EVENTS TO WATCH OVER THE NEXT 24 HOURS

URBN - Earnings Call: Monday 11/18 5:00 pm

BBY - Earnings Call: Tuesday 11/19 8:00 am

HD - Earnings Call: Tuesday 11/19 9:00 am

DKS - Earnings Call: Tuesday 11/19 10:00 am

TJX - Earnings Call: Tuesday 11/19 11:00 am

COMPANY NEWS

TIF - Tiffany financial chief resigns

(http://www.retailingtoday.com/article/tiffany-financial-chief-resigns)

- "Tiffany’s chief financial officer, Patrick F. McGuiness, has resigned his position effective Nov. 27. The company’s EVP and chief operating officer, James Fernandez, will assume the position of CFO on an interim basis."

- "Fernandez has been with Tiffany’s since 1983. The board of Tiffany’s has authorized a search for a new CFO."

GOOG - Google Opening Showrooms to Show Off Gadgets for Holidays

- "Google Inc. is opening showrooms in six U.S. cities, promoting its latest products and stepping up retail efforts against Apple Inc. and Microsoft Corp. as the year-end holiday shopping season gets under way."

- “Called Winter Wonderlabs, the outlets feature products such as Nexus 7 tablets, Chromebook computers and Chromecast video-streaming devices, the company said on a new website yesterday."

- "Google is putting the showrooms at or near New York, Washington, Chicago, Los Angeles, Sacramento, California, and Paramus, New Jersey. The company is also building a barge in San Francisco Bay aimed at showing off new technologies."

AMZN - Report: Amazon has best price 80% of the time

(http://www.chainstoreage.com/article/report-amazon-has-best-price-80-time)

- "Amazon.com has the best price on products in its assortment about 80% of the time. However, the new 'Amazon Holiday Pricing Insights' analysis from pricing technology provider 360pi shows that Amazon does have weak spots…"

- "For example, once Home Depot decided to be price competitive on Oct. 26, they were instantly and dynamically able to beat Amazon prices on power drills. Meanwhile, tablets and televisions are the categories where a majority of retailers are either price competitive or closer to the mark than other categories, such as printers and video games, which show the least amount of price competitiveness."

- "Top retailers such as Best Buy, Wal-Mart, and Sears and Costco are less than 5% more, or better priced, than Amazon in televisions, for example. During the Oct. 16 – Nov. 14 period, Amazon had the lowest-priced tablets 68% of the time, which means retailers are currently beating Amazon with lower tablet prices 32% of the time."

KER - Kering Taps Eyewear Executive Roberto Vedovotto

(http://www.wwd.com/fashion-news/fashion-scoops/eyes-on-eyewear-7280621?module=hp-topstories)

- "Kering is putting a new focus on its eyewear businesses — and has tapped Roberto Vedovotto, formerly chief executive officer at Safilo Group SpA, who is to start work at Kering effective today, WWD has learned."

- "Kering president and ceo François-Henri Pinault has tasked Vedovotto with reviewing the French group’s eyewear strategy across all brands in order to optimize and further develop the business. His remit is to coordinate Kering’s efforts across its luxury and sport-lifestyle brands, which include Balenciaga, Stella McCartney, Boucheron, Puma and Volcom."

INDUSTRY NEWS

China Tops E-commerce Opportunity Study

- "When it comes to market opportunity for e-commerce, China occupies the number-one position, followed by Japan, the U.S., the U.K. and South Korea, according to a new global e-commerce study by A.T. Kearney…"

- "The Global Retail E-Commerce Index ranks the top countries in online retail, based on a 0 to 100 point scale. A.T. Kearney looked at 186 countries to determine the ranking of the top 30 countries. The index evaluates countries according to online market size, technology adoption and consumer behavior, infrastructure and growth potential."

- "Over the past five years, online retail has grown at a 17 percent compound annual growth rate, with growth particularly strong in Latin America (27 percent) and Asia-Pacific (25 percent), according to the study. Interestingly, India didn’t make the top 30 because of its low Internet penetration and significant infrastructure constraints."

- "China’s $64 billion online retail market will explode over the next five years to $271 billion, due to infrastructure improvements, increased Internet access for rural regions, rising wealth and customers’ growing predisposition to spend. China has the world’s largest population (1.36 billion), the most Internet users (517 million) and the most online shoppers (220 million), according to the study."

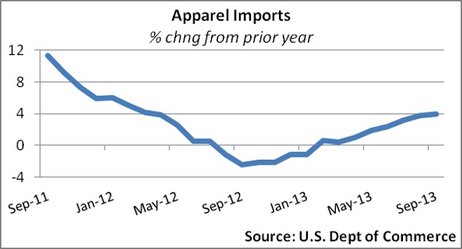

Apparel Beats Overall Import Growth in September

(https://www.sourcingjournalonline.com/apparel-beats-overall-import-growth-september/)

- "Total apparel imports (on a CIF basis) were $8.5 billion for the month, a 2.9% increase over September of last year and a drop from August’s $9.1 billion. Apparel imports grew faster than total goods and services imports, which increased 2.4%, due largely to increases in industrial supplies and automotive vehicles and parts."

Finally, Bangladesh Govt Sets New Minimum Wage

(https://www.sourcingjournalonline.com/finally-bangladesh-govt-sets-new-minimum-wage/)

- " Bangladesh’s government has finally agreed upon a new salary structure, effective December 1. Labor Minister Rajiuddin Ahmed Raju announced that the new minimum wage will be set at 5,300 taka ($68), a...77 percent increase."

What's Selling: Children's

(http://www.wwd.com/footwear-news/retail/whats-selling-childrens-7279736?module=hp-fn)

ITTLE’S SHOES, Pittsburgh

- Nina Kids Cassina

- Merrell Jungle Moc

- Stride Rite lighted shoes

Top trend: “People were really shopping for dual-purpose shoes at back-to-school time — shoes the kids can wear outside on the playground and with their uniforms,” said Justin Sigal, president of Little’s. “Now that the weather is getting colder, Ugg Australia, Kamik and Sorel boots are picking up.”

HARRY’S SHOES FOR KIDS, New York

- Naturino any style

- Stride Rite any style

- New Balance 990

Top trend: “Bright pops of color and rainbow colors are really hot for kids,” said Ivan Castro, store buyer and manager. “The colorful soles and combination of colors on the uppers are big for not just adults but kids, too.”

SESAME STEP, Miami

- Sperry Top-Sider Bahama and Cupsole

- Nina Kids Marnee

- Sam Edelman Fiona

Top trend: “Ballerinas are still big for us and so are the Sperrys,” said owner Eddie Quintana. “We’ve still had hot weather down here, so those categories are huge for us and controlling a lot of our business.”

HANSEL & GRETEL, Wilmington, Del.

- Jumping Jacks Anaa

- Livie & Luca

- Lelli Kelly Mary Jane styles

Top trend: “We do a lot of dress shoes at our location,” said owner Carol Harvey. “People like the Livie & Luca [label] because it has really well-made dress shoes for kids, and Lelli Kelly because of the soft soles.”