Long GBP/USD (via the etf FXB)

Our bullish call on the British Pound remains, an anchor of our Q4 2013 Macro theme of #EuroBulls presented on 10/11/13. (Click here for our previous note “Get Long the Pound”)

We’re buyers of the cross above our TREND support line of $1.58 and long term TAIL support line of $1.56. We could see the cross heading to the $1.65 - $1.70 range over the intermediate term.

In short, we expect currency wars to devalue the USD and EUR, and expect the British Pound to be the relative winner across both crosses. Here are some updated developments since the ECB unexpectedly decided last Thursday (11/7) to cut the main interest rate by 25bps to 0.25% that we think will boost our #PoundBullish call:

- Continued signs that Bernanke/Yellen will burn the Greenback via delaying the call to taper (likely pushed out to March 2014); a very dovish Q&A from Yellen today (11/14) before the Senate Banking Committee suggesting the call to taper pushed further out.

- Members of the ECB governing council suggesting further policy easing measures (since the cut):

- ECB Executive Board member Peter Praet said negative interest rates could be adopted or assets purchased from banks if needed.

- ECB Executive Board member Joerg Asmussen said that depending on how inflation develops, the central bank has not reached the lower bound on interest rates. He added that while he is wary of such a move, the ECB could also push the deposit rate into negative territory.

- ECB Executive Board member Benoît Cœuré said that the central bank can further cut interest rates and provide the banking system with additional liquidity.

- Austria’s Central Bank head and Governing Council member Ewald Nowotny said that the central bank's main concern is stagnation, not inflation. He added that unlike the Fed, the ECB had not yet reached the lower zero bound on interest rates.

In contrast, we expect sober hawkish policy from the BOE. The UK was the first to issue austerity, which we think will continue to boost its growth profile above most of its European peers. Improving economic data (more below) continues to confirm this position. On policy, we expect interest rates to be on hold over the medium term, with expectation for a hike over the longer term, and the asset purchase program target (QE) to remain unchanged. Both positions should strengthen the GBP/USD and GBP/EUR.

Improving UK Data This Week:

BOE’s Inflation Report-

- brought forward the likelihood of 7% unemployment rate to Q3 of 2015

- raised 2014 GDP forecast to 2.8% from 2.7%

High Frequency Data-

- UK Retail Sales 1.8% OCT Y/Y vs 2% SEPT

- UK ILO Unemployment Rate 7.6% SEPT vs 7.7% AUG

- UK Jobless Claims Change -41.7K OCT vs -44.7K September

- UK PPI Input -0.3% OCT Y/Y (exp. 0.1%) vs 0.9% SEPT

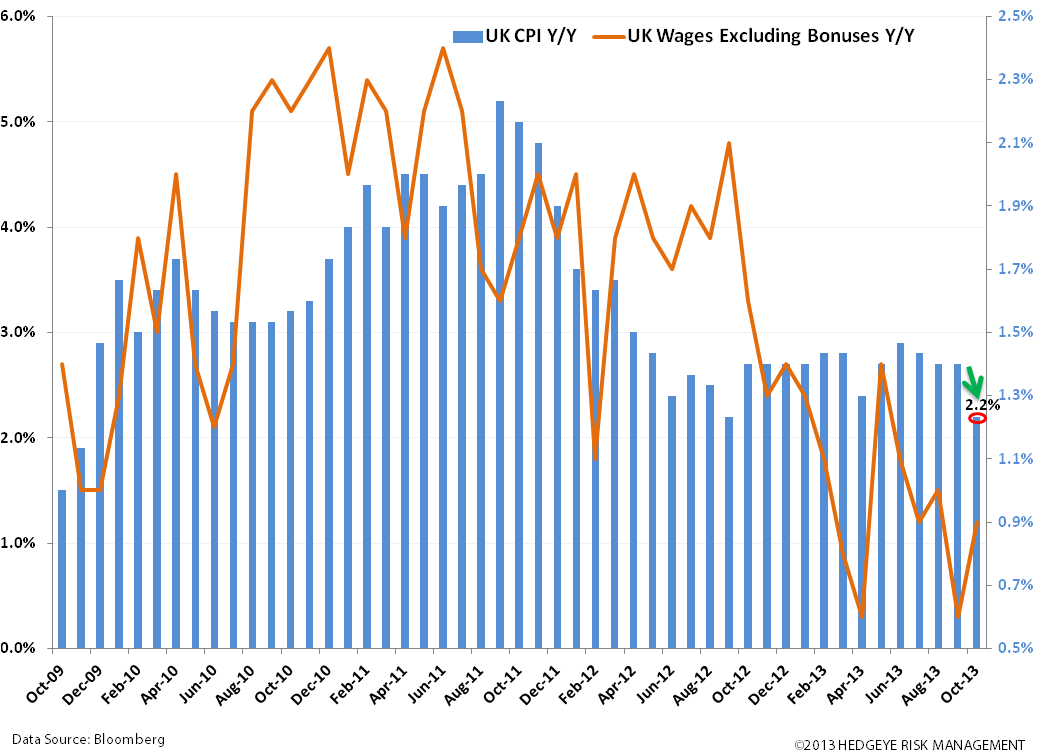

- UK CPI 2.2% OCT Y/Y (Exp. 2.5%) vs 2.7% September. We expect this move downward in inflation to aid consumer spending.