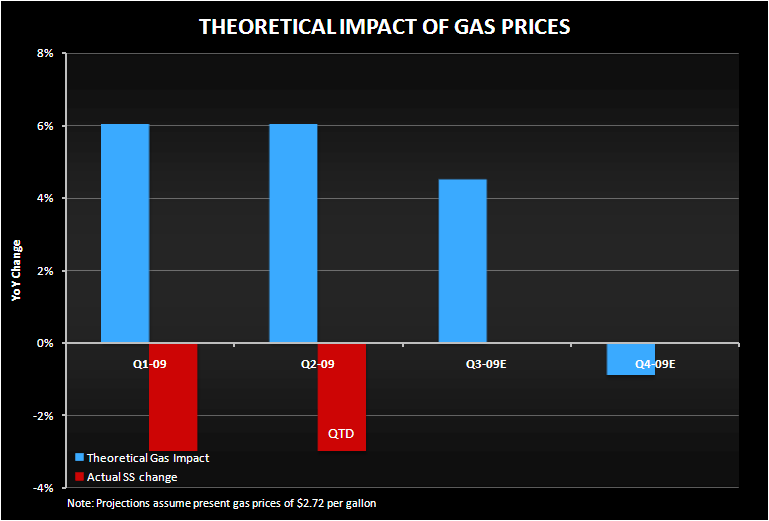

Historically, gas prices have been a highly significant driver of same store regional gaming revenues. We have expounded upon this relationship in our 06/29/08 note, "GAS PRICES AND THE ECONOMY DO MATTER", and several other posts since then, including "REGIONALS: DISCERNING A TREND" (06/18/2009). For regional gamers, every 1% y-o-y change in gas prices results in an inverse 0.15% change in same store gaming revenues, holding all other factors constant. In thinking about organic growth in regional revenues, it is necessary to focus on the trend in gas prices.

Despite the estimated benefit from the significant y-o-y drop in gas prices in 2009, same store revenues for the regional gamers have been negative in every month since January. The 40% decline in gas prices through May 2009 may be masking worse fundamentals than the numbers are suggesting. So the question is to what degree were the less bad numbers we saw come out of regional gaming a result of the nose dive in gas prices?

According to our calculations, the 40% y-o-y decrease in gas prices through May 2009 has had a 6% positive impact on same store gaming revenues. YTD same store gaming revenues through May 2009 declined by 3%, implying that if not for the gas tailwind, gaming revenues could have been down 9%. Note the chart below.

Looking at spot prices today at $2.72 implies a 30% y-o-y decline in gas prices in 3Q09, resulting in an estimated 4% positive impact on same store gaming revenues. However, the tailwind turns into a potential headwind in the fourth quarter of this year, as the y-o-y comparison for gas prices turns negative, leaving the regional numbers to reflect a more true demand level without the mask of the fuel benefit.

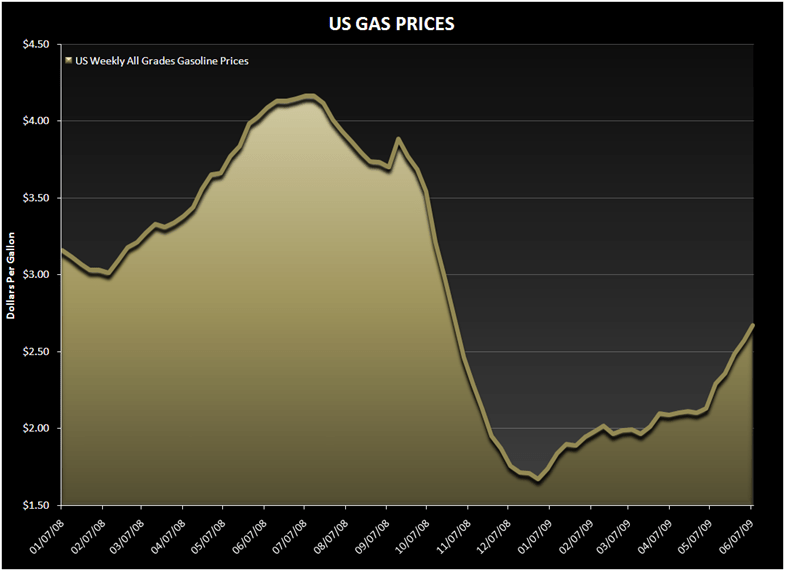

As can be seen in the chart below, gas prices have spiked dramatically in the last two months. It remains to be seen what the "sticker shock" impact will have resulting from the sequential change in gas.