A look under the hood

Position: No active position; bullish bias

The nose dive of the Norwegian stock market (OBX Stock Index) on 6/17 in the wake of the Norwegian Central Bank's decision to cut the overnight deposit rate 25 bps to 1.25% peeked our interest as an outlier. The market's reaction to the cut, closing down 4.97%, appeared bearish, yet in a broader context the close didn't look as harsh: (1.) the cut came unexpectedly as economists predicted that the Central Bank would first consider a cut in August, and (2.) most of Western and Eastern Europe also sold off on negative US-centric news, including increased fears of the expansion of the US government balance sheet, the threat of near to immediate-term inflation, and Obama's plan to restructure the financial industry.

While Wednesday's close was bearish, the stock market is up 31.3% YTD and we believe the country sets up nicely from a fundamental standpoint. Being outside of the EU, Norway has the ability (and some say luxury) to better maneuver its economy through monetary policy. With economies in contraction throughout Europe, it's become increasingly apparent the challenges the ECB faces in affecting policy for varied economies. In contrast, Norway's control over interest rates and currency levels has allowed it more flexibility to manage its economy. [From an autonomous perspective similar considerations could be made for Sweden (via the etf iShares EWD) and Switzerland (EWL), which we had in our portfolio on the long and short sides respectively this year.]

Fundamentally, Norway looks relatively healthy compared to some of its European peers. Already lower interest rates and stimulus measures have encouraged shoppers to spend, confirmed by retail sales rising 1.4% on a monthly basis in April and consumer confidence improving. Inflation rose to 2.9% in May year-over-year and is expected to average 2.5% this year before pulling back to 1.75% in 2010 according to the statistical office. The mainland economy (which excludes oil, gas and shipping) is forecast by Norges Bank to contract 1.5% this year and return to grow of 2.5% next. We'd be quick to point out the prospect of stagflation, yet Norway's rate of GDP decline is manageable, especially as the economies of the Eurozone and Sweden, its main trading partners, improve.

Playing to its Strengths: Oil & Gas

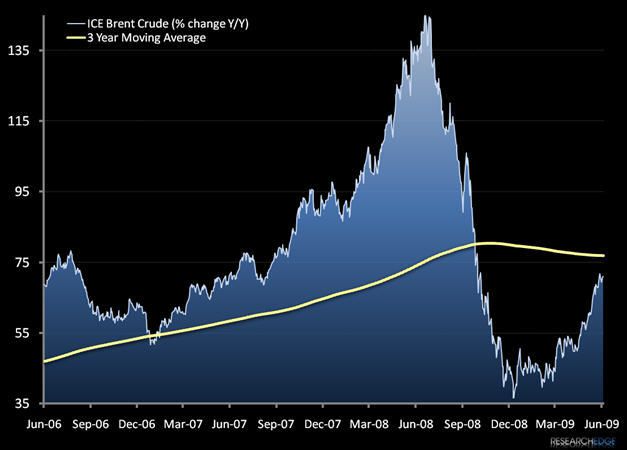

Norway's economy benefits from its rich off-shore oil and gas fields. Norway's petroleum industries account for ~23% of GDP, close to 50% of exports, and about 31% of government revenue in 2007, according to the latest IMF paper under the listing "Summary of Norway's Transparency Practices for Petroleum Revenue Management". If oil could sustain this level or better it would be decidedly bullish for Norway's economy as both an exporter and beneficiary of oil and gas royalties. The chart below illustrates the prospect of this price level for Brent based on a three-year moving average. Oil's YTD upward move of ~55% has certainly helped to propel the stock market to over 30% YTD, while neighbor Sweden stands at 17.5% year-to-date, and export-giant Germany's stock market (DAX) is up less than 1% YTD, as a comparison.

Today Royal Dutch Shell Plc, Europe's largest oil company, said it discovered a natural gas bed in the northern Norwegian Sea estimated to hold 10 to 100 Billion standard cubic meters of gas. While the discovery isn't particularly noteworthy considering Norway's net gas output was 99 Billion cubic meters last year, should Norway supply Europe's demand for natural gas it would have major geopolitical implications. You'll recall that we've been tracking the rising geopolitical tension between Russia and Europe over natural gas, which hit a crescendo over the New Year when Gazprom shut off supply to Ukraine and limited gas through Belarus (two main transit routes to Europe) that led to reduced capacity throughout Europe. The move, which disturbed many (esp. following Russia's invasion of Georgia), encouraged great debate among the European Commission to find an alternative to Russian natural gas, in short, to bypass Russia's political leverage over gas. Debate has included resumed talks of LNG capabilities, increased investment in renewable technology such as wind harvesting, and alternative pipelines to bypass Russian territory such as the Nabucco project, yet talks (and action) have stalled due mainly to price: Russian gas is still the cheapest option by and large.

Conservative Banking Practices

The historically conservative lending practices of Norwegian banks, focused more on prudent products and domestic loans rather than exotic credit products and global reach, has helped them not only weather the recessionary environment, but better position themselves for future lending. Despite leverage to Icelandic banks and customers, by and large the conservative nature of Norwegian banks has favorably positioned them. We believe this may encourage Norway to outpace its Eurozone peers on a recovery basis.

Managed Economy

Norway's economy has a unique blend of free market and state controlled enterprise. The latter is concentrated in its main industries, including: petroleum sector (StatoilHydro), hydroelectric energy production (Statkraft), aluminum production (Norsk Hydro), Norway's largest bank (DnB NOR), and telecommunication provider (Telenor). Norway has a very manageable population of less than 5 Million and due to the historic wealth of the country (Norwegians have the second highest GDP per-capita after Luxembourg), it has not seen major economic swings-such as an extensive housing bubble or excessive amounts of foreign debt-that have plagued some of its European peers.

Despite this positive fundamental set-up, and to the dismay of investors, neither Norway nor Scandinavia has an ETF or liquid product to get long the country. StatoilHydro (STO) currently trades on the NYSE and could be an oil play for us as we get more conviction on a longer term trend.

Matthew Hedrick

Analyst