Here are the latest comments from our Sector Heads on their high-conviction stock ideas.

***Please note that we added two new stocks -- Carnival Cruise Lines (CCL) and Greenhill & Co (GHL) -- to Investing Ideas this week. In addition, we removed Boyd Gaming (BYD) from our high-conviction Investment Ideas.

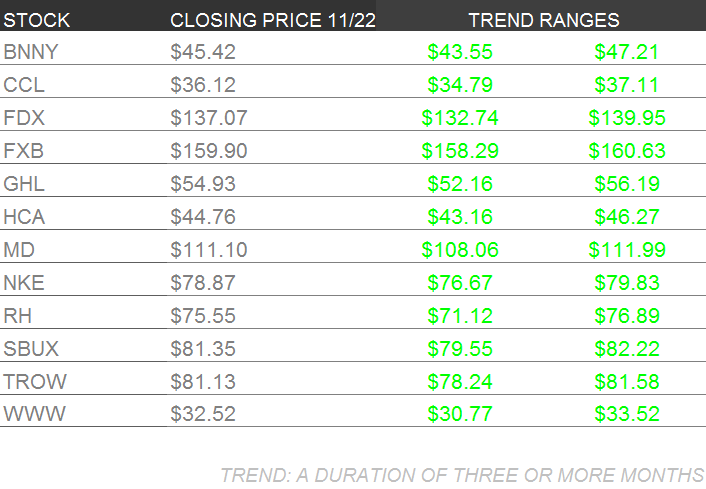

INVESTING IDEAS

BNNY – Annie’s stock was down 5% on the week, underperforming the consumer staples group. Consumer Staples analyst Matt Hedrick says there was no new news out on the stock beyond last week’s announcement of a 2.5MM common stock secondary. Hedrick says this dilution will not compromise the overall per-share profit outlook for the company. His long-term bullish thesis on BNNY remains intact, based on the company’s advantaged organic portfolio, strong retail positioning for growth, and easier top line and gross margin comparisons going into the back half of its fiscal year.

CCL – Please see the full report sent out Friday by Hedgeye's Gaming, Lodging & Leisure team.

FXB – European Macro analyst Matt Hedrick expects currency wars to persist, further devaluing the USD and EUR to persist, with the British Pound the relative winner across both currency cross trades. Both Mario Draghi at the ECB and Ben Bernanke/Janet Yellen at the Fed continue to signal a dovish policy stance. In contrast, BOE policy discussion continues to set a hawkish tone: Hedrick expects interest rates to be on hold over the medium term, with expectation for a hike over the longer term, and the asset purchase program target (QE) to remain unchanged.

Both positions should strengthen the GBP/USD and GBP/EUR. Says Hedrick, “we continue to see improving data out of the UK, including GDP revisions estimating 2014 growth of 2.8%. Further tailwinds include CPI that is slowly deflating (at 2.2%), which should be a benefit to consumer consumption, and the unemployment rate is slowly declining (at 7.6%).” He is looking for the GBP/USD to head to the $1.65 - $1.70 range over the intermediate term.

FDX – We learned from recent filings that several noteworthy investors, including Soros, Paulson and Dan Loeb’s Third Point, have recently entered positions in FedEx. These investors may see the same opportunity to create value in the Express division that Industrial sector head Jay Van Sciver has been presenting to investors for a year. While the presence of such investors always spurs enthusiasm – notably activists such as Loeb, who has already held talks with FDX CEO Smith about succession – it can take time for events to unfold. Van Sciver says in the immediate term, attention is likely to shift toward earnings in mid-December.

GHL – Please see the full report sent out Thursday by Hedgeye's Financials Sector team.

HCA– Healthcare.gov continues to limp along, although from our daily check of Alexa.com, traffic continues to fall, which we believe means progress in processing applicants. But this week we also heard another piece of even more frightening information, that healthcare.gov will likely be unable to process payments for medical care as of January 1. That's a big deal. Because so far, given the commitments made by all of the intertwining stakeholders in the US medical Economy, the only way to go from here is forward, even if things are not running smoothly. There simply is no way to reverse course now. But if payments can't be processed, and cash can't circulate, that sounds like a mortal threat.

We still see a lot we like even before ACA, but we will get very concerned if this story gathers momentum. If the threat of repeal moves from the realm of rhetoric to the realm of possibility, it would be a very negative sentiment overhang, at least in the short term. But that is a big if right now and appears unlikely. (Please see "Sector Spotlight" below for additional insight.)

MD – US Census released preliminary birth numbers through June 2013 this week. As we expected, volume was down year over year, not by a lot, but some. While the overall trend continues to improve, we would have expected to see a consistently positive trend by now.

As it is, the deferral pool now stand at between 10% and 20% of the annual birth rate of 3.8M , and that is just counting women who have yet to have their first child. We are 6 years since the first down year, the median age of the deferral class is now 32. If even a small percentage of women who have held off having a baby the last six years start to return to the maternity ward it will be a huge tailwind for MD earnings and the share price. (Please see "Sector Spotlight" below for additional insight.)

NKE – In this week’s investing ideas we thought we’d show, rather then tell. Every week we comb through athletic apparel and footwear point-of-sale (POS) data. That’s right, in this instance POS stands for point-of-sale. These numbers are not perfect by any means. They fail to appropriately address a brand’s direct to consumer business, and since the term ‘athletic’ is pretty vague in its description it is hard to judge what categories/products are and are not included in the data. While the data may not be perfect in its entirety it is consistently inconsistent, and it gives us a birds-eye view of the US athletic apparel marketplace allowing us monitor industry, brand, and category trends.

We whipped up a chart that breaks out the market share for three of the brands in NKE’s portfolio: Nike, Brand Jordan, and Hurley. The market share numbers reflect year-to date totals starting from the first week of February 2013 and they are compared to numbers from the similar 2012 time period. To give you some context, total athletic apparel sales for the year-to-date are over $6.9 billion and have grown 8.7% year-over-year. The key callout here is obviously Nike brand. It has captured an extra 4.2% of the market share this year and now accounts for over 25% of the total market. Sales of Nike have grown 30% over last years totals, and there has been no deterioration in price. What does that tell us? Well, people buy Nike, lots of Nike and not because it’s on sale.

RH – Williams Sonoma reported third quarter earnings numbers on Wednesday. Total company comps at WSM were up 8.2% led by their Pottery Barn (+8.4%) and West Elm (+22.2%) divisions. All in all we are encouraged by the print as it relates to RH, and we’ll walk you through some of the important read-throughs.

1) WSM’s prices are under pressure. Gross margins were down as a result of what they called ‘competitive pricing strategies.’ We interpret that clever choice of words to mean that someone (read RH) out there is offering a better product at a more attractive price. RH has a unique sourcing model that allows it directly source product, which eliminates the middleman markup. WSM is trying to realign its sourcing infrastructure, but they are well behind RH on this front.

2) RH’s closest compares are Pottery Barn and West Elm. Those businesses performed well, especially West Elm ,which like RH, is growing its store count. This isn’t a situation where WSM wins and RH loses. Home furnishings is a $164 billion dollar industry. Neither company currently holds a significant share of that marketplace, and both can continue to steal share from local and regional competitors.

3) WSM called out the strength of its Baby division within Pottery Barn Kids. This concept is gaining traction with consumers and strengthens our belief that once RH Baby gains a retail presence in the new Design Gallery concept, it can be a significant revenue driver.

4) Williams Sonoma put up a +1.4% comp number. This concept has comped negative in 5 of the last 8 quarters. RH Kitchen has the opportunity to be what Williams Sonoma is not. Limited SKU’s, less reliance on food and seasonal items. Shoppers aren’t responding to Williams Sonoma and we believe RH can fill that void.

5) WSM is opening its first store in London in 4Q. We don't foresee international expansion in RH's near future, but based on WSM's success entering the market we could see international as a real possibility for RH.

SBUX – Starbucks’ management presented at Morgan Stanley’s Global Consumer & Retail Conference earlier this week. One big takeaway is that transactions per labor hour at Starbucks is set to end FY13 at 11.7. This is an improvement from FY12 and significantly higher than it was five years ago. Not only is Starbucks getting bigger, but it is getting more efficient as well. Restaurants sector head Howard Penney says “We cannot overstate the importance of speed of service in today’s restaurant industry, particularly as it applies to quick-service and fast casual companies.”

Speed of service is a key part of the quick-serve experience. Indeed, it’s called “quick serve” for a reason, and the faster consumers can get in and out of a store, the more likely they are to return. SBUX is acutely aware of this and has consistently capitalized on efficient in-store execution. On another front, Penney notes some investors are concerned that the rollout of La Boulange will inevitably slow the speed of service in SBUX stores. “We have not seen any signs of this.” he says, and reminds investors that SBUX has been leading the technological revolution in the quick-service category. Penney believes their superior innovation will allow them to continue to deliver a speedy customer experience.

TROW – During our recommendation of T Rowe Price as a core long position, we have solely been using industry information on equity flows from the Investment Company Institute (ICI), the trade group for the asset management industry. However, there is a private survey of asset management performance and flows called Simfund which we don’t use that projected a very positive outlook for TROW separately from our research process using ICI data.

Last week, this private Simfund survey calculated that in October alone that T Rowe has netted over $1.8 billion in new net inflows, more than the prior 3 months combined which totaled just $1.2 billion. Thus it is safe to say that the fourth quarter has started in very strong fashion for this leading equity manager. In addition, Simfund projected that TROW’s industry leading performance gap has widened favorably, meaning TROW’s mutual fund families have increased their lead as the best performing mutual funds of the public asset managers. According to Simfund, now 70% of TROW’s assets are 4 or 5 star Morningstar rated, the only mutual fund products that have historically generated any significant inflow (see annual 4 and 5 star inflow versus 1 to 3 star rated products below).

In a nutshell, TROW stock is a prime beneficiary of the positively trending U.S. stock market with industry leading performance and improving retail equity mutual fund flows.

WWW– Let’s be clear. We don’t like Wolverine Worldwide because of its strong position in the athletic apparel marketplace. It simply can’t compete with the likes of Nike and Under Armour. However, there is one very important thing that WWW does better than the rest of them and that is sell product in international markets.

Merrell and Saucony are on a tear in 2013. You can see this in the chart below which compares year-to-date (February – now) sales with the similar period in 2012. Clearly the brands are doing something right.

Macro Theme of the Week – The Bubble Bubble

There’s been lots of talk lately about “bubbles” in the marketplace. Everywhere we turn folks are warning us “Don’t put your money there – it’s a bubble!” Bubbles here, bubbles there… bubbles bubbling everywhere. We are witnessing a bubble in bubbles.

The Fed still doesn’t seem to be able to bring itself to taper, even with strong growth in GDP, and with a marked downward trend in unemployment. The markets signaled their readiness last month, looking to continue massive outflows from fixed income – which stood to be matched by inflows into equities. The markets were, in fact, so very ready for the Taper, that the Fed switcheroo hit like a sucker punch. What were they thinking?

One noted Wall Street pundit with a jaundiced view of the Fed may be onto something. Fund manager William Fleckenstein says “Wall Street has sort of fooled itself with the Fed all year." There will be no taper, says Fleckenstein. Instead, “the Fed is going to make it much more difficult to leave QE. What that really implies, though, is that everything they've been doing thus far hasn't worked.”

We expect Chairman Bernanke would reply, “Whaddaya mean ‘it hasn’t worked’? Look how strong the recovery is!” We honestly could not say whether this is dumb luck on the part of the Chairman – being in the right place at the right time – or, as his apologists say, imagine how bad it would have been without QE. What we do believe is that Bernanke is a creature of his own rather imposing intellect. Having been placed in a position to run the mother of all market experiments, he appears determined to defeat Keynes’ most famous dictum: “The market can stay irrational longer than you can stay solvent.”

No one is more eternally solvent than He Who Owns The Printing Press. With his hand, God-like, eternally cranking out dollars, Bernanke is the Irresistible Force that will finally overpower the Immovable Object of the financial markets. This will be, in a Marxian-Hegelian-Fukuyamian “end of history” scenario, the End Of Keynesianism As We Know It – when government policy will finally triumph over the marketplace.

People whom we consider smart believe Yellen is more of a pragmatist than her about-to-be-former boss. Unlike True Believer Bernanke, they think Yellen can be convinced by facts to change her opinion (another famous Keynes quote: “When the facts change, I change my mind. What do you do, sir?”) This actually creates a quandary: if you think Bernanke’s policy has been horribly misguided and destructive, then you can’t wait for Yellen to take over and be convinced by reality to change course. If, on the other hand, you fearfully suspect that Bernanke’s course may have been the horribly best we could have hoped for in a miserable situation, then undoing QE could make matters worse than worse.

What do the markets say?

Hedgeye Financials sector head Josh Steiner observed “the US Dollar keeps dropping on Fed comments, but the 10-year Treasury yield keeps going up,” just one of the bubble-icious divergences as the Fed continues the monetary equivalent of Sherman’s March to the Sea. Despite Yellen’s clear message of more bond buying, tweeted Steiner, the long end of the Treasury yield curve was “hanging in like a champ,” indicating weakened bond prices.

By historical measures Treasury yields should be signaling a period of champagne and dancing in the streets. The traditional bank “free money” trade, the spread between the 10-year bond and the 2-year, has widened substantially. And the yield gap between the 20-year Treasury and the three-month T-bill has blown out to the upside. This steepening of the yield curve has historically been an indicator of coming economic expansion. Meaning that we appear to still be firmly strapped into our front-row seat on the #GrowthAccelerating Express.

B. T. D. B.

Our CEO, Keith McCullough, takes Bernanke to task once again this week (see “It’s A Certified Circus”) as the Fed chairman told the Economists Club of Washington that having the Fed stay the course is “the surest path to recovery.” As the Fed has moved the goalposts on its plan to taper, we are seeing lots of cash piling up. Lots and lots of it. A bubble in cash, in fact. Where will it all go when it bursts?

We are meeting with institutions who are increasingly uncomfortable with the idea of being invested in any particular asset class: bonds could break down if the Fed finally tapers and rates pop; equities have had a huge run and could easily top out if there is even a moment’s uncertainty; commodities still need someone like China to come to the rescue – and Goldman Sachs is calling for a double-digit drop in the price of gold, iron ore, and soybeans all of which could hurt worse than dropping a 14K ingot on your toe, if you are invested in the wrong ETFs.

Says McCullough: Yep, there are bubbles out there. Lots and lots of them. And as long as the pile of cash on the sidelines continues to grow, the bubbles will float higher and higher.

There was last year’s fear-mongering bubble that popped while everyone was calling the top in a “US stock market bubble.” Looks like our 2Q13 #GrowthAccelerating Macro call continues on target. Says McCullough: Buy the darned bubble!

There’s a bubble in stocks folks love to hate, as the most heavily shorted stocks in the S&P 500 have risen by over 31% year to date, outperforming the broad S&P 500 itself by nearly 6%. Buy the darned bubble!

#GrowthAccelerating. US stocks have soared to all time highs as we watched the country go from 0.14% GDP with the SP500 at 1360 in Q412, to 2.84% GDP Q313. We’ve had a great ride, says McCullough. For #GetActive traders, McCullough suggests raising cash on up days, and redeploying it at the next dip. If GDP growth “slows” to only 2% or a bit above, the equities run could flag. Much of the push in stocks is being driven by a massive rotation out of fixed income and into equity mutual funds, which we have been writing about. Fund flows chase performance, and as the equities market pauses to catch its breath we would expect a dip in equity fund inflows. We think it will not be sustained enough or big enough to damage the long-term bullish trajectory, but it will likely be playable for active traders and bubble buyers.

Says McCullough, “the Fed will cheer on the #GrowthSlowing data as more reason not to taper… and, in doing so, they’ll suck in every last lemming who hasn’t been long US stocks in 2013 to buy the bubble.” But, says McCullough, the “pop” is a long way off. Indeed, if the Fed has its way, that day may never arrive.

Meanwhile the cash bubble continues to inflate as more and more fund managers sit on their hands, waiting for clarity. With clarity will come investment decisiveness. With decisiveness will come cash inflows. With inflows will come market tops.

Until then, the key to trading the bubble is not buying at the absolute bottom, nor getting out at the absolute top. No one can do that – not reliably and not repeatably. The key is managing risk within the range. McCullough reminds us that “tops are processes, not points.” Once we see the process unfolding, we will manage the risk accordingly. Until then, says McCullough, B.T.D.B!

Sector Spotlight – Healthcare: Births of a Nation

Healthcare sector head Tom Tobin continues his proprietary survey of US birth rates. While these figures have obvious implications for companies in his sector – notably, Tobin’s two current names on the Investing Ideas list: HCA and MD – they also contribute to the general economic picture. Tobin’s earlier work on this series has identified correlations with women’s employment and new family unit formation, and implications for home sales and for sales in the things that go into homes, such as home furnishings, major appliances and pets.

This week Tobin picked up on newly-released data from the US Census Bureau that match the latest results from his proprietary OB/GYN survey “signaling that maternity trends remain flat to down over the last 5 months.” Census Bureau birth statistics, now available through June of this year, seem to support Tobin’s macro view, and to confirm his latest survey results.

Tobin notes that birth rates are a significant driver for stocks in the Healthcare sector. In the US, says Tobin, “births make up 25% of all inpatient hospital admissions, 30% of all commercially insured hospital admissions, and 40% of all Medicaid hospital admissions.” Survey results last year led Tobin to expect a recovery in maternity trends but he says the latest trend appears to be flat to negative, at least through this month. The CDC calculates this slackening of the pace of births indicates a decline of between 410,000-759,000 births by first-time mothers in their survey called “Deferred and cancelled births for first-time mothers.” All right, not a poetic turn of phrase. But a significant statistic. This slowdown in birth rates also creates a potential reservoir that can have explosive upside impact, should these women come back into the maternity pool.

Regarding Tobin’s Investing Ideas picks, MD remains highly levered to maternity trends. While there are other drivers such as Parity and M&A, the marginal update has been less positive, where some deals are slipping into 2014 and parity payment changes are slow to evolve. The overlay of NICU patient days and US birth remains tight with a 0.70 correlation.

Tobin says HCA is also still highly levered to maternity, although pricing, surgical volume acceleration, and organic bed growth remain tailwinds for this company.

There are a few other data points in the report that invite speculation. One is that medical practices with patients with incomes over $50K report weak deliveries similar to lower income practices, those with incomes under $50K. While some observers read this as meaning income is not a factor, it could be that there is a mid-range, where families are not earning enough to make it compelling for a woman to keep her job rather than stay home to give birth, but not earning so little that they can’t contemplate the cost of having a baby at all.

Meanwhile, practices with a higher percentage of Medicaid patients report positive trends relative to practices with higher percentages of patients with commercial insurance. Again, while there is no clear conclusion to be drawn, this trend could reflect women opting to remain in full time employment, where they retain medical benefits paid for, at least in part, by their employers.

All this is only speculation – but then, that’s what makes the stock market go up and down. Tobin continues to expect maternity trends to recover over time, “based on the size of the deferral pool, trends in age specific confidence, household formation, and employment.”

Investing Term – Healthcare Sector

Healthcare represents a significant portion of most developed nations’ economies. This business sector is made up of companies that offer a range of services to maintain health, prevent and cure disease, rehabilitate, sustain, and ultimately provide final comfort for individuals. Broadly defined, Healthcare contains everything from biotech and pharmaceutical companies that do basic research and create and market drugs, to medical devices and diagnostics, to hospitals and the machines and people who fill them, to the health plans – yes, including the Affordable Care Act – that get folks into the hospitals and HMOs, where the practitioners use the machines, devices, drugs and a broad range of other treatments produced by companies in the group to take care of what ails you.

It is estimated that the Health Care segment on average consumes over ten per cent of developed economies’ GDP, and while the sector has traditionally been seen as defensive – people need health services no matter what the broad economy is doing – significant trends can emerge that affect sector performance. Some of these appear to be related to broad demographic and economic changes – as exemplified by Tobin’s proprietary work on US birth rates and the implications for economic growth. And some are clearly discretionary, even if they balloon into major revenue drivers. Think Botox, for example, or earlier waves of cosmetic surgery such as breast implants.

This year, the broad Healthcare sector has done well, generally keeping pace with the S&P 500, while some subgroups within the sector have outperformed. According to at least one report, over three-quarters of Healthcare companies reporting in the current earnings season have beaten consensus earnings projections, putting the group slightly ahead of the broad S&P index. As of the end of October, Healthcare ETFs had risen over 30% YTD – not really beating the S&P overall, but with performance like that who’s complaining? Meanwhile, BlackRock reports that their own IBB Nasdaq Biotechnology ETF had risen over 52% by the end of 3Q13.

Gold in them thar ills…?

- By Moshe Silver

Moshe is a Hedgeye Managing Director and author of the Hedgeye e-book Fixing A Broken Wall Street