“Unlike an inexorable, Newtonian “great machine”, the economy is not a closed system.”

-Geoger Gilder

That’s a quote from the end of lucky chapter 13 of one of the best markets/economics books of 2013, Knowledge and Power, by George Gilder. I like this book because it’s the precise opposite of what your central planning overlords @FederalReserve think.

Yesterday, at the Keynesian-economics-Club-of-Washington-D.C. event, Ben Bernanke proclaimed his mystery of faith to his head nodders: “the surest path to recovery” is for the Fed to do more (read: no taper).

Right, right. It’s a good thing he’s sure.

Back to the Global Macro Grind…

This, of course, is the basic divide between how most of us market-practitioners think about markets/economies versus some un-elected and unaccountable academic theorist does. Core to Fed group-think is certainty whereas what we do is embrace uncertainty.

Markets and economies aren’t some theoretical “great machine” that behaves in “equilibrium.” Markets and economies are dynamic and non-linear. Anyone who has studied history understands that.

I’ve been on the road seeing clients in Los Angeles and San Francisco this week. I’ll be in Vegas tonight and Phoenix tomorrow. No matter where I go, I get the same feedback from market-practitioners about Fed policy – uncertainty.

At the same time, these dudes (and dudettes) backslapping one another at the Fed think that they have this completely under control. At one point yesterday, Bernanke said that his “forward rate guidance is helping the economy.”

Pardon?

Taper, no-taper, taper, no taper, maybe-taper, no taper, change goal posts on taper, don’t taper…

It’s a certified circus at this point.

The smartest investors I meet with have the humility to tell people that they have no idea how this ends. So that’s comforting, right? Not only one of the sharpest clients we have, but one of the best performers in 2013 YTD, summarized that this he-said-she-said-taper-talk thing has given him a tremendous amount of conviction in one position – cash.

“Keith, with all of the illiquidity and policy risk factors building out there, I really like cash.”

Indeed.

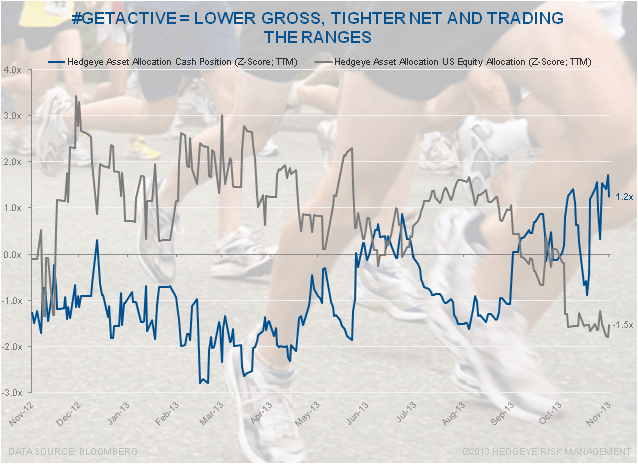

After effectively day-trading Yellen’s predictable behavior last week, I’ve gone from 48% cash in the Hedgeye Asset Allocation Model to 60% this morning. But I was at 66% cash yesterday morning, and bought-the-damn-bubble in a few things on red again yesterday.

Day-trading? Yep. I have no problem with that. Do you? #GetActive

I realize its below these uber intellectual types at the “Economics Club of Washington” to risk manage (read: trade) the market risk they are superimposing on us every day. And I kind of like that. Maybe they’ll label me a lower-class-trader, or something like that.

Moving along…

What’s my call? It’s been a fantastic year to be long US #GrowthAccelerating (from 0.14% GDP with the SP500 at 1360 in Q412 to 2.84% GDP Q313 and US stocks at all-time highs), and now, on up days, it’s time to raise cash.

Looking at both real-time market indicators (Russell2000 growth has been making lower highs since locking in its all-time high on October 29th) and high-frequency economic data, it appears to us that the slope of the line on US growth is peaking.

Since what happens on the margin matters most, if and when the US economy slows (from here) to say 2% (or 1.6%, which is now the downward bound in our GIP model for US GDP Growth in 2014), what do you think the top performing Style Factor in US Equities (GROWTH) is going to do?

No worries, you don’t have to guess – that style factor is already starting to do what you should expect it to do – slow. As US equity market momentum slows (on lower and lower volumes), both the Fed and its nodders are going to get lulled to sleep.

Moreover, I think the Fed will cheer on the #GrowthSlowing data as more reason not to taper… and, in doing so, they’ll suck in every last lemming who hasn’t been long US stocks in 2013 to buy the bubble.

How messed up is that? I have no idea on timing, but oh how this “great machine” of Keynesian certainty is going to fall.

Our immediate-term Risk Ranges are now as follows:

UST 10yr Yield 2.67-2.81%

SPX 1

VIX 11.85-13.88

USD 80.48-81.36

Brent 103.68-108.69

Gold 1

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer