The broader issue with bond managers like PIMCO is how far afield they have journeyed in search of yield. And therein lies the key question: At what cost does this hunt for yield come?

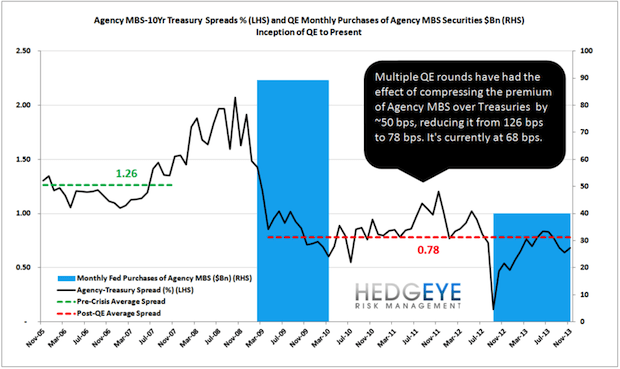

As it relates to the PIMCO Total Return Fund, prospective underperformance may even be more concerning given the fund's holdings and where the managers have gone to find yield. According to analysis by our Financials Team here at Hedgeye, almost 34% of PIMCO Total Returns holdings are in agency Mortgage Backed Securities (MBS). Check out the chart below highlighting the spread of agency MBS to the 10-year Treasury Yield.

Prior to the financial crisis, this spread was around 126 basis points. It has now narrowed to approximately 68 basis points. In other words, the almighty chase for yield has effectively priced mortgage backed securities to one of the lowest levels of risk that we've seen in the asset class. Even if the spread for Agency MBS normalized by just 50 basis points, to pre-crisis levels, it would have a meaningful impact on the market. By our estimation, allowing for modified duration, a 50 basis increase (reversal of tapering for instance) in yield would lead to 5% downside in the Agency MBS market.

Editor's note: This is an excerpt from an article in Fortune written by Daryl Jones, Director of Research at Hedgeye. Click here to read it in its entirety.