This note was originally published at 8am on October 31, 2013 for Hedgeye subscribers.

“One day everything will be well, that is our hope. Everything’s fine today, that is our illusion.”

-Voltaire

In German folklore a doppelganger is literally a paranormal double of a living person. More contemporarily, the word doppelganger is used to identify a person that closely resembles someone else either physically or behaviorally. As an example, some people have suggested that my doppelganger is Russell Crowe.

As it relates to the Federal Reserve, the biggest question facing investors currently is whether Janet Yellen will be a doppelganger, in terms of policy and communication, of current Chairman Ben Bernanke (more commonly known as The Bernank). Practically speaking, copying Bernanke’s behavior is likely to mean a continuation of QE Infinity.

Keith had some colorful comments on Fox Business last night as it relates this idea of QE Infinity. The video is attached in the link below and Keith’s comment begin at around the 3:00 mark. As Keith notes, the biggest issue is that the Fed is confusing the market which has dramatically heightened interest rate volatility this year.

Paul Singer from Elliott Management made a similar statement in his letter to investment partners yesterday where he wrote:

“QE Infinity” has so distorted the prices of stocks and bonds that nobody can possibly determine what the investing landscape would look like, or what the condition of the economy and financial system would be, in the absence of Fed bond-buying.”

This is indeed the issue, namely that the economy and investors have become so accustomed to abnormal interest rate policy, that they have an incredibly difficult time determining what normal is anymore. Sadly, the new normal appears to be to wait for the Fed’s next whisper to the Wall Street Journal’s Jon Hilsenrath.

To be fair, for those that are into reading Federal Reserve tea leaves, there was communication other than whispers to Hilsenrath yesterday. Specifically, in its statement the Federal Reserve made three changes:

- This clause was removed, “the tightening of financial conditions observed in recent months, if sustained, could slow the pace of improvement in the economy and labor market”;

- They changed ”that economic activity has been expanding at a moderate pace” to “generally suggests that economic activity has continued to expand at a moderate pace”; and

- They removed the “some” from this statement - “Some indicators of labor market conditions have shown further improvement”.

Maybe it is just me, but I’ve been reading English for a long time now and I have no idea what the implication is of those changes.

The fact is that the bogey that remains out there is 6.5% unemployment and if we take their word then the Fed will:

“. . . keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that this exceptionally low range for the federal funds rate will be appropriate at least as long as the unemployment rate remains above 6-1/2 percent.”

Although, even there, The Bernank has been quite dodgey as he has at times alluded to 7% being the bogey for altering monetary policy and other times suggesting he would lower the bogey to 6%. But if we accept the current 6.5% target, QE Infinity is likely to continue at the rate of $85 billion, give or take, for the for seeable future.

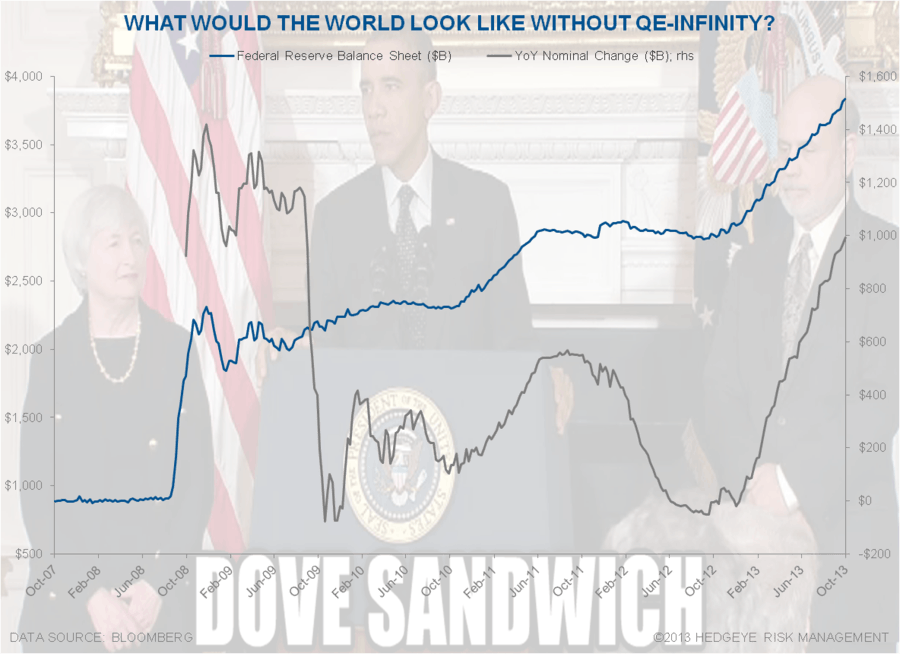

In the Chart of the Day, we’ve highlighted the growth of the Federal Reserve balance sheet since 2008 as a result of QE Infinity. In total, the Fed is almost at $4 trillion in assets on its balance sheet. Not to be the alarmist, but another reason that we may be in the low interest time zone for a lot longer than we realize is because of interest rate risk associated with the Fed’s balance sheet.

Ironically, some pundits (we won’t name names) have commended the Fed under Chairman Bernanke for being transparent and great at communicating. Sadly, it doesn’t take much more than the last 24 hours to understand that a) the Fed is as bad at communicating as ever and b) this is why investors are so confused. Frankly, we see no reason to believe that Yellen will be anything but Bernanke’s doppelganger on the communication front . . . and so the confusion will go on.

Sadly for stock operators, this confusion has led to an environment in which fundamentals for companies are, at times, ignored. As an example, let’s look at both earnings and sales results for SP500 companies:

- Sales: 60% of companies that beat sales estimates subsequently outperformed the market to the tune of 3.7% on average. The other 40% of companies that beat sales estimates underperformed the market over the subsequent 3-days by an average of -3.8%. Subsequent performance for companies missing Sales estimates was similarly mixed.

- EPS: 56% of companies beating EPS estimates subsequently outperformed the market by ~3% on average while 44% went on to underperform the market by an average of -4.1%. Subsequent performance for companies missing EPS estimates was similarly mixed.

In a nutshell, stock performance has had very little relation to fundamental performance in 2013. More simply, it has been a structurally tough year to isolate Alpha. But even there no one should be surprised, because it is a macro driven market. And if you don’t do macro, macro will do you.

Our immediate-term Risk Ranges are now:

UST 10yr Yield 2.47-2.60%

SPX 1755-1771

VIX 12.85-14.92

USD 79.21-81.16

Brent 108.86-111.27

Gold 1327-1363

Keep your head up and stick on the ice,

Daryl G. Jones