“Anyone who isn’t confused doesn’t really understand the situation.”

-Edward R. Murrow

That was the closing quote from David Einhorn’s most recent quarterly letter. I can’t think of one that better summarizes where we are right now in understanding markets. So I’ll leave it at that.

Back to the Global Macro Grind…

While he’s been quite adept at not violating Rule #1 of investing (don’t lose money), that doesn’t mean Einhorn shies away from writing about where he could make more money. One of those areas is high short interest stocks.

From a Hedgeye Style Factoring perspective, last week was the 1st week of 2013 where SHORT INTEREST (as a style factor) diverged versus its TREND. We look at these style factors by quartile in the SP500:

- HIGH SHORT INTEREST (as a style factor) was -0.5% last week

- LOW SHORTS INTEREST (as a style factor) was +0.8% last week

In other words, if you’re short company that hedge fund consensus (high short interest) doesn’t like, the stock actually had a good chance of going down last week. Look at Tesla (TSLA). That’s new.

What wasn’t new vs. intermediate-term macro TRENDs last week?

- US stocks closing at another all-time high (SP500 = 1804, +26.5% YTD)

- #RatesRising on the 10 yr US Treasury Yield (+4 bps w/w to 2.74% = +99 bps YTD)

- Rate Sensitive “asset classes” (like Gold and REITS) going down on that

In fact, “rate sensitive” was really sensitive last week:

- MSCI REITS (real estate) Index lost another -2.2% going to FLAT 0.0% return for 2013 YTD

- Gold was down another -3.4% on the wk to -26.3% for 2013 YTD

And, to be clear, all those pundits who told you that #RatesRising (tapering) was going to spell the #EOW (end of the world) were dead wrong this year. Wrong is as wrong does.

Would you be wrong to buy anything “rate sensitive” on sale today? Buying any of Bernanke’s Yield Chasing Bubbles is not for the faint of heart. While he won’t acknowledge the mother of all global commodity inflations (2011-2012), history’s score will.

For the YTD here are your Top 5 Deflating of Bernanke’s Inflations moves:

- Silver -34.6%

- Coffee -33.0%

- Corn -29.6%

- Gold -26.3%

- Coal -20.3%

I know. I know. At the all-time high in world food prices (2012), there was NO INFLATION. More Jelly Donuts, please.

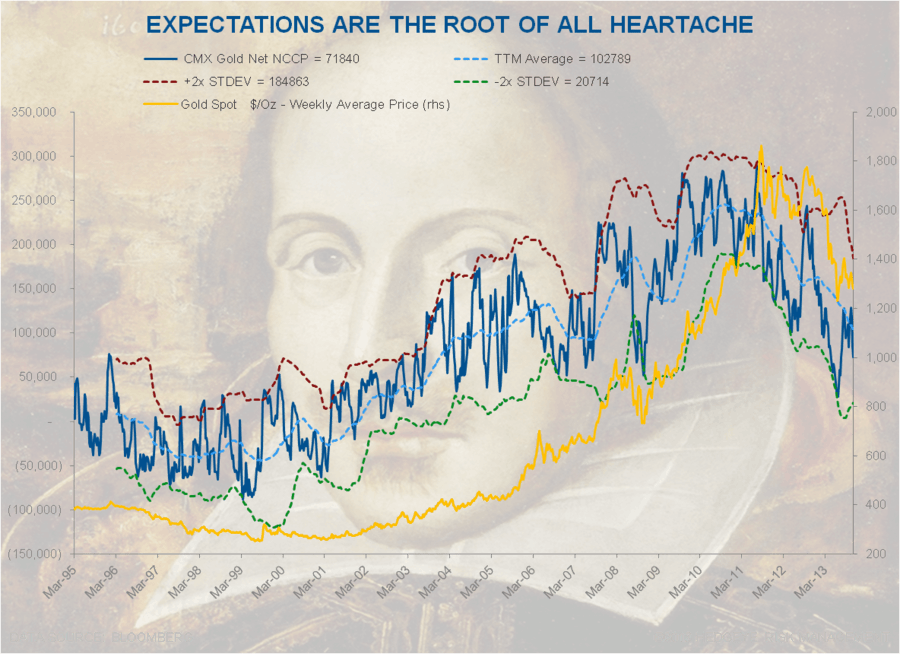

At the all-time high in commodity inflation expectations (2011), check out our Chart of The Day: the net length of the CFTC (Commodities Futures Trading Commission) non-commercial net long positioning in Gold spanning Bernanke’s tenure as Fed overlord:

- John Paulson launches his Gold fund 2010

- EXPECTATIONS PEAK = August 2nd, 2011 = +289,000 net long Gold contracts

- SPOT GOLD PRICE PEAK ($1900.20) = September 5th, 2011

Last week’s net long position in Gold fell below < 75,000 net long contracts for only the 2nd time since 2008. Down -15% week-over-week to +71,840 net long contracts, that’s down -75% from the expectations peak (not to be confused with the price inflation peak).

Expectations, as Shakespeare wrote, are the root of all heartache. And my guess is that those shorting Gold -1% this morning will have some heartache of their own when we get back from Thanksgiving. So get all wild and crazy today, and buy yourself some. It’s “cheap-(er)”!

What is not confusing about Gold is that it trades on expectations. When the market expected interest rates to rise into their YTD peak (January-July 2013), it went down; when the market expected rates to fall (July-September 2013 into no-taper), Gold went up.

Oh, and if you are confused as to whether or not our central planning overlords will allow #RatesRising (and Gold falling) from today’s time/price, join the club. Because, eventually, the Fed may very well lose control of that expectation too.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.69-2.83%

SPX 1

VIX 11.85-13.62

USD 80.54-81.29

Brent 106.25-111.24

Gold 1

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer