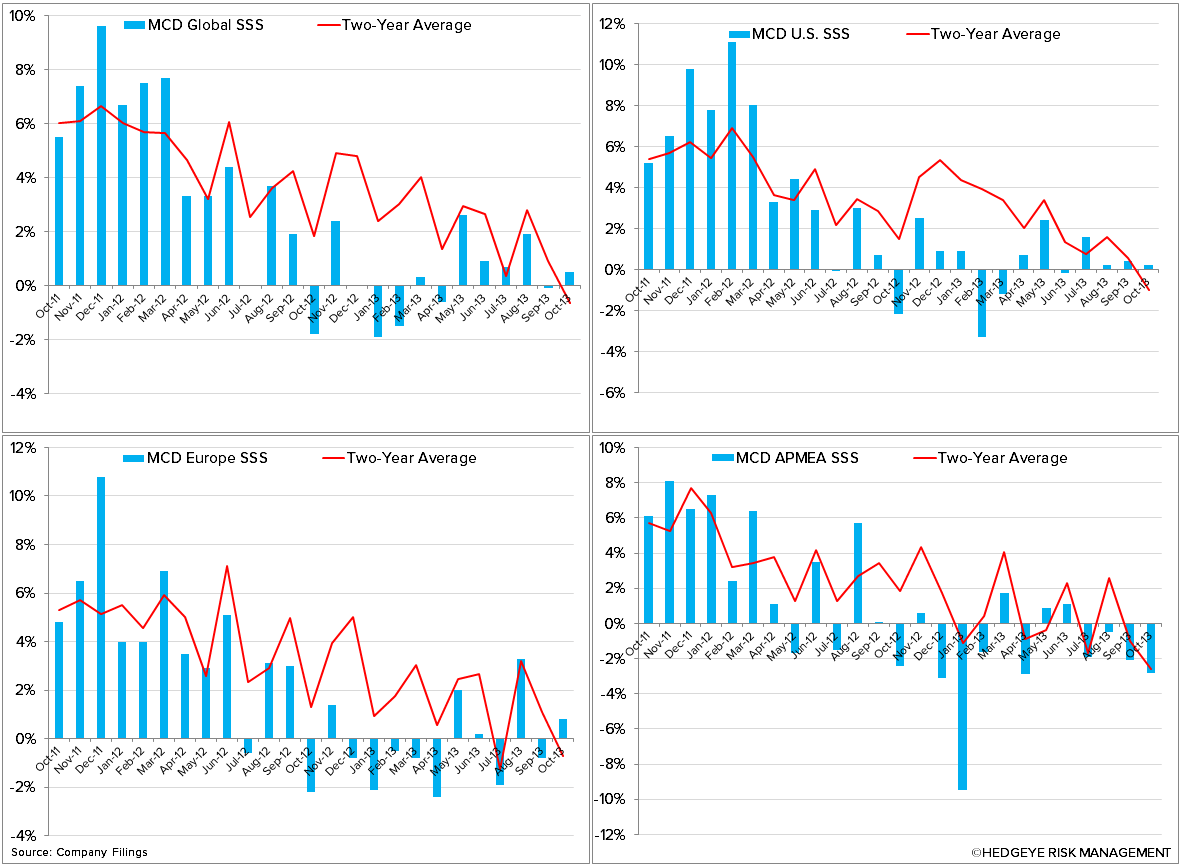

As outlined at the recent analyst meeting, McDonald’s will rely on beverages to drive top line sales in 2014. As we’ve said before, we believe that allocating resources to selling more beverages, particularly hot espresso beverages, will not generate the incremental sales needed to achieve the current estimate of +1.7% same-store sales growth in the U.S. in 2014.

In our opinion, McDonald’s is a food first destination and whenever management shifts their focus away from food and to selling beverages, the core business suffers. The shift in the marketing calendar for the remainder of 2013 is an early indication of where management plans to go.

It was recently reported that, after selling the highly successful McRib nationally for three years, McDonald’s is switching back to offering the sandwich on a regional basis. Rather, McDonald’s will focus the balance of 2013 on selling Mighty Wings (a disaster), the Southwest Premium McWrap (hasn’t driven incremental traffic), and now White Chocolate and Peppermint Mocha specialty beverages.

This implies that management believes adding a premium espresso-based beverage to the menu will generate more incremental traffic than nationally promoting the McRib. Although the McRib will be promoted locally, it will not have the full force of the McDonald’s marketing machine behind it in 2013.

We don’t expect MCD to report strong same-store sales for the balance of the year and well into 2014. Looking back on 2013, MCD was forced to shift its strategy mid-year because new products and the promotional calendar were not resonating with consumers and, as it stands, all indications are for 2014 to be a repeat of 2013.

McDonald’s will report November same-store sales on 12/09. We will post on anything incremental after the release.

Howard Penney

Managing Director