KEY POINTS

- Unsustainable business model riddled with different, non-synergistic brands.

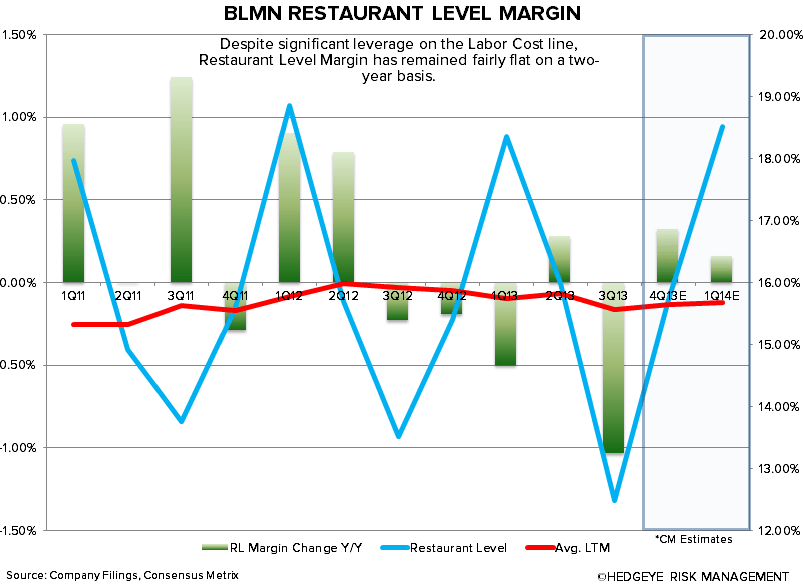

- Restaurant Level Margins are very low, due to an inflated Other Expenses line and, as a result, Operating Margins are low.

- Current same-store sales guidance assumes at least +2% traffic on an annual basis in 2014.

- Expectations for 19% EPS growth in 2014 are aggressive.

- AUV growth for Outback, Carraba’s, and Bonefish is decelerating.

- Adding the lunch time daypart at Outback and Carraba’s has not proven to be successful.

- Outback’s Gap-to-Knapp has been narrowing since 4Q12.

- Outback may be losing share to its closest competitors.

- Bonefish Grill, Bloomin’s growth vehicle, suffered from declining same-store sales and traffic in the most recent quarter.

- Incremental, material G&A cuts from this point are unlikely.

- Trading at an unwarranted, premium valuation.

- Sell-side sentiment is very high.

- We see fair value between $18-$22.

SHORT BLOOMIN' BRANDS

Admittedly, we may be biased against a business model that has proven multiple times that it simply does not work in the casual dining industry – but why wouldn’t we? Bloomin’ Brands is another company that doesn’t make sense to us. Contrary to what management teams like to tell you, the majority of multi-concept structures in the casual dining industry tend to create operational inefficiencies that only worsen over time. As the CFO of EAT, Guy Constant, mentioned several weeks ago on a conference call with our clients, the casual dining industry has evolved and, in our opinion, some companies have been unreceptive to these secular changes. You can listen to a replay of the call here.

In the particular case of Bloomin’, the operating structure of the company lacks cohesiveness and its many brands fail to align in vision and strategy. Over the past year, the company has been the beneficiary of the generous valuations being handed out to casual dining companies. As we wrote a couple of weeks ago, the casual dining industry looks suspiciously like a bubble. What’s concerning is that this bubble has developed despite weak casual dining trends, the recent momentum of fast casual restaurants, and the introduction of premium items at quick service chains.

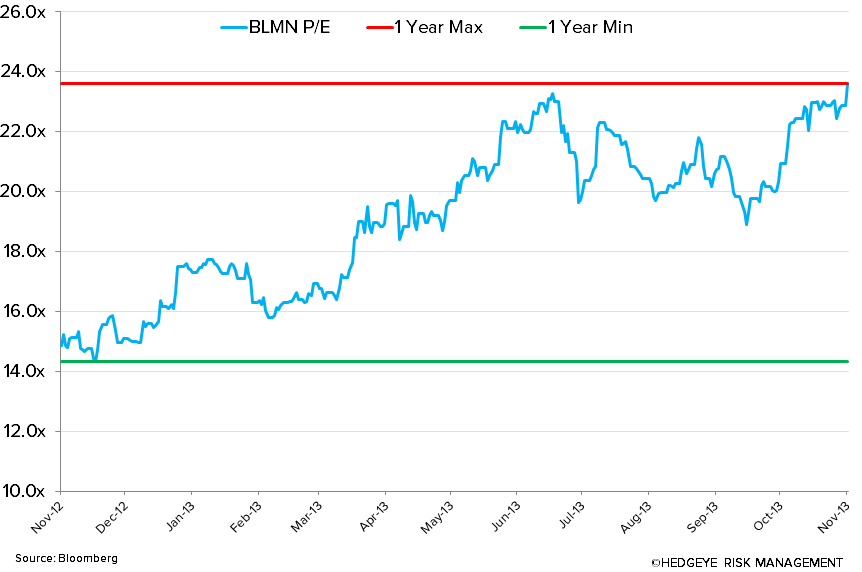

With Bloomin’ currently trading at A P/E of 20.5x and 9.3x EV/EBITDA, we believe the stock more than discounts the potential growth of the company. Given the current demand environment, casual dining companies focused on adding significant capacity are finding it increasingly difficult to generate the incremental returns needed to justify their investments. The street is looking for BLMN to grow EPS by 19% in 2014, despite only managing to grow EPS 12% in 2013. We view this as highly unlikely, and expect this number to be revised down over the coming months.

There are several similarities between BLMN, DRI and the old EAT. In fact, we’d argue that Bloomin’ faces some of the same issues running the company that Brinker experienced five years ago and Darden faces today. To be fair, we constantly ask ourselves what makes BLMN different? Aside from the relative perception of BLMN as a growth company as opposed to a mature company, not much:

The Bloomin’ model has a few aspects to it that simply don’t add up. These became clear during the 3Q13 earnings call:

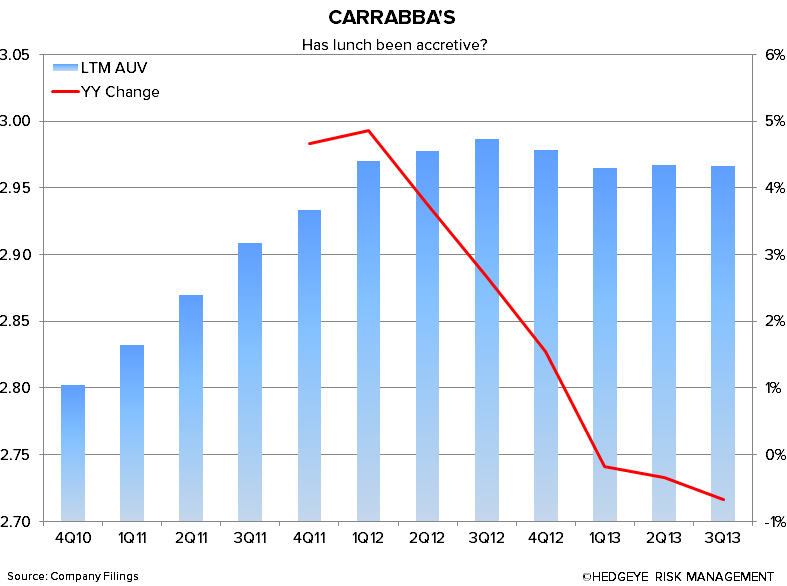

- In 3Q13, the Outback Steakhouse concept missed sales expectations which management immediately attributed to an underperforming LTO. This was a recurring theme throughout the 3Q13 conference call, which marks the first time, since we can remember, that management constantly referred to LTOs. What bothers us is that there is much more to the operational story than promotions. For example, Outback is continuing to roll out weekday lunch which was offered by approximately 26% of stores at the end of Q3. If lunch is driving incremental traffic, then what does that mean for the core dinner business? The two-year average of Outback’s company same-store sales has been in steady decline since peaking in 3Q12.

- According to management, Bonefish Grill is the company’s compelling growth vehicle. We find this rather odd considering same-store sales were down -2.7% during the quarter and are only up 0.4% on a two-year basis. It is not very encouraging when your growth brand is posting declines in traffic and comps. In what quickly became a common theme during the call, management attributed the weakness at Bonefish to a lack of food innovation and an underperforming LTO. Despite “very strong” brand health, management acknowledged that Bonefish is in need of a menu overhaul.

- Cost saving is an integral part of the Bloomin’ bull case, yet the company needed excessive G&A cuts to beat EPS estimates.

All told, there are some holes emerging in the BLMN story. Management appears to be aiming to be “bigger and better” at the same time and capital allocation decisions are unlikely to add shareholder value. That being said, we realize that management has a couple of levers it can pull in the intermediate-term (i.e. debt reduction, international consolidation) that can be accretive to equity holders. Longer-term, however, we believe the business model will struggle, much like every other multi-branded casual dining company we have covered.

We see several other issues that are difficult to overlook:

- Full-year same-store sales guidance assumes at least 2% positive traffic.

- Management publicly announced that a disappointing LTO was the reason for weak comps in Q3, yet they are confident that “Q4 should be the strongest domestic comp of the year.”

- Driving business through LTOs is not a sustainable practice and is a flawed long-term strategy.

The casual dining industry continues to struggle:

- Industry volatility will persist and the segment will continue to be flat, on average, until we see a notable improvement in discretionary income and spending.

- The casual dining industry has become aggressively promotional and value-focused.

- Aside from internal competition and aggressive pricing practices, the industry continues to face external pressure from both fast casual and quick-service companies.

INTERNATIONAL IS A BRIGHT SPOT

Bloomin’ is one of the better positioned restaurant companies internationally, where casual dining is growing. Last quarter, BLMN completed the acquisition of 80% of its Brazilian JV. While Brazil is one of the strongest consumer markets in the world, it is still an emerging market and we caution that it should be viewed as such. According the management, the Brazilian restaurant AUVs are double the domestic locations and they believe the business abroad can double to 100 restaurants over the next five years. This acquisition will be accretive to EBITDA, but it is not enough, in itself, to support the bull case.

OVER TIME, COMPANIES WITH A DIVERSE PORTFOLIO OF BRANDS UNDERPERFORM

There has never been a successful casual dining company that attempted to manage a large, diverse portfolio of brands. In our opinion, BLMN is no exception.

Quite frankly, some of management’s recent commentary is startling: “Having a portfolio that spans steak, Italian, seafood and high end, puts us in a strong position to weather any variability in category demand.” If demand for the entire industry is declining, why would a portfolio of different brands be good? When all is said and done, we believe the success, or lack thereof, of the Outback concept will drive Bloomin’s stock. Unfortunately, we believe management has too many balls in the air to successfully manage that business. Bloomin’ will, inevitably, suffer from the “impact of brain space.”

CAN A 17 YEAR OLD CONCEPT SUCCESSFULLY INTRODUCE LUNCH?

Management continues to roll out weekday lunch at Outback and Carraba’s which, for now, is “comping” positive. However, with only 50% of the Outback chain in a position to serve lunch, the overall opportunity is smaller than many expect.

Curiously, Bloomin’s recent commentary around lunch trends is inconsistent with what others in the industry are saying. According to management: “…as you look out over the last 12 months ending March 31, the lunch segment in general for the industry has held up better than the dinner segment.” We suspect management may be exaggerating the state of the lunch daypart in an attempt to build excitement around their rollout. According to what we’ve heard from the majority of casual dining companies, both the lunch and dinner dayparts are performing relatively the same, with weekday lunch slightly weaker than weekend lunch. As a reminder, casual dining same-store sales trends have been rather anemic for the majority of the year.

As of the end of 3Q13, approximately 26% of Outback locations and 28% of Carraba’s locations were offering weekday lunch. This is up from 25% for Outback and 21% for Carraba’s in 2Q13. During 3Q13, the company lapped the rollout of the weekend lunch at Outback. The weak performance during the quarter suggests that the company had a difficult time lapping the rollout of weekend lunch. As we progress thur 2014, we believe the street will begin to question if lunch is truly incremental to the overall business if Outback does not see a significant improvement in same-store sales in 4Q13.

IS UNIT GROWTH A POSITIVE OR A NEGATIVE?

A large part of the Bloomin’ bull case is embedded in the unit growth potential of the company. We’re not sold on this being a positive. We haven’t seen any mature branded casual dining company grow its restaurant base without running into major problems in due course.

In 3Q13, BLMN opened 14 new system-wide locations and is targeting the lower end of the 45-55 unit guidance for 2013. Development has been slower than anticipated due to the high demand and intense competition for “A” sites. This slowdown could be a blessing in disguise, but we don’t expect it to last. The company is guiding for new unit openings in 2014 to be well in excess of what we saw in 2013.

Another issue is the declining trends at BLMN’s primary growth vehicle, Bonefish Grill. Considering the sluggish top line trends, the brand needs to quickly turn things around in order to justify the 2014 unit opening story.

PRODUCTIVITY

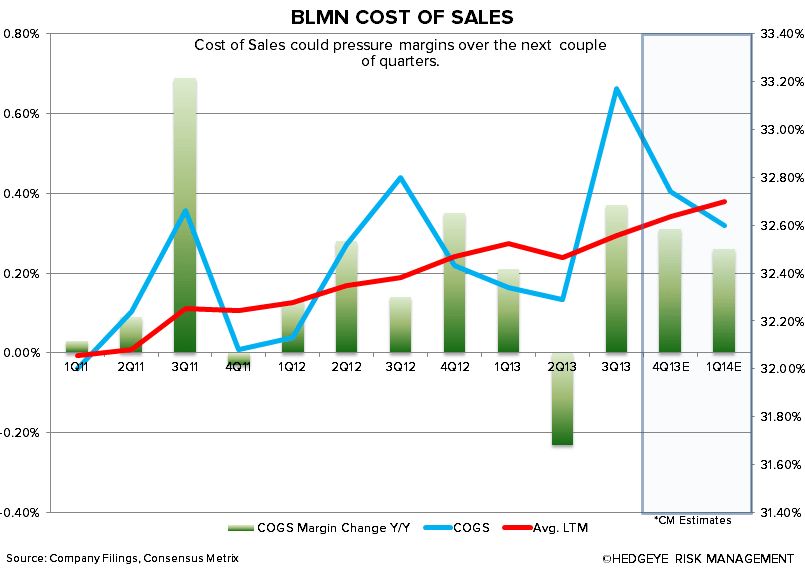

According to management, they are seeing strong progress on the productivity front. This includes year-to-date savings of $42 million of the “at least $50 million” of savings in 2013. According to management in 2013, the majority of savings have come from the cost of sales line, which suggests there is no material benefit to margins given the inflation the company is seeing. On a rolling 12-month basis, cost of sales has gone from 32.47% in 4Q12 to 32.56% in 3Q12 and is expected to edge higher in 4Q13.

Moving to the labor side, the company is suggesting that its new scheduling tool is gaining traction and should lead to further savings in 4Q13. On a rolling 12-month basis, labor costs are expected to only decline by 15 bps in 2013, which includes an estimated 42 bps drop in 4Q13.

For all the hype surrounding productivity savings and the results this will yield, EBIT margins are only expected to improve 39 bps in 2013. The trend certainly appears to be heading in the right direction, but the company will need to see 2%+ same-store sales in order to meet current street estimates.

REGARDING G&A, HOW MUCH IS LEFT IN THE TANK?

At 5.79%, G&A was down 100 bps y/y in 3Q13 and represents the lowest percent of sales in a quarter for which we have the data. This decrease is due to the aggressive management of the line, which was driven down by lower corporate compensation and lower professional fees. We suspect that management pulled forward some cuts from 4Q13 in order to appease the street in 3Q13.

OUTBACK SAME-STORE SALES

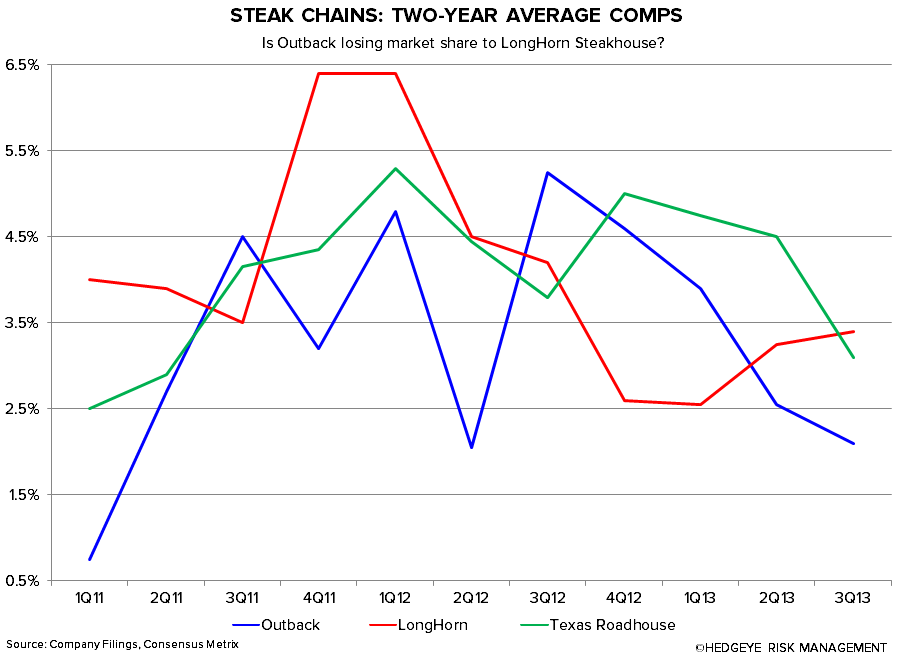

The health of the Outback brand is vital to the success of BLMN. Despite maintaining a positive Gap-to-Knapp in 3Q13, its outperformance has been in steady decline since 4Q12 and appears to be waning. Outback’s Gap-to-Knapp peaked in 4Q12 at +600 bps and has since fallen to +220 bps in 3Q13.

Outback’s Gap-to-BlackBox tells the same story, although with perhaps a more discouraging twist. Because BlackBox excludes Darden’s brands, most of which are struggling mightily, some investors view it as a more accurate gauge of the casual dining industry. The second chart below shows that Outback’s Gap-to-BlackBox peaked at +550 bps in 4Q12 and has since fallen to merely in-line with the industry in 3Q13.

These numbers suggest that Outback is losing market share. This could either be to other unrelated casual dining companies or to its direct competitors. The chart below suggests that Outback has been losing share to LongHorn Steakhouse.

VALUATION

BLMN is up +69.0% over the past year and has outperformed the S&P 500 by 40.8% over this time. The stock is trading at a P/E of 20.5x and 9.3x EV/NTM EBIDTA and above its direct peer group. In our opinion, the current fundamentals of the company do not warrant a premium multiple.

SENTIMENT

Highlighted in the chart below, 80% of analysts rate BLMN a buy while the other 20% rate BLMN a hold. This puts sell-side sentiment regarding the stock approaching levels not seen since September 2013. Further, short interest is only 7% of the float.

Howard Penney

Managing Director