This note was originally published at 8am on November 13, 2013 for Hedgeye subscribers.

“The tax on capital gains directly affects investment decisions, the mobility and flow of risk capital . . . the ease or difficulty experienced by new ventures in obtaining capital, and thereby the strength and potential for growth in the economy.” -President John F. Kennedy

As stock and bond market operators, we all know full well that the world is laden with risks. For any investment, there are macro risks, industry risks, and company risks, to name a few. As portfolio managers, there are then the universal risks of timing and sizing, which can be critical to performance and ultimately job risk.

On the macro level, I recently happened upon President Kennedy’s quote above and it made me ponder a risk we actually think about very frequently at Hedgeye – government risk. In this case, Kennedy’s quote refers to the specific issue of taxation and its impact on the economy.

There are some analysts out there who believe a dollar sent to the government is no different than a dollar left in the hands of the consumer or investor. Without getting into politics, hopefully the recent debacle over the website for the affordable care act reinforces this idea that government is inefficient at allocating capital, particularly to new businesses.

Back to the global macro grind...

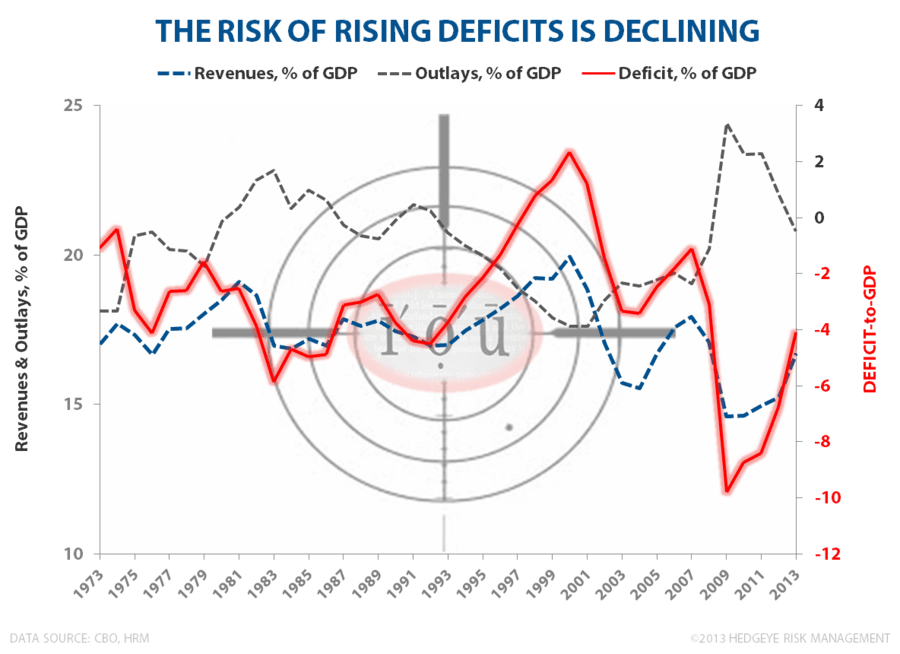

The one government risk that is improving is the risk of rising federal deficits. As we highlight in the Chart of the Day, the federal deficit as a percentage of GDP peaked in fiscal 2009 (Obama’s first year in office) and has declined steadily to -4.1% in this fiscal year ending September 30th. On a notional level, the deficit has declined from -$1.4 trillion in 2009 to -$680 billion in 2013.

Certainly, running an almost $700 billion deficit into the fifth year of a “recovery” is nothing to get overly excited about. But one marginal positive point, which we do need to give our elected officials credit for, is that actual federal government outlays have declined sequentially for the last two years by -1.8% in 2012 and -2.4% in 2013. And, frankly, the obstructionist “Tea Partiers” probably deserve the most credit for this improvement.

From an investing perspective, this decline in deficit is certainly a positive tailwind for the U.S. dollar. It takes off the table certain questions of U.S. credit worthiness and the likelihood of future tax increases, which bode more positively for future GDP growth. As painful as the budget debates have been in the last couple of years, this novel approach of cutting spending and growing the economy has worked.

As quietly as the deficit as improved, the fourth branch of government, the Federal Reserve, appears to be no closer to getting out of the way. Instead of protecting against inflation, as has historically been the case, the Fed now seems overly focused on the omnipresent evil known as: deflation. The top headline on Bloomberg.com this morning says it all:

“Central Banks Risk Asset Bubbles in Battle with Deflation Danger”

The premise that deflation is dangerous resolves largely around the concept that as consumers begin to see that prices are falling they will hold off on purchases in anticipation of lower prices. Secondarily to this is the idea that in an inflationary environment, inflating assets will allow consumers, and the government, to pay off debts quicker.

Call me a simpleton, but personally I’m going to pay off more debts when I have more excess cash flow, not due to lower prices for basic goods (food and energy) or lower taxes. Even if I agreed with the concept of inflation as a way to pay off debts, the broader issue is changing the definition of CPI does not mean deflation exists. In fact, based on the MIT billion prices index, inflation has been solidly at over 2% for most of this year.

The biggest challenge with the ever moving inflation, GDP and employment goal posts of global central banks is that it breeds contempt and confusion, which ultimately leads to increased volatility (we’ve seen this in spades in the interest rate markets this year). The longer term issue of central banks trying to save us from every economic threat known to man is that when we do eventually unwind this extreme policy, it will be excruciatingly painful.

Another challenge of course is that central banks have limited room to stimulate from current levels. As Bridgewater's Ray Dalio recently wrote:

“Because central banks can only buy financial assets, quantitative easing drove up the prices of financial assets and did not have as a broad effect on the economy. The Fed’s ability to stimulate the economy became increasingly reliant on those who experience the increased wealth trickling it down to spending and incomes, which happened in decreasing degrees (for logical reasons, given who owned the assets and their deceasing marginal propensity to consume) . . . the marginal effects of wealth increase on economic activity have been declining significantly.”

In essence, the more central bankers attempt to stimulate from current levels the less and less impact it will have on real economic activity.

Luckily for us, not every central banker in the world wants to pursue an activist strategy and attempt to manage every ebb and flow of the global economy. Fellow Canadian and BoE Governor Mark Carney actually seems rather content to let the improving economy do its thing and not, like his ECB counterparts, double down on easing. As a result, Carney is also raising his 2014 GDP forecast for the United Kingdom to 2.8%. Long the pound remains one of our top macro ideas.

Speaking of activists, it was nice to see Dan Loeb from Third Point show up in one of our Best Ideas, Fed-Ex. The stock is up more than 25% since we added to our Best Ideas list on February 27th of this year and may have more room to run. If you’d like to learn about access to our Industrials Sector and go through our 60 page presentation on Fed-Ex, ping sales@hedgeye.com.

Our immediate-term Risk Ranges are now:

UST 10yr Yield 2.66-2.81% (bullish)

SPX 1748-1778 (bullish)

FTSE 6656-6748 (bullish)

Shanghai Comp 2067-2044 (bearish)

VIX 12.22-14.51 (bearish)

USD 80.85-81.39 (bearish)

Pound 1.58-1.60 (bullish)

Euro 1.33-1.35 (neutral)

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research