KEY CALL OUT

Several key International happenings overnight in the apparel/footwear retail industry...but the most notable is added rhetoric out of India on keeping up with recent moves by China to lower VAT (taxes) and/or increase rebates for Indian textile manufacturers in an effort to stimulate both production and exports. This supports one of our key themes headed into 2010, though the interesting twist is that China is largely a footwear play (where 86% of US footwear is manufactured), but with India joining the game, this scales up the impact for apparel as well. Not all will win, as we've been highlighting - and mark my words - some will lose big time. Though this datapoint helps solidify that this is a theme that absolutely can't be ignored. I still think the impact will be far greater than what is currently being quantified (for those that are taking time to do the math).

LEVINE'S LOW DOWN

Some Notable Call Outs

- The streak is over! Monday marked the first day that gas prices declined, reversing a record 54 day streak of increases.

- European M&A following US? Mario Moretti Polegato, through his investment vehicle LIR, has entered into an agreement to acquire Diadora S.p.A. from Geox SpA. Both Polegato and Diadora are based in Italy.

- Furniture makers in Bangladesh on Monday urged the government to withdraw the proposal for increasing VAT on furniture products in the budget for the FY 2009-10 to 15% from 4.5%.

- According to Reliance Retail India, Sr. Executives of Pantaloon Retail India Ltd sounded positive about the business. "Consumer demand has picked up sharply in the last two weeks, and the company has various alternate funding plans to expand its business."

- Bata India, the subsidiary of the Switzerland based Bata Shoes Organization, has appointed Promodome Communications as its creative and media planning and buying partner. The decision follows a multi-agency pitch which saw incumbent creative agency Saatchi & Saatchi and media agency ZenithOptimedia miss the cut. [Note: any short portfolio that tracked changes in consumer products' ad agencies over the ensuing 12-months would have meaningfully outperformed over the past 10 years].

- More weather woes through the weekend. There's no question that by the time June is complete, the weather will have impacted seasonal apparel sales. In particular, the northeast region is now on track to be the coldest in 27 years and one of the wettest June's on record. Couple the weather with the most difficult comparisons we have seen in a year and June is setting up to be a tough month for most retailers. There are little signs of heavy discounting to clear goods at this point, but we expect markdowns to pick up soon the keep inventories clean.

MORNING NEWS

ZachHammer's overview of items you're unlikely to find in the general press.

- Pakistan is set to give its struggling textile industry a major financial boost to aid its ailing textile industry with a policy to be introduced next month that will mirror their regional competitors. China gives a 17% rebate to its textile exports and India gives between 8% and 9%. Pakistan's textile industry needs the support after exports fell by 7% between now and last year. Pakistan is the world's fourth largest producer of cotton, but is only the 12th largest exporter of cotton products. Fifty percent of the country's cotton exports are value-added products, but most are at the lower end of the price spectrum, while the rest is raw cotton, yarn or greige fabric, he noted. <http://www.wwd.com/business-news/china-us-spar-over-trade-2184421?navSection=business-news>

- China's decision to direct stimulus spending toward domestic products first, after months of complaining about a U.S. policy of the same nature, could spell further trouble for trade relations between the two nations as concerns rise about protectionism amid the global economic downturn. China's $587 stimulus packaged has a clause directing spending on domestic goods and services and not imports. China has ridiculed the US since February for encouraging its consumers to buy domestic with the American stimulus package. <http://www.wwd.com/business-news/china-us-spar-over-trade-2184421?navSection=business-news>

- Indian retail companies in the organized retail sector want the government to take a series of initiatives in the forthcoming budget that would boost consumption and have sought 'industry status' as well as abolition of the service tax to beat back the slowdown. Vishal Retail group president Ambeek Khemka said that besides granting industry status to the sector, the government should allow FDI into multi-brand retailing and announce some special sops for the sector. "There should be less restrictions on the retail sector and the government should grant it industry status. It's a very big sector and a major employer," he said. Only a small portion of the retail sector is organized and falls under the purview of local laws. Khemka also said the central service tax should be abolished as it is having a negative impact on the sectors profitability. <http://www.indiaretailing.com/News.aspx?Topic=1&Id=3914>

- Furniture makers Monday urged the government to withdraw the proposal for increasing VAT on furniture products and at the same time recognize furniture production as a manufacturing sector instead of service sector. Chairman of Bangladesh Furniture's Industries Owners Association (BAFIOA) KM Akhtaruzzaman said budget for the FY 2009-10 has proposed 15 per cent VAT replacing existing 4.5. <http://www.firstrain.com>

- Online Brands Turn to Traditional Ads - Kayak is among a handful of online brands, including Zappos.com and Amazon.com, that are now seeking traditional agencies (and offline tactics) to create mass awareness and define more broadly what they do. Zappos and Amazon, for example, are frustrated that many consumers don't know that they sell more than shoes and media content, respectively. And while online efforts, including paid search ads, are part of the answer, they are clearly falling short in the eyes of companies with ambitious growth plans and money to spend.

- In an RFP Zappos issued two weeks ago, the Las Vegas-based company said it was seeking "traditional mass advertising (print, TV, OOH, etc.), online advertising (brand awareness, co-op partnership development), grassroots/word-of-mouth and social media." And this month Amazon launched an online contest to solicit potential TV spots from consumers. <http://www.brandweek.com/bw/content_display/news-and-features/digital/e3i8071e0d9c25cb6b83816760c887651bf>

- Saks Chief Cuts Orders to Avoid Discounts on Stiletto Heels, Men's Suits - Saks Inc., Neiman Marcus Group Inc. and other luxury retailers are reducing orders this year to limit supply and boost profitability. <http://www.bloomberg.com/news/industries/consumer.html>

- The European Confederation of the Footwear Industry named Vito Artioli as president of the organization. Artioli was previously the president of the Italian Footwear Manufacturers' Association. Artioli said he would pursue compulsory labeling for products that come from outside the European Union, investigate into trade practices carried out by China and Vietnam, and work toward geographically expanding the European Confederation of Footwear's membership base. <http://www.wwd.com/footwear-news/european-footwear-organization-names-president-2184261?navSection=footwear-news>

- The ESCADA Group, an international fashion group for women's apparel and accessories, reported a weak first half of the year and a negative outlook ahead. Sales for the first half of the year were down 24% (Europe -27%, North America -31%, and Asia -19%), and down 33% for the second quarter of 2009. Gross profit declined 260 basis points from moderate price adjustments. SG&A declined from cost cuts by 2.4% for 1H 09 and 4% for Q2 09. The company sold the entire PRIMERA segment (comprised of the apriori, BiBA, cavita, and Laurel labels) earlier this year. ESCADA Group cited an OECD economic report that claimed the economic output of their targeted countries would decline by 4.3% this year. ESCADA, a German based company, expects Germany to shrink by 6% in 2009 and destabilization until 2010. ESCADA Group's largest losses come from the US and Russia where consumers are trading down from the luxury good industry. Other events that occurred in 1H 09: appointed a Chief Restructuring Officer, improved the liquidity situation, sold their 40% stake in the fashion distributor Schustermann & Borenstein GmbH, prematurely terminated ESCADA's New York 5th Ave Flagship, and cut jobs and expenses. <http://investor-relations.escada.com/eng/>

- Hong Kong-based global consumer goods exporter Li & Fung Limited is enhancing its supply chain management capabilities with a revolutionary portal to support its extensive supplier network. Provided by ecVision, Li & Fung has deployed a supplier portal that will be used by vendors and internal sourcing teams as they collaborate on global supply chain management and shipment tasks. The web-based, role-based application serves as a common platform to standardize trade and customs documents, consolidate shipment data, and provide a means of collaboration between the vendors and the agents. With its extensive global presence, Li & Fung operates a sourcing network of over 80 offices covering over 40 economies across North America, Europe and Asia. <http://www.fibre2fashion.com/news/textiles-technology-news/newsdetails.aspx?news_id=74059>

- Isaac Mizrahi, known for his products lines ranging from Target to Liz Claiborne, is turning a renovated brownstone in New York into a showcase for his own Isaac Mizrahi New York collection. The 1500-square-foot store, on East 67th Street between Madison and Fifth Avenues, is the designer's first freestanding store and will showcase his accessories, shoes and sportswear. http://vmsd.com/content/mizrahi-open-ny-store

- German shopping center developer Management für Immobilien AG (Mfi-Group) has emerged as a second potential candidate to take over some of the 90 insolvent Karstadt department store doors. But the Essen-based group denied reports it is actively pursuing plans to bid for any of the Karstadt properties. <http://www.wwd.com/business-news/china-us-spar-over-trade-2184421?navSection=business-news>

- Marks & Spencer will start the search for a new chief executive in September, making it likely that executive chairman Sir Stuart Rose will leave the company early next year, according to The Sunday Times. The newspaper reported that M&S had been inundated with calls from headhunters looking to win the search contract to find Rose's replacement. It added that M&S planned to start the search after the summer which was likely to mean Rose was almost certain to leave a year earlier than the previously agreed to 2011. <http://www.drapersonline.com/news/multiples/news/weekend-newspaper-round-up-june-20-21/5003751.article>

- A survey of 1,067 consumers ages 18 to 65 by Chicago-based market research firm Information Resources Inc. found: Seventy percent reduced clothing purchases, with 56 % saying that they will do so in the future, 60% wear clothing multiple times before washings to save on cleaning costs and 30% said they will continue to do so, 82% wash laundry only when they have full loads and 60% plan to keep doing that, and 51% repair clothes by sewing and patching them. <http://www.wwd.com/retail-news/echoes-of-the-great-depression-2184359?navSection=retail-news>

- Kitson is ratcheting up its global footprint with store plans for new units in Tokyo, with the first opening Sept. 6 in the Harajuku area and the second in March 2010 in the high-end Omotesando district. Under a licensing agreement, all of Kitson's stores in Japan are owned and operated by Itochu Corp. Kitson founder Fraser Ross said he is in talks to open boutiques in China, South Korea and Singapore, possibly in the next year. <http://www.wwd.com/retail-news/echoes-of-the-great-depression-2184359?navSection=retail-news>

- Following up on its successful collaboration with "Sesame Street," Boston-based New Balance has partnered with licensing and syndication firm United Media to create a line of co-branded children's sneakers based on the popular comic strip "Peanuts," penned by the late Charles M. Schulz. The launch will hit stores in October and initially feature three versions of New Balance's heritage running shoe, the 574, that bring to life three of "Peanuts'" most popular stories: "It's the Great Pumpkin, Charlie Brown;" "A Charlie Brown Thanksgiving;" and "A Charlie Brown Christmas." All three sneaker styles will be available in infant, preschool and grade-school sizes. Retail prices will range from $38 to $60. <http://www.wwd.com/footwear-news/european-footwear-organization-names-president-2184261?navSection=footwear-news>

- W.L. Gore & Associates, which works with apparel, outerwear and even architectural fabrics announced that footwear will be its focus, aggressively expanding from rugged outdoor footwear into new categories. To do it, the company has partnered not only with the brands it supplies (including The North Face, Nike, New Balance, Ecco, Merrell and Salomon) but with the entire manufacturing chain - and it is seeking to bring its partnership model to more retailers, factories and brands. <http://www.wwd.com/footwear-news/european-footwear-organization-names-president-2184261?navSection=footwear-news>

- German Consumer Confidence Rises for Second Month on Outlook, Price Drop - German consumer confidence rose for a second month as the economic outlook brightened and retreating prices boosted household purchasing power. <http://www.bloomberg.com/news/industries/consumer.html>

- French consumer spending fell by more than expected in May, underlining worries about fragile domestic demand but business morale ticked up in June

- Carrefour Gains Most Since April on Report Costs to Be Cut by $2.8 Billion - Carrefour SA, Europe's largest retailer, rose the most in more than two months in Paris trading after Le Figaro reported that the company is planning annual cost savings of 2 billion euros ($2.8 billion) by 2012. <http://www.bloomberg.com/news/industries/consumer.html>

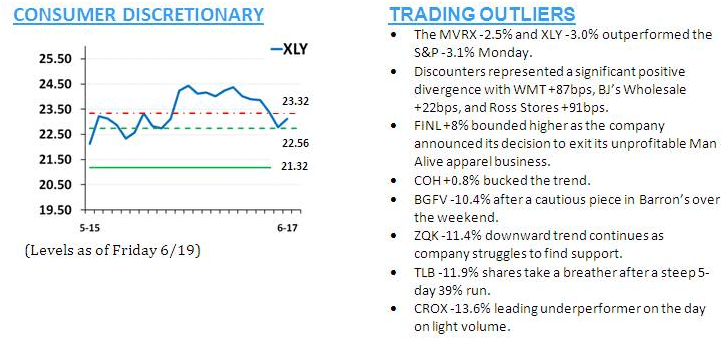

MACRO SECTOR VIEW AND TRADING CALL OUTS

THIS WEEK'S COMPANY CALENDAR: