Note this a summary of our current thoughts on TWTR. We go into far more detail in our Blackbook. Ping sales@hedgeye.com for more information.

THESIS SUMMARY

- HOLES IN THE BUSINESS MODEL: TWTR’s current business model has a limited runway for growth given headwinds we’re seeing across the main levers in its business model

- CONSENSUS ESTIMATES ARE AMBITIOUS: . Our concern is mostly on 2H14 and 2015, which is when we expect revenue growth to slow precipitously.

- TWTR PRICED BEYOND PERFECTION: We thought the $26 IPO price was lofty, $43 is beyond reason, and well in excess of anywhere FB or LNKD have ever traded on a P/S basis.

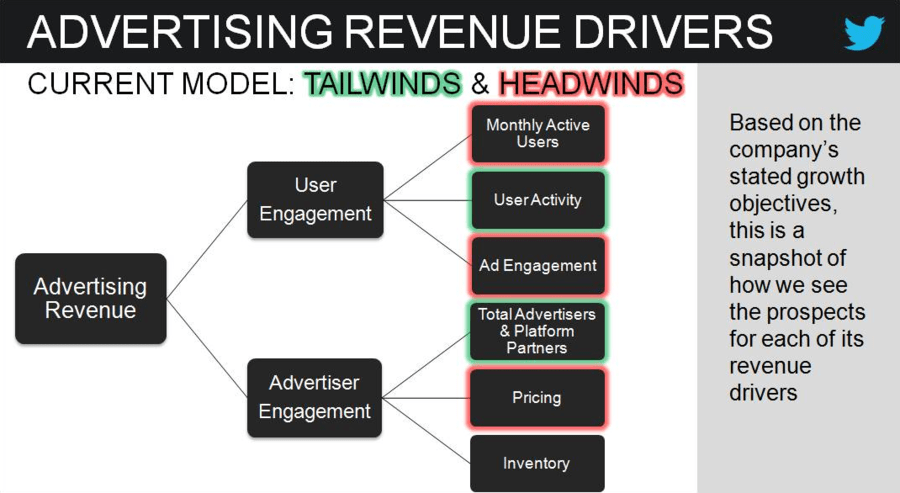

HOW TWTR MAKES MONEY

TWTR’s revenues are sourced primarily from advertising, which is predominately US (~75%), and “substantially all” of those revenues are derived from ads that users engage with. Those ad engagements, and resulting revenues, are driven by a combination User and Advertiser Engagement.

- User Engagement: driven by the number of users on their platform, their level of activity on the site, and the rate at which they engage in ads.

- Advertiser Engagement: this simply a function of the number of advertisers & size their ad budgets, and the price & supply of ad inventory.

Below we weigh TWTR’s growth prospects against its stated growth priorities and the headwinds/tailwinds facing its business model.

HOLES IN THE BUSINESS MODEL

In the diagram above, we highlight where we see emerging headwinds/tailwinds in TWTR’s business model; most of which comes on the side of user engagement, which is where we will focus below. In short, slowing US user growth combined with stagnant-to-slowing ad engagement is a recipe for a marked slowdown in revenue growth through 2015 (see our Blackbook for more detail). Summary bullets below

User Engagement: Headwinds/Tailwinds

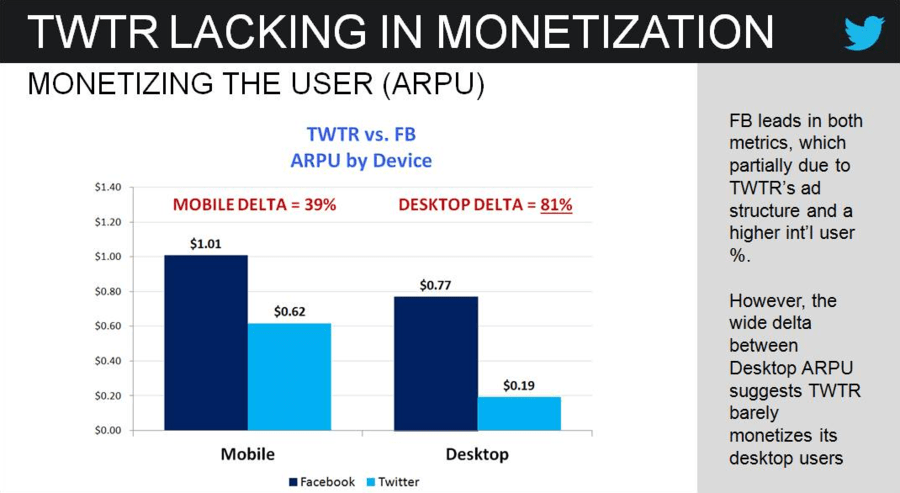

- Monthly Active Users: TWTR’s US growth has been slowing, and management expects this to continue. The runway for US user growth may be limited here given that Twitter’s total user penetration levels (including inactive users) may be much higher than its monthly active user metrics suggest. The main issue is that US users are far more lucrative than international users (almost 10x higher in terms of ARPU), meaning domestic user growth trends will have a disproportionate impact on revenues.

- User Activity: Anecdotally, we see this as a tailwind in terms of management’s efforts to drive more content on its platform. However, we are not sure it will be if enough to drive meaningful growth in total user activity, especially in light of slowing US User growth

- Ad Engagement: A deeper dive into TWTR’s financials suggests that the company is barely monetizing it desktop users (especially in relation to FB), which we belief is due a poorly designed user interface (more detail in our Blackbook). We believe it’s recent surge in ad engagements has been driven primarily by increasing supply, which we suspect was due mostly to extending its desktop ad products to its mobile application. That said, TWTR’s only option for driving supply growth on mobile is to introduce new products, which could push users away at the same time. So as ad inventory growth slows, TWTR’s revenue growth will slow with it.

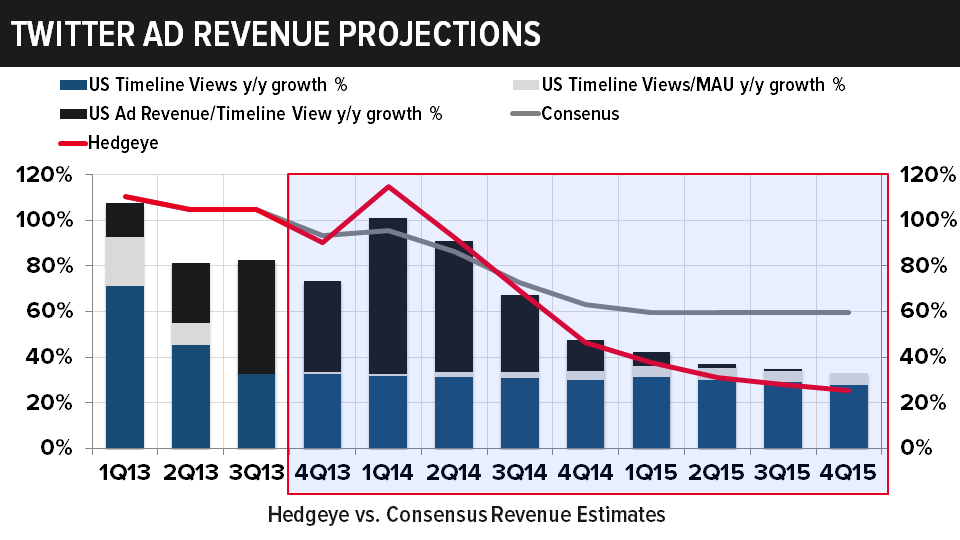

CONSENSUS ESTIMATES ARE AMBITIOUS

Consensus is expecting revenue growth of 80% and 59% in 2014 and 2015, respectively. Our concern is mostly on 2H14 and 2015, which is when we expect revenue growth to slow precipitously. Reason being that the tailwind from increasingly mobile ad supply will likely be fully annualized by that point, which means that the company’s revenue growth will be tied to new advertising products, which we expect to have a limited impact, and US user growth, which we expect to wane unless TWTR takes a more active approach to recruitment.

TWTR PRICED BEYOND PERFECTION

At $43, TWTR is now trading at close to $30 billion market cap on a fully-diluted bases. That puts TWTR valuation on a P/S basis well in excess of both the current and peak P/S multiples for either FB and LNKD.

it’s important to note that the trajectory of its share price and multiple expansion will be tied to its forward growth expectations, which are currently see as lofty into 2015. We believe that TWTR could trade as low as $25.00, which is 11x our 2015 Revenue Estimate of $1.57 billion.

Once again, this is the summary version of our thesis, and there is much more supporting data behind this analysis than what is shown above. If you would like to run through the analysis in more detail, please let us know.

Hesham A. Shaaban, CFA