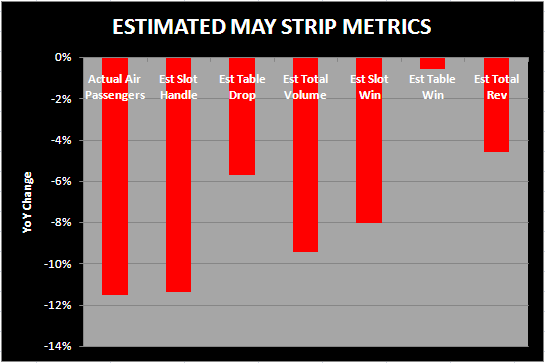

Low hold on slots and tables in May 2008 should allow the total revenue decline in May 2009 to look better than the 11.5% decline in McCarran airport traffic. Assuming normal holds on tables and slots, we project that Strip gaming revenue will decline only about 5%. In terms of YoY revenue change, May could be the best month since September 2008. As a refresher, gaming revenues declined 16% in April 2009 which was the 7th consecutive double digit monthly decline.

Before we get too excited though, our sources indicate that June looks a little weak and the hold comparison is a little challenging. Las Vegas is not yet out of the woods.