Labor Leads the Long End of the Curve

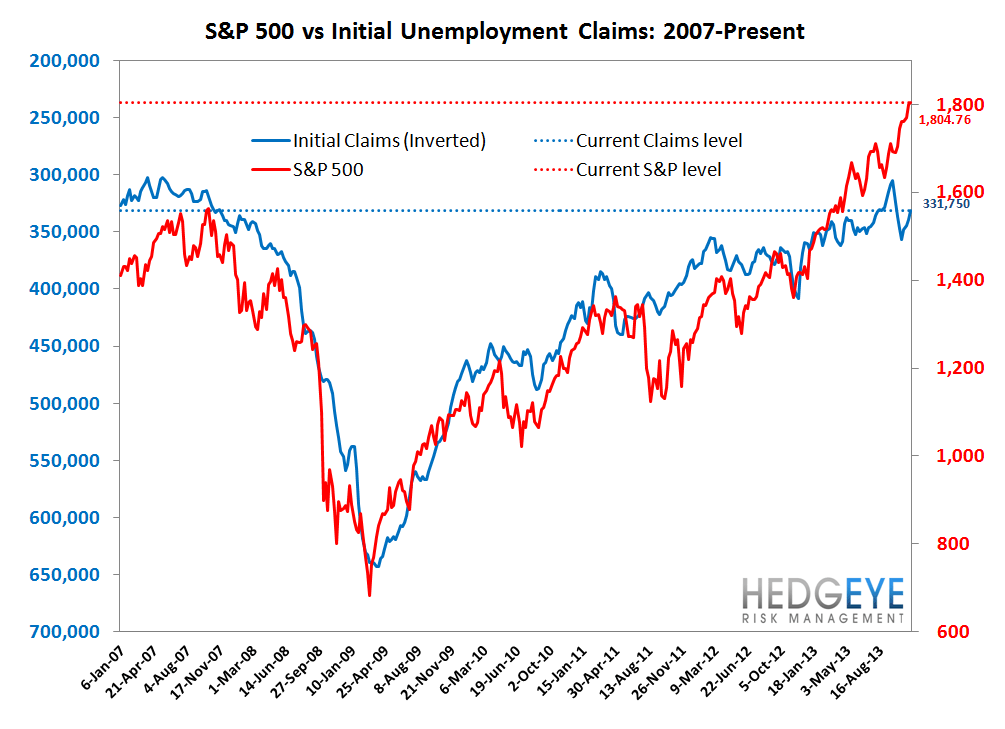

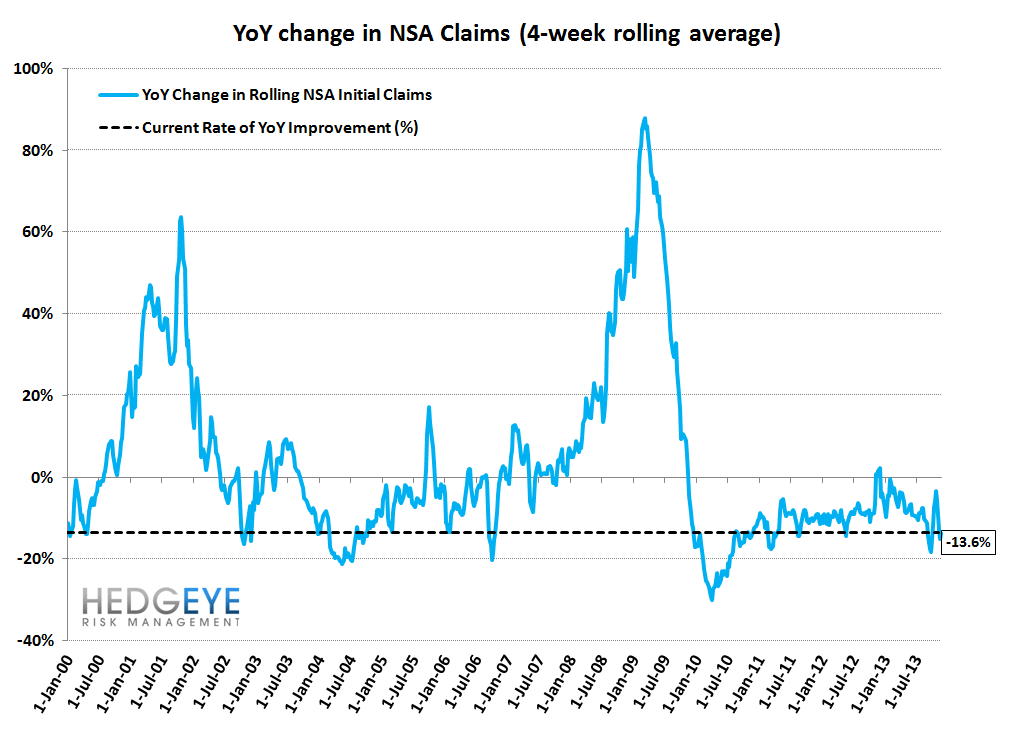

Hurricane Sandy continues to distort the year-over-year trends in the labor market. As such, we are relying on the SA data as well as the 2-year comps on the NSA data. On both fronts, the data is very strong this week. The two-year comp shows claims down by 17.5%, which is the fastest rate of improvement in the last two months. On the seasonally-adjusted data, the headline print of 316,000 marks the third lowest print since the start of the Financial Crisis, and is only 8k shy of the low. By all accounts it would appear that the labor market continues to make steady progress in spite of the naysayers who'll tell you otherwise. Not only is an improving labor market conducive to lower credit costs for Financials, but it also exerts upward pressure on the long end of the yield curve. We showed recently just how correlated the banks are with the 10-year treasury yield, so now you've got both labor and spreads working in tandem to push bank stocks higher. For more details, see our note from 11/22 "#Rates-Rising: A Current Look at Rate Sensitivity Across Financials", a link to which can be found here.

Nuts & Bolts

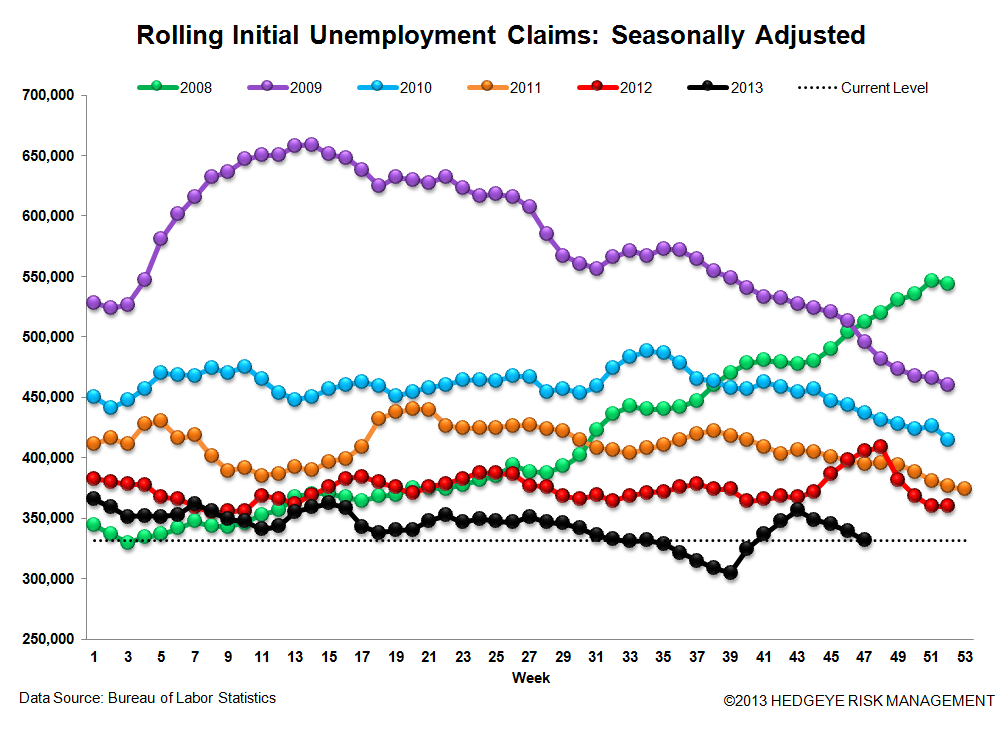

Prior to revision, initial jobless claims fell 7k to 316k from 323k WoW, as the prior week's number was revised up by 3k to 326k.

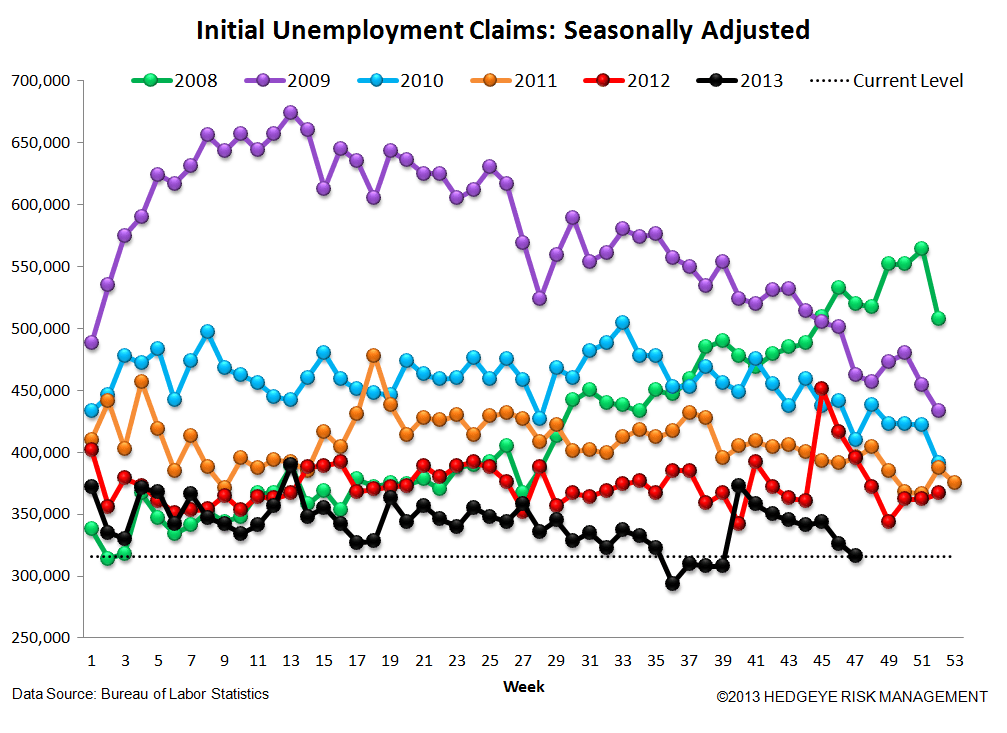

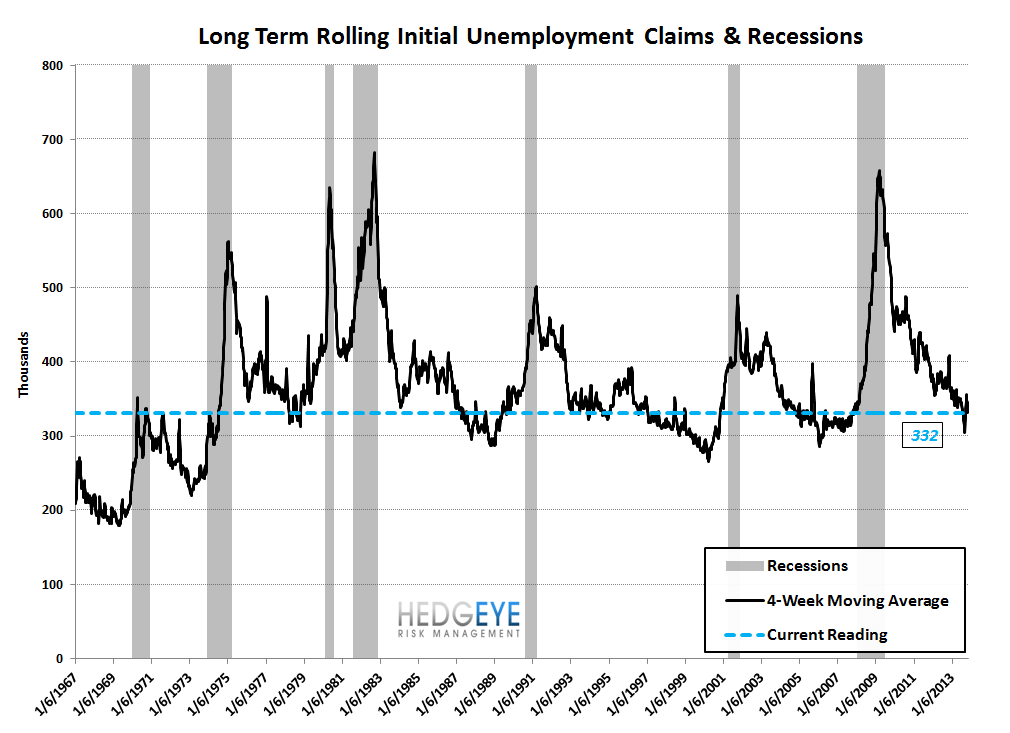

The headline (unrevised) number shows claims were lower by 10k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -7.25k WoW to 331.75k.

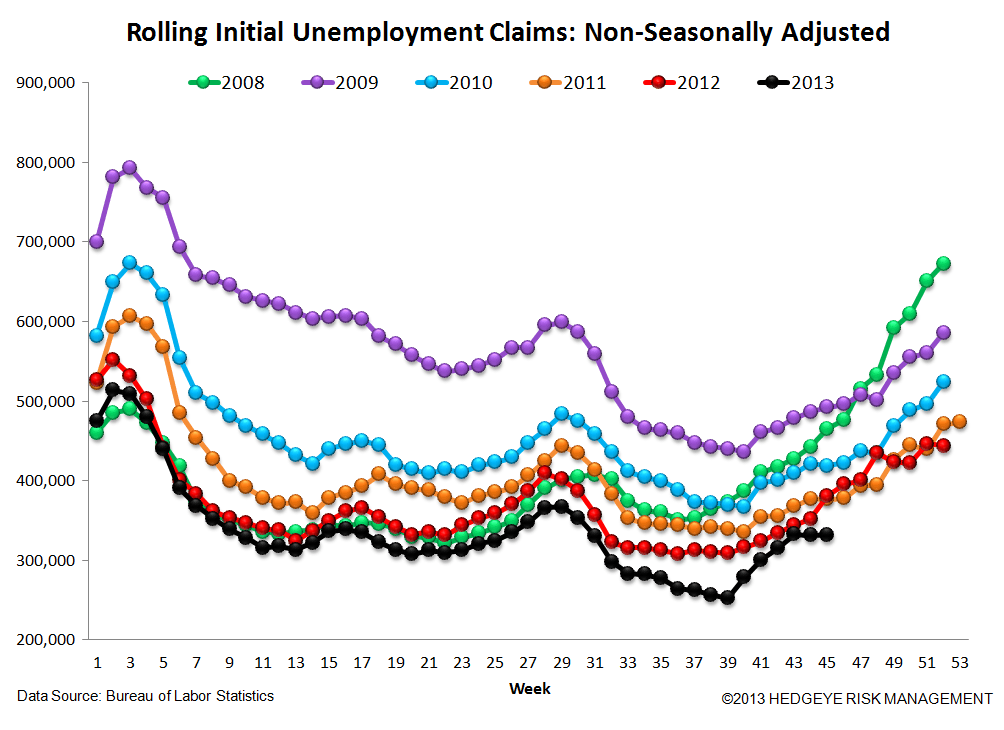

The 4-week rolling average of NSA claims, which we normally consider a more accurate representation of the underlying labor market trend, was -13.6% lower YoY, which is a modest sequential slowdown versus the previous week's YoY change of -15.1%

Yield Spreads

The 2-10 spread rose 1 basis points WoW to 243 bps. 4Q13TD, the 2-10 spread is averaging 233 bps, which is lower by 1 bp relative to 3Q13.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT