We are adding PBPB to Hedgeye best idea list as a SHORT.

Chipotle redefined the quick-service industry with its innovative operating model, Panera created the bakery café segment and Noodles catapulted into the fragmented Asian fast casual category. All three are unique concepts that have, in a sense, redefined their respective categories.

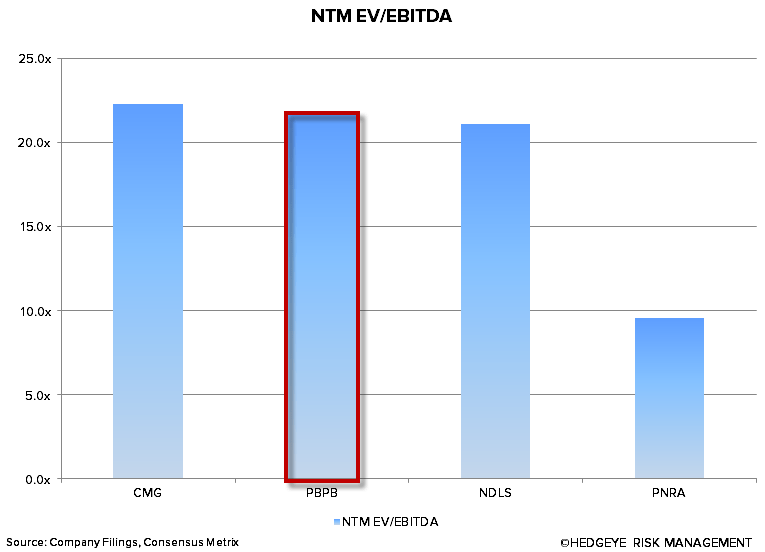

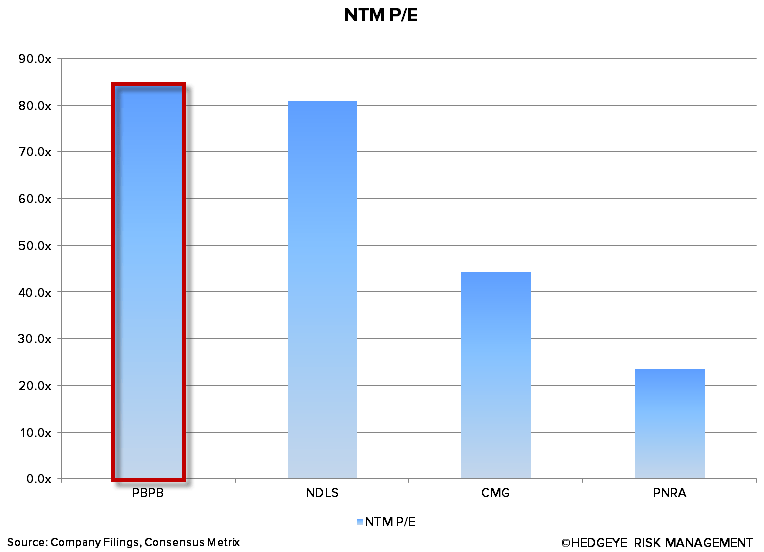

At the heart of it, Potbelly is a single daypart, low margin, low return sub shop with declining traffic and little competitive advantage over its most basic competitors. Admittedly, these are not quite the qualities we’d expect to find in a company that is trading at a P/E of 84.3x and 21.7x EV/EBITDA on a NTM basis. But, this is precisely what we have here.

To be clear, we believe Potbelly is a solid company with a strong management team, but it should not be trading at a premium multiple to its aforementioned peers.

With that being said, we would not be surprised to see PBPB decline by 30-40% over the next twelve months.

As we wrote last week, in aggregate, the current valuations seen across the casual dining sector are shockingly high. In fact, we have no problem referring to them as bubble-like and we’ve found this extends beyond the depths of casual dining stocks to several newly minted “growth” restaurant stocks. Our CEO, Keith McCullough, did a nice job contextualizing these bubbles in this brief excerpt from yesterday’s Early Look titled “Weird Bubbles”:

From a US stock market “Style Factor” perspective, check out the score:

- LOW YIELD (i.e. GROWTH) stocks = +40.4% YTD

- Top 25% EPS GROWERS (by SP500 quartile) = +37.2% YTD

- HIGH BETA stocks = +35.8% YTD

From a pure “Style Factor” perspective, PBPB fits the bill of a “growth” restaurant stock. Let’s consider management’s aggressive guidance:

- New unit growth of 10%+ for a “long period of time”

- Low-single digit same-store sales growth

- At least 20% annual adjusted EBITDA growth

- At least 20% annual net income growth

- At least a 25% return on invested capital, as measured by the second full-year profit of new shops

- Shop margins above 20%

At its core, Potbelly is a local sandwich chain competing in the most competitive segment of the restaurant industry – the sandwich segment. Although many people like to refer to it as the newest fast casual concept, the reality is it’s only at the “intersection between the fast casual and sandwich categories.” Needless to say, Potbelly’s operating model, while solid, is nothing close to jaw-dropping.

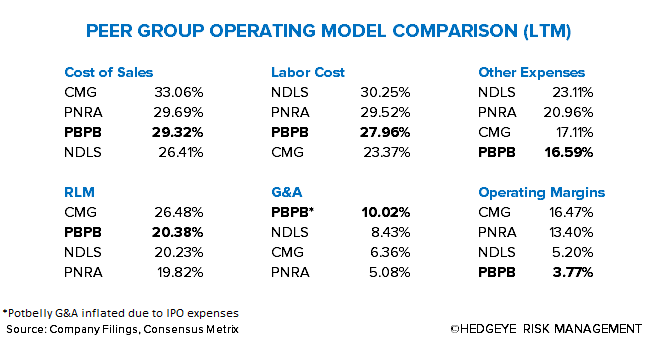

Peer Group Operating Model Comparison

- Potbelly’s average unit volumes are low.

- Food costs are in-line with Panera’s. There is very little room to move lower without downgrading to lower quality food.

- The company appears to be very efficient, with labor costs running at 27.96%.

- Other operating expenses are also very low, which could be the difference-maker in maintaining 20% store-level margins over the long haul.

- Excluding IPO expenses, Potbelly’s G&A costs are running closer to 8%, which puts it fairly in-line with its competitive set.

- Even after adjusting for lower G&A costs, operating margins remain low and will require sales leverage for any further upside.

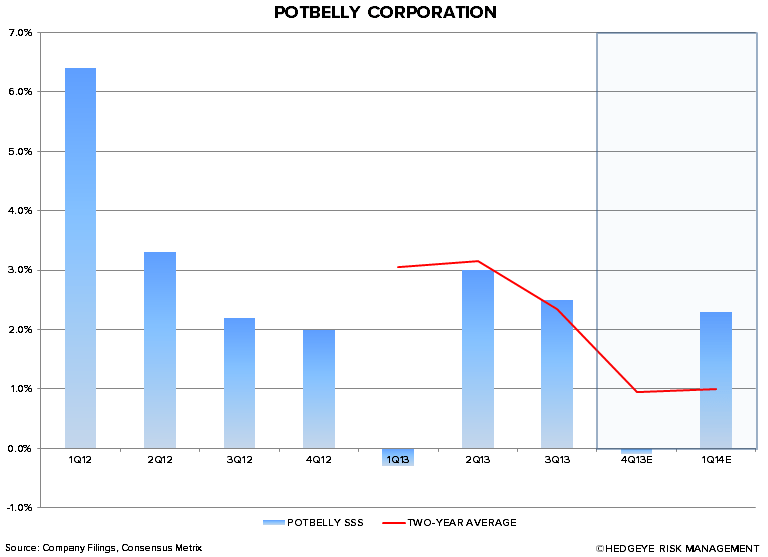

Same-Store Sales

Management’s long-term guidance of “low-single digit same-store sales” implies that they believe, or want us to believe, they have the ability to take price in order to consistently drive average check higher. In fiscal 2012, Potbelly’s average check was $7, which, on the surface, appears to be in-line with other fast casual operators. With average check already at this level, relying on price as the primary driver of future profitability is a risky proposition. Needless to say, we haven’t seen anything recently that would suggest this rate of same-store sales growth will come from traffic gains. Potbelly has seen traffic decline for at least the past 3 quarters and expectations are for this trend to continue into the first half of 2014.

Average Unit Volumes

The Potbelly mission is to be “the best place for lunch.” While a strong focus on lunch is important, restaurant companies that generate the best returns operate across multiple dayparts and, in turn, generate higher average unit volumes. Depicted in the chart below, at $1.1 million, Potbelly’s average unit volumes are below all of its primary public peer competitors. Given the inherent unit economics of a Potbelly shop, we find the company’s premium multiple very difficult to justify even with the “growth” story as a backdrop.

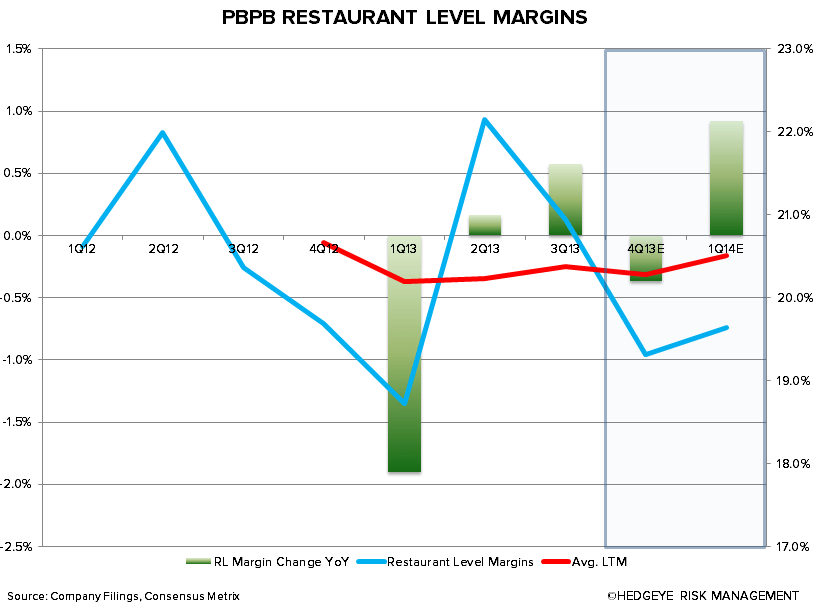

Restaurant Level Margins

Given the rapid projected growth rate of the company, PBPB will be facing downward pressure on restaurant level margins for the foreseeable future. On average, new Potbelly shops will open up with shop level profit margins in the high-single digit or low-double digit range. It will require nearly flawless execution on store openings to avoid being stymied by incremental margin pressure.

Low Returns

Relative to its competitive peer set, PBPB generates a very low return on assets.

Strong Balance Sheet and Cash Flow

PBPB is expected to have $48.87 million of cash and short-term equivalents on its balance sheet at the end of 2013 and is expected to generate approximately $7.8 million in free cash flow after allocating $31.16 million to capital expenditures in 2014. The company has not formally announced what it will do with its excess cash, but we can safely presume they will use it to fuel their self-funding model and accelerate new unit growth in the second half of 2014 and 2015.

Valuation

Per our comments earlier and the visuals from the charts below, PBPB is a very expensive stock that we, at the very minimum, find quite unattractive from a valuation standpoint.

Conclusion

As it stands, PBPB’s operating model has little room for error. To justify the current multiple, it needs to be clear that there is significant upside from current consensus EPS estimates. We don’t anticipate this coming to fruition and, with short interest comprising 15% of the float, it appears as though we are not the only ones.

Howard Penney

Managing Director