Here are the latest comments from our Sector Heads on their high-conviction stock ideas.

INVESTING IDEAS

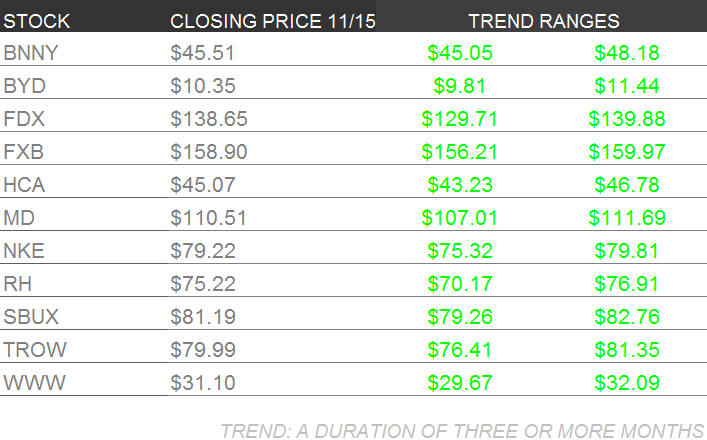

BNNY – Early this week (11/12) Annie’s announced a secondary offering of 2.5MM common stock shares (expected to close and settle on 11/18/13) which sent the stock tumbling around 5% on the week. Consumer Discretionary sector analyst Matt Hedrick expects fears associated with near-term dilution to subside and remains committed to his bullish outlook on the stock over the immediate and intermediate terms. The real story here continues to be the company’s advantaged organic portfolio and strong positioning for growth.

BYD – Gaming, Leisure and Lodging sector head Todd Jordan says September was a disastrous month in regional gaming markets, and Q3 earnings were crushed for Boyd Gaming and the other operators. However, Jordan sees October coming in much better – down low single digits versus down 9% in September. And, says Jordan, November should also improve from September and give investors more comfort with earnings. BYD has ample opportunity to drive margins as they remain 500-700 bps below the competition in many of its markets.

Longer term, BYD continues to generate huge free cash flow, despite the tough environment, and de-lever quickly. Upcoming catalysts include updates on the Penny Lane slot promotion, further meaningful tax relief from the State of New Jersey, and the roll out of BYD’s internet gaming platform in New Jersey.

FXB – European Macro analyst Matt Hedrick expects currency wars to persist, with continued devaluation for the USD and EUR. Hedrick says the British Pound should be the relative winner across both cross-trade relationships. Following the ECB’s unexpected decision last Thursday (11/7) to cut the main interest rate by 25bps to 0.25%, Hedrick also notes continued confirmation of a dovish bias from the Fed (see Yellen’s commentary before the Senate Banking Committee this week) as numerous ECB executive board members talked up the prospect of future rate cuts.

In contrast, the BOE policy discussion continues to set a hawkish tone: Hedgeye expects interest rates to be on hold over the medium term, with expectation for a hike over the longer term, and the asset purchase program target (QE) to remain unchanged. Both positions should strengthen the GBP/USD and GBP/EUR. Improving data out of the UK this week continues to suggest that the country’s growth profile will exceed most of its European peers and stoke the currency higher.

This week the BOE’s Inflation Report raised 2014 GDP estimate to 2.8% from 2.7%, the unemployment rate tick down 10bps to 7.6%, and CPI fell from 2.7% to 2.2% (deflation of this tax should aid consumer spending). We’re forecasting the GBP/USD to head to the $1.65 - $1.70 range over the intermediate term and continue to like the FXB exchange-traded vehicle for investors who want to be long the British currency.

FDX – In the aftermath of activist investor Dan Loeb’s Third Point Management announcing a stake in FedEx this week, Industrials sector head Jay Van Sciver hosted a Hedgeye Flash Call, bringing investors up to date on the stock. Van Sciver has been bullish on FDX for one year. So far, so good. See the complete write-up in our Sector Spotlight, below.

HCA – Healthcare Sector Head Tom Tobin says we will soon see how this craziness all ends with President Obama changing the rules of the Health Reform game midstream. It's unclear to us after his press conference if anything really changed at all. In order to keep his pledge that nobody lose their insurance who did not want to, Obama has reinstated those cancelled policies. Well... sort of, since state level Insurance Commissioners and insurance companies will have to figure out how to actually renew those cancelled policies.

When it comes to Hospital stocks and HCA, we have several drivers to the thesis: maternity, which has finally made its way back to 0% after 5 years of declines; Orthopedic and Cardiac Surgery (32% of revenues) returning to modest, but high margin growth; consolidation, and lastly, bad debt relief coming from the ACA. On the ACA, and healthcare.gov, it does appear traffic is dropping over the last week which we see as evidence that the backlog of frustrated shoppers is getting worked off.

MD – The Hedgeye Healthcare team ran a new analysis on our OB/GYN survey recently that showed that trends in maternity in the Northeast region remain weak, while growth in the Southwest is very strong. We believe this relates to differences in employment growth in the two regions, a key driver of our national forecast model. We remain bullish on Mednax at these levels.

NKE – Retail sector head Brian McGough recently wrote this following Nike’s analyst meeting: “The company remains maniacal in its quest to innovate. That sounds like a cliché when talking about Nike, because it’s all management, from the CEO on down, ever talks about. But in evaluating the product pipeline, it’s abundantly clear that literally no one can compete effectively with Nike without a painful outsized capital outlay.”

That proved true this week as Under Armour agreed to purchase the online training platform MapMyFitness for $150 million in an attempt to gain some traction in their battle to steal market share from Nike. Since, 2006 Nike has dominated the digital training space when it created Nike+ with Apple.

Nike has been collecting data through its Nike+ digital initiative, Nike Fuelband, and Nike Training Club (iPhone/iPad app) for years now. The company has found a way to reverse engineer that data in a way to both create and improve and of course innovate product. It’s almost like how Wal-Mart uses RFID to learn the shopping patterns of its shoppers. Nike can harness all that data and turn it into commercial opportunity, while building brand awareness and loyalty.

With this move, Under Armour can now control the message being sent to MapMyFitness’ existing 160+ million, and may win some converts. Yet, they lack the distinct advantage that Nike has developed over the past 7 years which allows them to understand the consumer in a way that nobody else can.

RH – The key to the Restoration Hardware growth story is the real estate transformation. More square footage and new product categories equals tremendous upside. To reach our +$8.00 in earnings estimate by 2018 the company must continue to streamline its supply chain in order to be able to efficiently supply the increased demand. Most people don’t know this about RH, but 90% of their product ships from distribution centers. That means that customers walk out of RH’s current retail stores with only 10% of the total product sold. The rest is shipped from the company’s distribution centers. That 10% number will likely increase as stores get bigger and non-furniture items (think kitchen) become a bigger part of RH’s business, but for the near term operating efficiency is key for the company.

At the beginning of November RH opened its sixth distribution center in Texas, and the company projects that it will have seven shipping hubs in its top markets by year end. This is important for a company that ships 20 foot dinner tables and 600 pound sofas to its customers across the US and Canada. The company currently charges a sliding scale flat fee for shipping and that weighs heavily on the gross margin. The charges collected in no way offset the shipping fees the company incurs. The company must, effectively scale their infrastructure as the top line continues to grow. We remain confident that they will.

SBUX – Starbucks finally concluded its packaged coffee quarrel with Kraft (KRFT) this week. The arbitrator ruled that SBUX must pay Kraft $2.8 billion to settle the dispute. Kraft will direct the net proceeds to Mondelez International (MDLZ). The number was fairly disappointing, in the sense that it came in at the high end of expectations. Starbucks CFO Troy Alstead was clearly unhappy with the decision, saying he strongly disagreed with the ruling and felt SBUX acted appropriately in ending its agreement with Kraft.

While analyst reactions were fairly mixed, the news turned out to be somewhat of a non-event. SBUX clearly has more than enough cash on its balance sheet to pay the damages. Restaurant analyst Howard Penney was relieved after the announcement, noting that the end of the dispute removes an overhang from the stock. While he was hoping the outcome would yield a smaller settlement, SBUX remains his favorite name in the restaurant space.

TROW – Senior Financials sector analyst Jonathan Casteleyn’s favorite asset management stock continues to be T Rowe Price which has one of the highest exposures to equity products (mutual funds and separately managed accounts) in the investment management industry. TROW drives 83% of its revenues from equity products and directly benefits from the emerging reversal in equity fund flows from redemptions last year in 2012, to subscriptions and inflows this year in 2013.

Shares of T Rowe Price have always traded at an industry premium on a forward P/E basis because of its high cash balance ($1.6 billion in cash on its balance sheet), strong free cash flow generation ($1.2 billion of free cash flow generation for 2014), and no debt; however, Casteleyn says shares currently are the cheapest they have been in three years, relative to the rest of the asset management group. Currently TROW shares fetch just a 12% premium to a group average forward P/E (a 3 year low) versus a 23% average premium since 2010.

Casteleyn says TROW is experiencing institutional outflow right now, coming from a handful of sovereign Asian wealth funds, and this has compressed the stock’s valuation. But Casteleyn says this is not a systemic situation; he expects TROW shares to unwind this discount and appreciate versus the rest of the industry.

WWW – We added WWW to our Best Ideas list on April 18th, as of Thursday the stock is up 34%. Our thesis hasn’t changed. The company has the best global reach in the industry and will continue to integrate the brands it acquired from PLG (Saucony, Stride Rite, Keds, and Sperry) into its industry leading global supply network. Management has done a good job curbing the streets expectations, but we’re not buying it. We think WWW is a 100+ stock over 2-years.

Sperry may grab headlines, but Merrell is still WWW’s biggest brand, accounting for about 20% of sales. After the company’s acquisition of the PLG brands, Merrell was largely ignored. After disappointing 2Q numbers, Wolverine hired Gene McCarthy to lead the Merrell brand – a massive positive in our opinion. He was the most eligible bachelor on the market and his resume speaks for itself - Nike, Reebok, Timberland, and Under Armour. McCarthy’s full influence won’t be felt until 2014, but we’ve seen some positive trends from Merrell lately. In Q3, Merrell put up a double digit growth rate due in large part to the strength of its outdoor brand. That strength was reaffirmed in the most recent Footwear News survey. Merrell was the leading the Outdoor footwear category. Of the nine shoe styles cited by footwear store managers and buyers across the nation as particularly strong this fall season Merrell had three on that list. Our thesis on WWW is focused on the global opportunities for the PLG brands, but strength in the Merrell brand only strengthens our conviction.

Macro Theme of the Week – QE: Too Big To Taper?

The Federal Reserve turns one hundred years old next month and looks set to mark its anniversary by delivering much, much more of the same. The looming confirmation of Janet Yellen as the next Fed chief gives new meaning to the sentiment “Many happy returns,” as she sets the table for the endless banquet of Quantitative Easing to continue unabated.

In case you forgot, the Federal Reserve Act of 1913 established the central bank and assigned it three key objectives: maximum employment, stable prices, and moderate inflation, as expressed in long-term interest rates. The Fed is supposed to achieve these goals through monetary policy and influence on interest rates.

Observers increasingly rant about the politicization of the Fed, but it could be equally well said that Washington has increasingly abdicated its responsibilities, facilitating – some would say requiring – that the Fed take control. Legislators and presidents alike have been happy to hand off the hot potato of economic policy to unelected academics, freeing themselves to get back to the basic business of governing, which largely consists of politicians sucking up to powerful constituents, while in turn encouraging wealthy lobbyists to suck up to them.

Two articles appeared in the press this week that shed light on problems within the Fed. The more widely read appeared in the Wall Street Journal (12 November, “Confessions of a Quantitative Easer”) but observers of economic policy should not miss Alan Greenspan’s piece in the latest Foreign Affairs (November/December 2013) endearingly entitled “Why I Didn’t See the Crisis Coming.”

Greenspan writes “irrational factors in economic decision-making” – broadly known among Dismal Scientists as “animal spirits” – are “hard to measure and stubbornly resistant to systematic analysis.” He then says “For decades, most economists, including me, had concluded that irrational factors could not fit into any reliable method of forecasting.”

This is a bit of a bombshell. The world’s most powerful central banker, whose tenure was bookended by the Crash of 1987 and the Crash of 2007, was aware of a whole body of data that impacts economic decision making, but didn’t incorporate it in his calculations because (a) it’s really hard to measure, and (b) no one else measures it anyway.

In retrospect, Mr. Greenspan now believes that “people, especially during periods of severe economic stress, act in ways that are more predictable than economists have traditionally understood.” We would stretch that statement and say that people behave irrationally – in contrast to received economic wisdom which has people acting in their own best interest – and that this irrational behavior, which is often a causal factor leading to periods of economic stress, can be modeled and even predicted in ways that economists never explored until recently: the world of serious economic research has embraced Behavioral Economics, perhaps out of the desperate recognition that traditional economic analysis could not deliver when it was most critical.

In the more widely-cited piece – and speaking of economic stuff that wasn’t working – readers of the Wall Street Journal got a full-bore apology this week from Andrew Huszar, now of Rutgers University business school, formerly of Morgan Stanley – and in between, the executive at the New York Fed charged with running “a wild attempt to buy $1.25 trillion in mortgage bonds in 12 months.”

We find Professor Huszar’s mea culpa confusing. He worked at the Fed for seven years then left “out of frustration, having witnessed the institution deferring more and more to Wall Street.” Faced with “regulatory capture,” where the regulators end up in thrall to the industry they are supposed to be policing, Huszar left the Fed and went to work for the industry itself. It strikes us as disingenuous that Huszar says he left the regulatory entity because he had lost faith in its ability to police Wall Street – and then went to work on Wall Street. Perhaps the subtlety of the message is lost on us.

Within a year, Huszar’s former employers were calling on him to return. The Fed swore that they had gotten religion and were committed “to a major Wall Street revamp.” Huszar “took a leap of faith.” That faith turned to particularly bitter disillusionment when Huszar realized “Wall Street had experienced its most profitable year in 2009, and 2010 was starting off in much the same way” – largely thanks to the largesse he was personally doling out to the banks. “Demoralized,” he writes, “I returned to the private sector.”

Don’t let our cynicism stop you from reading Professor Huszar’s piece in full. It’s well worth your time, if only because it appears to point to the willful blindness of an apparently well-meaning and intelligent professional (shades of Ben Bernanke? Janet Yellen?). It was painfully obvious from the outset, even before the Fed started its QE program, that Washington was gearing up to bestow enormous quantities of cash on the financial sector, and that everyone else was going to get stiffed quite royally. One didn’t need a PhD in economics to recognize that, when then-Treasury Secretary Hank Paulson told Congress they had to give him nearly one trillion dollars for TARP and that there was to be no Congressional oversight, no audit, no reporting, and no intervention even by the courts, we were headed for the abyss.

The Fed’s bond buying program has been the equivalent of setting up a printing press to turn out $100 bills, with the input tray inside the taxpayer’s pocket, and the output tray inside America’s largest private financial firms. But as Congress and the President have all but shredded any remnant of fiscal responsibility, the burden of running America’s economy defaults to the Fed. Given the extent to which our elected officials have catered to America’s most powerful economic interests, we don’t see how we can demand that the Fed behave differently.

Huszar quotes PIMCO’s Mohammed El Erian suggesting “the Fed may have spent over $4 trillion for a total return of as little as 0.25% of GDP.” Larry Fink is CEO of BlackRock, a firm with about four trillion dollars under management – almost to the penny the same amount currently held on the Fed’s balance sheet. Fink says Fed policy has wrought “bubble-like” conditions in the financial markets. Oh, and there’s this tidbit: 0.2% of America’s biggest banks “now control more than 70% of the US bank assets.” Are you worried yet?

Hedgeye CEO Keith McCullough thinks you should be, and with Yellen testifying explicitly that “it ain’t over till it’s over – and I say it ain’t over,” Hedgeye’s analysis of Fed policy stands out sharply.

This week on Hedgeye TV, Keith explained “Why the Fed is Failing.” The Fed’s “dual mandate” comprises price stability, and maximum employment. Hedgeye’s analysis of 50 years of bond market data shows price volatility in the bond market is at its widest point ever. Bond yields have shown corresponding volatility. Between the moment the market expected the Taper, and the realization that there was to be no Taper, bond yields experienced a swing of over 50%. This is the Fed’s version of “price stability” – in the “riskless asset,” no less.

What is a Fed Chair Yellen likely to do? Her recent comments indicate that she would extend the current bond purchase program, with a hint that she may deepen it. For those who believe that the solution to America’s economic plight is to continue to print money, this is a Good Thing. For us at Hedgeye, this continued dollar debauchery will push back economic growth and weaken America’s standing internationally.

We offer two concrete concerns around the policies Yellen is likely to promote. First, Yellen may out-dove the “moderate” Bernanke. She could do this by moving the goalposts on the Fed’s policy signals. Instead of a 6% unemployment target, for example, Yellen could insist on a 5-handle. That takes care of the “maximum employment” leg of the dual mandate. As to price stability, among risks associated with the Taper, no one is mentioning the risk of a massive write-down in government agency securities.

This is a bit of a long shot, and has a few moving parts. But if the past few years have taught us anything, it is that no catastrophe, no matter how unlikely, should be dropped from consideration.

The Fed is buying $85 billion a month worth of bonds. Half of that goes to buy Treasurys; the other half goes to buy government agency mortgage-backed bonds. As Professor Huszar points out, until he started the New York Fed’s buying program, the Fed had never in its history bought a mortgage-backed security. Now, these purchases are the order of the day – to the tune of $40 billion-plus a month. And here’s a little secret: these bonds don’t trade.

Treasury bond portfolios are marked to market for valuation, with real-time prices from the world’s largest and most liquid securities market. Mortgage-backed bonds, by contrast, are not liquid for sellers, and most of the largest managers buy bonds from the agencies – Fannie Mae and Freddy Mack – intending to hold them to maturity. They value these portfolios on a price-paid basis – which makes sense if they will never be sold, and assuming no risk to maturity. On that score, note that Treasurys are backed by the full faith and credit of the US government, while agency bonds are a “moral obligation” of the federal government. This is a lot like “full faith and credit,” until someone decides it’s not. Should that day ever come, look out below.

Today, in the face of a massive shift out of bonds, the major holders of mortgage-backed issues are mirroring the behavior of the banks at the height of the financial crisis: everyone knew that a huge portion of the mortgages they held were never going to be paid off, but no one was willing to write down their portfolio. Indeed, if any one bank had dared charge off its bad mortgages, it would have forced the others to follow suit. The entire sector stood pat, aided and abetted by Congress and the very regulators who were supposed to be keeping them honest. Ultimately, the banks were bailed out by the taxpayer. Can you guess who would bail out the PIMCOs and BlackRocks of the world, should a similar crisis erupt in the mortgage-backed agency market? Have you forgotten that the Fed is already bailing them out, to the tune of over $40 billion a month?

It is unambiguous that the Fed’s greatest impact on the markets is an increase in volatility. The QE shuffle has so far roiled the gold and fixed income markets with waves of volatility. And equities are not immune. Indeed, they could be next – just as investors have switched gears, sucking money out of their bond funds and putting it into equity funds. Hedgeye’s macro analysis sees a pattern of higher lows in the VIX, a key measure of market volatility, indicating an increasing probability of an upside volatility breakout – which could drive at least a 5% correction in the S&P 500.

The Fed’s ongoing policy to trash the dollar has had the effect of inflating prices of things priced in dollars. This policy has most notably sent the equities markets through the roof. But remember that actual economic growth is “priced” in real terms. A factory that increases productivity by 2% a year can not “put it on margin” to turn that into a 4%-10% annual gain. Indeed, we are suffering the aftermath of an economy whose growth over more than a generation was increasingly driven by borrowing, borrowing, borrowing.

It appears that the Fed really believes it is helping the economy by guaranteeing that the prices of mortgage-backed bonds remain unrealistically high – and using our money to do so. What is really going on is that asset prices are diverging from fundamental asset values, to the extent that markets risk becoming completely untethered from reality. Into this morass treads Janet Yellen, who looks set to launch a new round of aggressive doveishness. We think this risks trashing what’s left of the dollar. Maybe shutting down the government wasn’t such a bad idea.

Sector Spotlight – Industrials: FedEx, Special Delivery

News that activist investor Dan Loeb and his Third Point Management hedge fund had taken a stake in FDX sent the shares higher this week, as investors looked for him to catalyze the company’s restructuring program, which has shown first signs of promise.

Industrials sector head Jay Van Sciver has been consistently bullish on FDX for a year; on the news of the Third Point stake he presented a Hedgeye Flash Call titled “FDX: Delivering After A Year In Transit?” to bring investors up to date on what is still a bullish call. Van Sciver touched on key points in the FDX story, including: Long-term cycle drivers, Express margin opportunity vs. execution, competitive risks, industry headwinds, FY2Q set-up, and the case for valuation and margin of safety for FDX holders.

Van Sciver’s initial bull case keyed off of two basic concepts. The first was the valuation of FDX’s Express division – at the time, the stock price was below $100. Van Sciver said this reflected the value of FedEx Ground, and essentially valued the Express business at zero. The second was management’s stated objective to tighten controls and improve shareholder value, an initiative that seemed to lack initiative, with management continually returning to loss-leader global efforts to capture market share, among other distractions. Van Sciver said this created a compelling case for an outside activist investor, particularly one who could work with management to push for efficiency and profitability. With the breaking news that activist investor Dan Loeb’s Third Point Partners has taken a stake in FDX, this begins to look like a possibility, if not yet a reality.

Why look at the company now, when the thesis appears to be working? The stock trades over $130 a share, a bona fide activist has taken a stake and is publicly discussing the succession from CEO Fred Smith, one of the true corporate heroes of the modern world. Say Van Sciver, it ain’t over till it’s over – and it ain’t over.

True, the Express division is no longer free. But Van Sciver argues that shareholders should still have a long profitable road ahead, and should be planning how to navigate, as there are likely to be some downs as well as ups over the next 2-3 years.

Van Sciver’s work indicates the Ground business itself could still be worth $100 – making Express not free, but still cheap. In the immediate term, and considering possible macro risks of a market correction, Van Sciver says shareholders should evaluate the risk that Express might go back to being “free” in FDX’s share price. Van Sciver notes that when markets break down, investors tend to rush to sell what they can, rather than what they should.

For investors with a 3-5 year time horizon, Van Sciver says FDX should be able to deliver on a program for substantially higher share prices. But there could be bumps and dips along the way, he cautions, and today’s analysis is an opportunity to start to prepare.

On the ongoing restructuring of the Express division, Van Sciver says there is only one full quarter of data – hardly conclusive – and management appears to have “pulled some levers” to roll restructuring related cash into Q1. This includes deferring salary increases and other expenses into the second quarter to keep the momentum of the restructuring going strong. Van Sciver says FDX should be able to deliver on the full promise of the restrucdture, but there will have to be payback for the rolled-forward items, which could come as soon as the next couple of quarters. This would not indicate failure, says Van Sciver, but that levers need to be reset, and could make it easier to buy on earnings-related dips.

As with many of the cyclical companies in his sector, Van Sciver cautions that earnings numbers and multiples may prove counter-intuitive. Thus he says Express division margins remain at multi year lows and lag their competition. The restructuring is only into its second quarter, so it’s a bit early to get skeptical. To the contrary, says Van Sciver, FDX is contending with a macro situation characterized by bloated corporate inventories, and notes that people don’t pay extra to ship what they already have in excess in the warehouse. Recent government statistics do not show much improvement in the inventory situation, and Van Sciver says this is typically a good entry signal. Shippers such as FDX tend to ride highest when overall inventory-to-sales ratios are low – clearly that is when companies need to ship the most. In trough periods shippers tend to underperform, and Van Sciver says that on this metric, with the industry cyclically depressed, FDX is very much flashing an entry signal.

The other big news in the world of door-to-door delivery is, of course, the announcement that Amazon will use the US Postal Service for Sunday deliveries. The USPS is in desperate straits, and the AMZN contract is nowhere near big enough to bail them out. But it could present an opportunity for FDX and others in the group, as the USPS will likely not be able to handle all of AMZN’s business.

Van Sciver points out that the USPS has one asset that no one else can touch: your mailbox. But their delivery expertise is concentrated on small packages. For larger deliveries the USPS will likely branch out to a “co-petition” model, farming out portions of their AMZN work to shippers who can handle larger and more complex deliveries. Van Sciver sees the USPS contract as an expansion opportunity for the entire industry and makes the observation that, as the non-union provider, FDX will have a cost edge.

Finally, what about the activist thesis?

Loeb has stated publicly that he is not seeking Smith’s ouster. But at age 69, the former Marine may welcome a competent outsider to help streamline the operation for his successor. This is likely to be a patient and thoughtful game, not a public dust-up resulting in greenmail. Investors looking for a fight should tune in to the WWF. Investors looking for a solid company with a good long term outlook should keep an eye on FDX.

Conclusion

Van Sciver says “it gets a little messy” going into the next couple of quarters, especially after management raised expectations with a strong showing in Q1. He counsels leaving room to buy patiently, perhaps over the coming year as resetting expectations after a strong Q1 could provide buying opportunities.

Van Sciver says the long-term thesis remains largely intact and he continues to see the potential for margin expansion in the Express division. The market is likely to reward continued progress with higher stock prices as the company shows it can deliver.

On the risk side, pulling the financial levers in Q1, even though done transparently, creates risk if the market has already priced in most of the success of the restructuring. In that case, even a simple reset could be seen as a backtrack and could hurt shares in the short term.

As to the activist card, it is too early to tell what impact Loeb might have on the future shape of the company, though on the margin his presence should at least keep management more focused on the restructure and less distracted.

Van Sciver says he would prefer “a smaller downside. I liked the shares better at under $100, when Express was essentially free, and there was less risk in the stock.” The fact remains that he did like it there. He liked it very much there, and he told you so. No long-term thesis plays out without disruptions, but FDX is working. Says Van Sciver, as long as the profit improvement plan continues to deliver, there should be plenty of upside left for patient investors.

Investing Term – Industrials

Speaking of Jay Van Sciver, the Industrials sector includes companies that manufacture industrial supplies and / or provide industrial services. This includes machinery used in construction, rail and highway building, agriculture and mining, as well as companies in the aerospace and defense area, air freight, and heavy and light electrical equipment, just to name a few.

The sector, formally known as the “Industrial Goods Sector,” tends to be largely driven by macroeconomic factors, particularly by demand for construction – both residential and commercial – and manufactured goods. Since many of these are largely discretionary purchases (a new house, a car, a refrigerator) macro factors and consumer confidence play an important role in the performance of these companies. As they are tied to economic cycles, Industrials tend to underperform when the economy is weak – especially when confidence is poor. As a general rule, Industrials as a group tend to lose more than the broad market averages, such as the S&P500, in down markets. In up markets, characterized by greater confidence, the group may get ahead of the broader averages.

Depending on whom you ask, Industrials either do generally about as well as the broad averages over time, or they do somewhat better. Hedgeye’s Van Sciver notes that the cyclicality of the group gives a key on how to invest. By their nature, Industrials are not a high growth group. People are either building houses, or they’re not. They are either mining iron ore, or they’re not. In growth sectors – Tech, for example – a high PE ratio indicates that the market is looking for continued growth acceleration. In the Industrials group, it often signals a top, as companies get bid up when they make more money – but they only make more money when their cycle nears its peak. Van Sciver says all other things being equal, the Industrials are best bought when they look worst, and best sold when the world is most enthusiastic about them.

Sometimes it’s easier to come up with a rule than to stick to it. At Hedgeye we believe that a repeatable process is the foundation of investing success. And of course we recognize the other fundamental rule of investing: that the rule is going to change.

- By Moshe Silver

Moshe is a Hedgeye Managing Director and author of the Hedgeye e-book Fixing A Broken Wall Street.