TODAY’S S&P 500 SET-UP – November 27, 2013

As we look at today's setup for the S&P 500, the range is 14 points or 0.43% downside to 1795 and 0.35% upside to 1809.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.43 from 2.42

- VIX closed at 12.81 1 day percent change of 0.16%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, Nov. 22 (prior -2.3%)

- 8:30am: Init. Jobless Claims, Nov. 23, est. 330k (pr 323k)

- 8:30am: Durable Goods, Oct., est. -2% (pr 3.7%, rev 3.8%)

- 8:30am: Chicago Fed Natl Activity, Oct., est. 0.1% (pr 0.14)

- 9:45am: Chicago Purch Mgrs Index, Nov., est. 60 (pr 65.9)

- 9:45am: Bloomberg Consumer Comfort, Nov. 24 (prior -34.6)

- 9:55am: U of Mich Conf., Nov. final, est. 73.1 (prior 72)

- 10am: Freddie Mac mortgage rates

- 10am: Index of Leading Eco Ind., Oct., est. 0.0% (pr 0.7%)

- 10:30am: DOE Energy Inventories

- 12pm: EIA natural-gas storage change

- 1pm: Baker Hughes rig count

GOVERNMENT:

- House, Senate not in session

- 10am: Consumer Federation of America, Credit Union Natl Assn event on Holiday Consumer Spending Survey

WHAT TO WATCH:

- Hewlett-Packard sales top ests. on corporate demand

- HP, Whitman lose bid to dismiss investor suit over Autonomy

- Gensler gives Wall Street 2 mos. to meet cross-border policy

- JPMorgan pressured to reveal $13b accord complaint

- Crocs said to discuss investment w/funds including Blackstone

- Japan to issue icing risk warning to JAL on Boeing 787 engine

- Position for volatility on Mon. after Black Fri., Goldman says

- IMF may shift more bailout risk to bondholders, NYT says

- Microsoft’s Skype enters new China JV w/GMF, China Daily says

- Symantec to end struggling data-storage service amid overhaul

- Morgan Stanley hiring in China being probed by DOJ: Reuters

- KKR’s Bis Industries scraps plan for Australian share sale

- ANA, Japan Air fly through new China zone without notice

- German consumer confidence to rise to highest since Aug. 2007

- U.K. economic growth accelerates on investment, homebuilding

EARNINGS:

- Golar LNG (GLNG) Bef-mkt, $0.41

- Golar LNG Partners (GMLP) Bef-mkt, $0.60

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI-Brent Spread Widens for Sixth Day as U.S. Stockpiles Climb

- Zeppelins Seen Hauling Caterpillars to Mine Siberia: Commodities

- China Gold Imports From Hong Kong Rise to 2nd Highest on Record

- Soybeans Reach Two-Month High as Demand Seen for U.S. Supplies

- Copper Rises as Premiums and Stockpiles Indicate Steady Demand

- Rebar Drops on Slowing Demand Ahead of Industrial Profit Data

- Rubber Falls to 2-Week Low as U.S. Confidence Data Weaken Demand

- Codelco Said to Raise Korea Copper Premium to Nine-Year High

- U.S. Oil Glut Seen in 2015 as Export Ban Tested: Energy Markets

- Energy Market at Mercy of Wars, Fed as Year Dawns: 2014 Outlook

- Gold Heading for 2013 Low as Haven Demand Ebbs: Chart of the Day

- Illegal Coal Mines Leave Hundreds Dead in Ukraine’s East: Energy

- China May Delay U.S. Corn Buying as Cargo Held, Shanghai JC Says

- Crude Traders Skeptical Iran Deal Will Bolster Oil Supplies

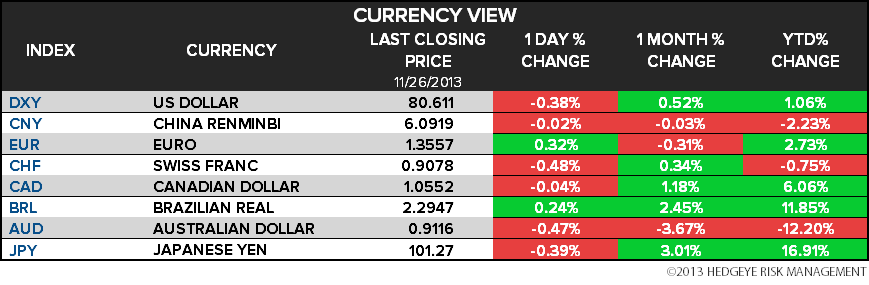

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team