lorillard (LO) and its e-cig brand Blu that currently has national distribution and number one market share.

- Philip Morris (PM) announced last week that it is accelerating its launch of an e-cig product to mid-2014, instead of a previous target of 2016/17, at a cost of $100MM.

- We think Big Tobacco’s entry into the e-cig market lends credibility to the category, and should spur innovation and promote good manufacturing practices along with a handful of select private companies (such as NJOY, Mistic, Krave, Victory, Fin, Logic) that stand to strongly compete with Big Tobacco for category share.

- We believe that the prospect for regulation on the industry equates to Big Tobacco’s advantage, with its deep pockets, retail distribution, and strong manufacturing practices. We would expect some consolidation from the current large and fragmented group of nearly 2000 smaller e-cig U.S. manufacturers.

- Given RAI and MO’s entrance (with PM around the corner), we wouldn’t be surprised to see price wars, especially for rechargeables, to heat up, as the category is still in its infancy and manufacturers look to solidify brand loyalty. This would be negative for profit in the short term. We’d expect more rational pricing in forward years.

Regulatory Uncertainty

- It’s anyone’s guess when a regulatory announcement on e-cigs may come. Expectations were last set for an October announcement (then came the government shutdown) – the industry seems to guess now that one will come before year-end.

- We think that industry is bracing for regulation that could include: 1) ban of online commerce, 2) age verification standards at retail, 3) flavor limitations (beyond tobacco and menthol), 4) health/safety certifications, and 5) labeling and marketing requirements.

- A higher bar, which the industry broadly seems to characterize as “the wrong regulation” could include limits to innovation by mandating premarket approval requirements, tax raises on e-cigs, and in NJOY’s case, very vocal remarks against mandatory shelving to the back counter and the prohibition of TV advertising.

- The industry is cautiously optimistic around recent statements from Mitch Zeller, the new Director of the Center for Tobacco Products, in which he said that the agency will be giving a high priority to developing a more comprehensive approach to the regulation of nicotine-containing products, which will be based on the continuum of risk.

- Zeller’s words, including the phrase “continuum of risk”, hint that the FDA may consider e-cigs (along with non-combustible alternative products such as snus, and nicotine gum and patches) in a separate category from combustible tobacco, which the e-cig industry applauds.

- We expect the FDA to struggle with balancing too little regulation versus too much, fighting for instance PR winds that e-cigs could be a gateway to traditional cigarettes, while recognizing full well the health risks of combustible cigarettes and the opportunity to allow for “healthier” alternatives.

- It is likely the FDA takes longer than a few weeks or months to come up with a summary judgment, yet may call for introductory regulations, as there is no current scientific proof of the long-term safety or risk of e-cigs.

Category Color

- We’re seeing and expect future increased rates of trial and adoption given 1) Big Tobacco’s involvement in the category to bring awareness and credibility to the market and 2) increased innovation given Big Tobacco’s involvement and a strong group of private players competing for share.

- Talk around innovation and “Next Generation Products” includes everything from puff counters and LED light indicators to signal battery strength and nicotine supply, to improvements on form, function, and design in getting the e-cig experience in-line with a traditional cigarette.

- We continue to see e-cig manufacturers favor the razor-razorblade model of a rechargeable unit and replacement cartridges to that of disposable e-cigs (NJOY is one big exception among major distributors in only selling disposables), with expectations that rechargables will be higher margin than disposables.

- We’ve heard a number of manufacturers quote gross margins for rechargables in the 40-50% range and well above traditional cigarettes around 13%-15%.

- The higher margin opportunities in e-cigs versus traditional, especially if partially passed onto to retailers, should also help to accelerate growth in the category.

- Blu, NJOY, Logic are the leading brands.

- Current trends suggest that disposable sales are strong, and in some cases outpacing rechargables. As an example, Blu states that its current mix is 51% disposables, 23% cartridges, and 26% rechargeable kits.

- Manufacturers are pricing a single disposable roughly between $5.99 to $9.99 and claim the number of puffs is equivalent to 1.5 to 2 packs of traditional cigarettes. [Note: an average pack of cigarettes in the U.S. is $6.00 and in New York City the minimum price for a pack is now $10.50, mandated by Mayor Bloomberg’s newly approved bill that raises the legal age to buy cigarettes to 21 from 18]

- We believe the price discount of e-cigs to cigarettes remains attractive to consumers. Many top manufacturers continue to push the value of rechargables, especially when the discount on a price per replacement cartridge is factored in when buying multi-pack replacement cartridges (versus single replacements or disposables).

- A defining trend within the category is companies’ strategy to broaden retail distribution, often at a lower margin to online, with recognition that the FDA could ban online sales.

Awareness, Adoption and the E-Cig User

- Adoption rates remain quite low despite increases in trialing and awareness throughout the year. However, we expect that to change as the category grows behind Big Tobacco’s involvement and innovative improvements.

- Recently Blu cited that in Q1 2013, 57% of adult smokers had heard of Blu, and by Q3 2013, the number had increased to 82%.

- Companies like LO and NJOY are advertising on television. LO has used celebrities such as Jenny McCarthy and Stephen Dorff to get their messages out. Our concern here is that such high profile advertising may adversely harm the e-cig image in the FDA’s eye. As mentioned above, the FDA could well ban e-cig TV, print, and banner ads as it has with traditional tobacco.

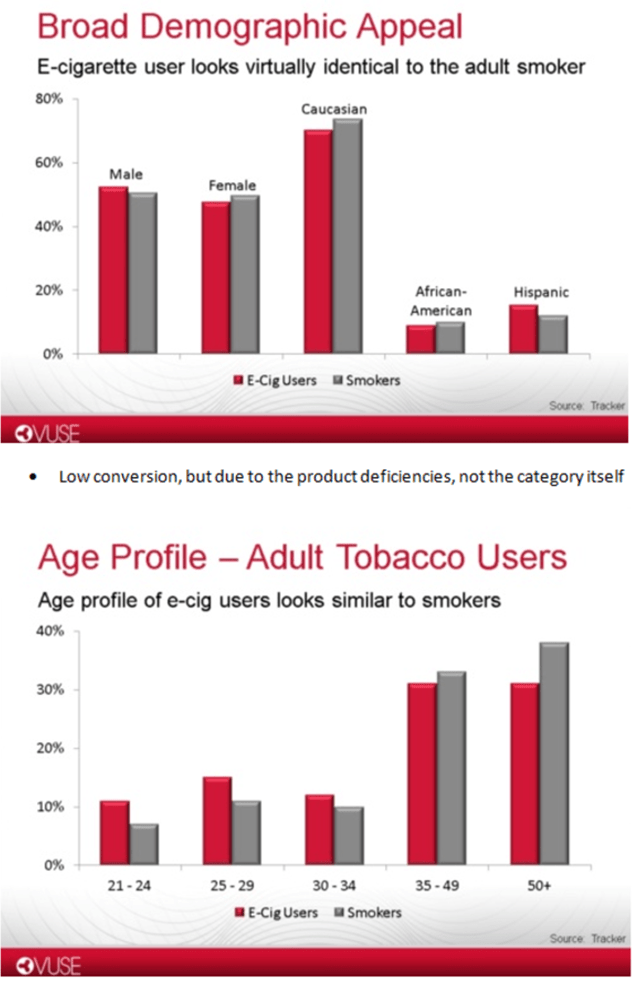

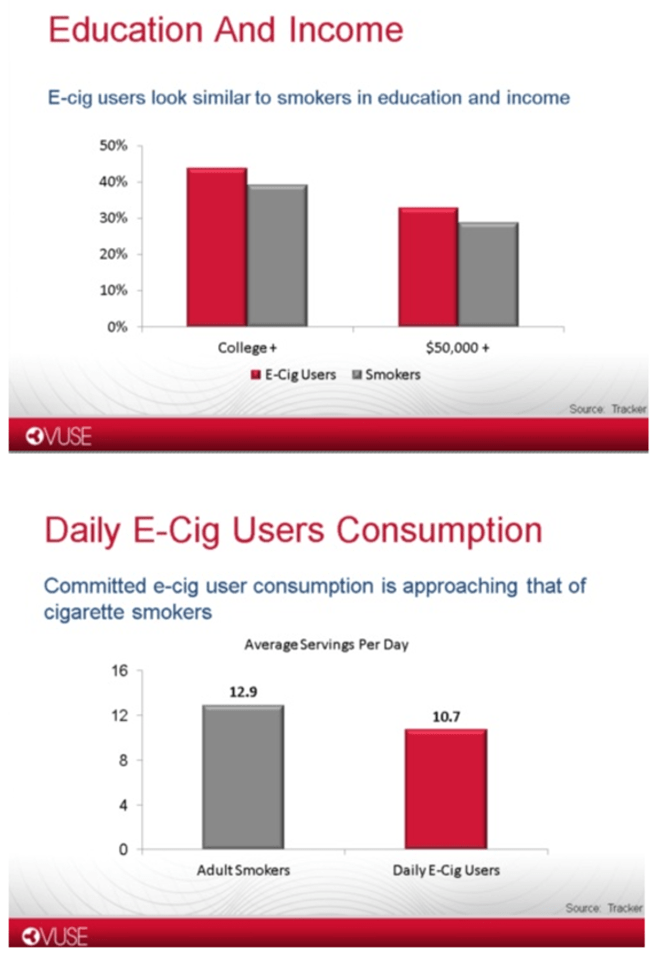

- The charts below from a recent RAI presentation suggest demographic trends are very similar between e-cig users and cigarette smokers.

The Opportunity

- Smoking causes 5-6 million deaths per year and kills over 400,000 in the U.S. each year. Smoking is also the first avoidable cause of death and disease in the U.S. and the second globally. The numbers alone indicate to us that there’s a huge opportunity for products that can lead to harm reduction.

- We think e-cigs demonstrate truly disruptive and compelling innovation because the e-cig so closely mimics smoking behavior.

- We expect that technical performance changes and enhancements of e-cigs, their price discount to traditional, and e-cigs’ perception as a healthier alternative to tobacco will accelerate growth in the category.

- We’re bullish on the U.S. and global runways for the category: the global tobacco market is worth $800B annually. While the industry is subject to the scope of the FDA’s regulation, we believe the category is here to stay.

Vape on!

Matthew Hedrick

Associate