THE HEDGEYE EDGE

Carnival Cruise Lines (CCL) has been in rough seas the last couple of years. It started with the Concordia incident in January 2012 and more recently impacted by ship operational problems (e.g. power failures, fires, etc). While our team has been cautious on Carnival since the Triumph fire (Feb 2013), we think, after three guide downs in yields and earnings, performance and sentiment may have bottomed.

We are encouraged by the changes made by the new management team with new CEO Arnold Donald at the helm. Given the deterioration of the Carnival brand and a breakdown in communication between customers and the agent community, it was a timely change. In addition, the collaboration between Holland America and Princess may help eliminate operational redundancies and reduce in-house competition.

Our proprietary cruise pricing survey indicated that starting in October 2013, Carnival brand pricing in the Caribbean had stabilized; pricing further improved in November 2013. Furthermore, European business seems to be on the upswing. These are encouraging signs before the 2014 Wave Season.

TIMESPAN

INTERMEDIATE TERM (TREND) (the next 3 months or more)

Wave Season begins in mid-late January, where the bulk of 2014 bookings will be made. While CCL has already warned of a tough operating environment for the 1H 2014, 2H 2014 yields are estimated to be modestly positive, due to easy comps.

LONG-TERM (TAIL) (the next 3 years or less)

2014 is another transition year for CCL as investors look ahead to 2015 for normalization purposes. In 2014, the ship operator will be busy with the many major ship revitalizations it will need to conduct to improve the quality and sustainability of its fleet. The rebuilding of the Carnival brand will be a slow one but we believe the management has put in place aggressive marketing/advertising programs and incentives to right that brand over time.

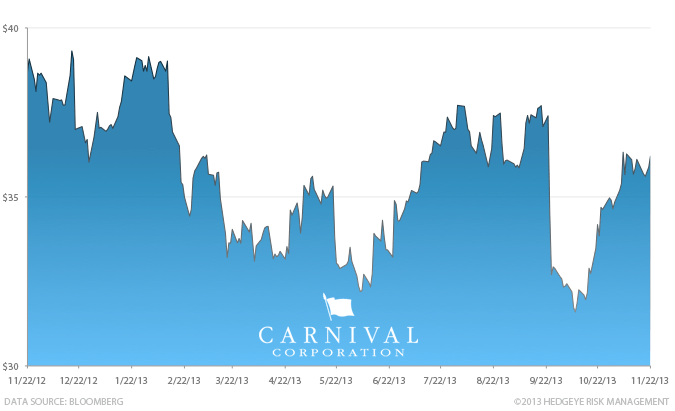

ONE-YEAR TRAILING CHART