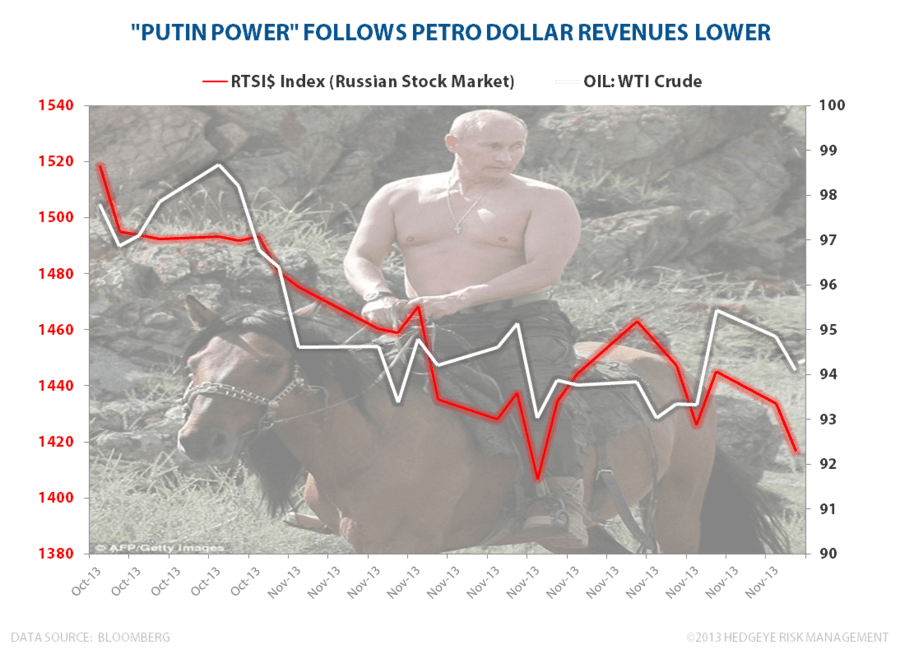

"Putin Power" (or lack thereof) is turning into an interesting story yet again as the price of Oil makes a series of lower-highs and Ukrainians go after the pro-Russia central planning thing.

The Russian stock market leads the losers this morning down -0.8%. Russia is down over -3% year-to-date.

Live by oil, die by oil.

Editor's note: This is a brief excerpt from Hedgeye Research earlier this morning. For more information on how you can subscribe click here.