COMPANY NEWS

JCP - J. C. PENNEY COMPANY, INC. PROVIDES UPDATE ON CONTINUED PROGRESS OF TURNAROUND

(http://ir.jcpenney.com/phoenix.zhtml?c=70528&p=irol-newsCompanyArticle&ID=1873694&highlight=)

JCP Q3 Update:

- Same store sales increased 0.9 % in October, marking a 490 basis point increase over September

- Sales on jcp.com increased 37.6 % versus last year, a continuation and acceleration of the positive trend in the Company's online business

- Conversion continues to improve in October compared to last year, reflecting favorable customer response to promotional events and improved inventory levels

- "The Company attributes its improved sales trends to the restoration of inventory levels in key private brands, including St. John's Bay®, Stafford®, and jcp Home(TM), and significant sales increases in Levi's®, Nike®, Carter's®, Dockers®, Alfred Dunner®, Vanity Fair® and IZOD®, some of the Company's largest national brands."

- "The Company also continues to make strides in the remerchandising and reconfiguration of its Home department both in stores and online to better reflect how customers shop while highlighting its most compelling brands and price points. These changes are beginning to resonate, as Home saw the largest percentage sales increase among the Company's divisions in October."

- "The Company noted, however, that gross margin showed sequential improvement within the quarter, with October representing the highest margin levels of the quarter."

Takeaway: This is old hat to the market by now, but it's still worth highlighting. True, a 0.9% comp is hardly worth declaring victory over -- especially when you're going against a -26% comp last year. But the +38% dot.com growth number was absolutely fantastic. That's a respectable growth number for a REAL company, never mind JCP. We still think that this beast is fixable, and remain in the bull camp..

LULU - LULU is repurposing its see-through Luon pants. Maybe these ones will fit everybody or should we say every body?

Takeaway: The company can't be quoted in the press as suggesting that the product did not fit the consumer because the women are too fat. Seriously…that's the most ridiculous thing we've heard from a Chairman of a company. You don't blame the consumer for not fitting into your product, you blame yourself for not making product that fits the customer.

MW, JOSB - Activist Takes Stake in Men's Wearhouse

- "The Men's Wearhouse Inc. has a new large shareholder in the form of Eminence Capital…"

- "The New York-based hedge fund in a regulatory filing Thursday said it is now the single largest shareholder in MW, holding nearly 4.7 million shares, or a 9.8 percent stake."

- "Eminence’s chief executive officer Ricky C. Sandler said in a letter to MW’s board: 'We are writing to you to express our disappointment in the board’s response to the recent proposal put forth by Jos. A. Bank [to] acquire MW….In our view, the board’s actions to date with respect to this matter fail to fulfill that obligation.'"

- “'We agree with the board that the proposed $48 share price undervalues MW both for its stand-alone prospects and for its fair share of the merger synergies.'"

Takeaway: We remain of the view that MW should remain independent, unless JOSB gives it complete assurance that it move forward with its business plan on its own. The $48 price is still too low.

GIII, JNY - G-III Drops Out of Jones Pursuit

- "G-III Apparel Group Ltd., which had been looking to acquire Jones’ apparel business, has dropped out of the process, according to two sources."

- That leaves private equity firm Sycamore Partners, which has been pursuing the footwear side of Jones, in an uncertain position. It is unclear whether Sycamore is able to, or even wants to, make a play for all of Jones, or if there’s another investor who would step into G-III’s place and buy the other portion of the company."

- "One source said the Jones camp has recently reached out anew to other investors to see if they want to buy the whole firm."

Takeaway: Not a surprise. JNY's brands are not desirable to the general public (if 80% of the brands went away the consumer wouldn't care), the stock is not valuable to the public equity market, and it's no surprise that private capital is getting skittish as well.

PUM - PUMA SE amends full-year 2013 guidance

(http://about.puma.com/wp-content/themes/aboutPUMA_theme/media/pdf/2013/08.11.13_E.pdf)

- "PUMA’s Management anticipates one-off charges, the majority of which will be non-cash effective, of approximately € 130 million to be booked in the fourth quarter of 2013. The majority of these special items will consist of impairments charges related to non-current assets. New initiatives include the closure of the product development centre in Vietnam and the intended transfer of our international product teams from London to Herzogenaurach."

- "Reflecting these new elements mentioned above, Management now expects 2013 full year net earnings to be positive, but significantly below those of 2012 (previously: increase in net earnings compared to 2012)."

Takeaway: First Adidas takes down numbers…now Puma. Not a good month for German sports apparel brands. At the same time, Nike is crushing it. Germany hates Nike.

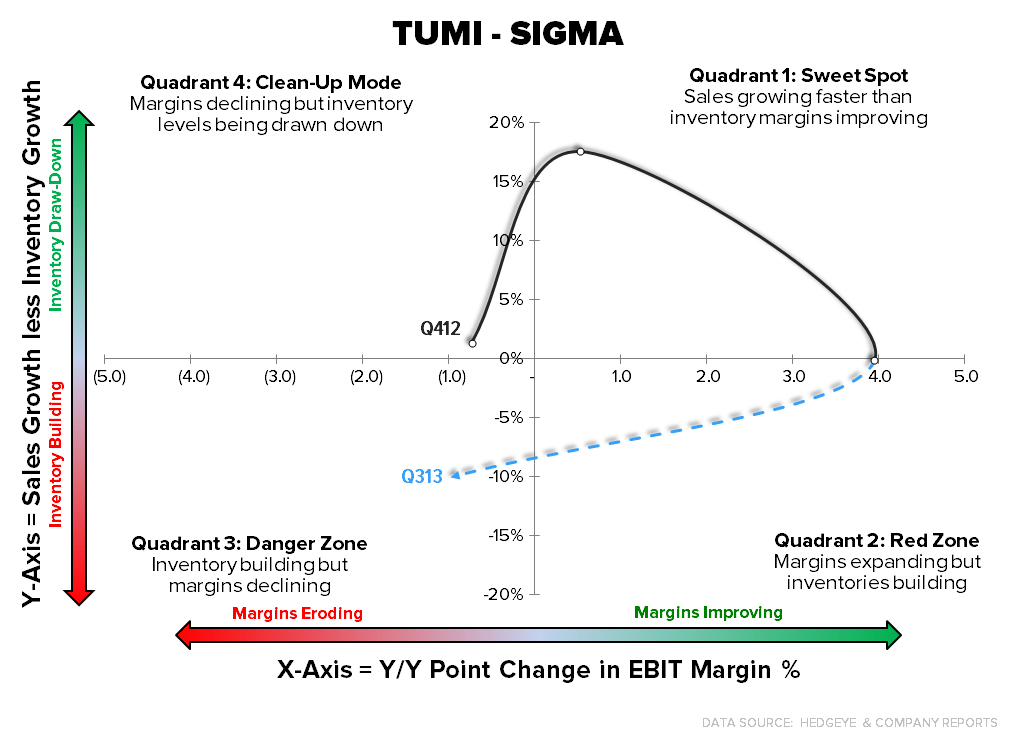

BEBE, TUMI - BEBE & TUMI report quarterly results

Takeaway: Two polar opposite SIGMA results here. BEBE (surprisingly) takes a sharp about-face from the Danger Zone to positive sales/inventory territory. On the flip side, TUMI went from the Sweet Spot (sales up, inventories down and margins up) to the dungeon -- pretty much polar opposite to where it had been.

HBI - HanesBrands to prepay 8% senior notes due 2016

(http://www.fibre2fashion.com/news/garment-company-news/newsdetails.aspx?news_id=155377)

- "The company will prepay the remaining $250 million of 8 Percent Senior Notes on Dec. 16, 2013, completing its successful multiyear campaign to use cash flow to retire all of the company’s bond debt except for its $1 billion of 6.375 percent notes."

- "The company expects to incur costs of approximately $15 million in the fourth quarter of 2013 for bond prepayment expenses and acceleration of noncash unamortized debt costs. The expectation for these costs has been previously communicated and is incorporated in the company’s 2013 financial guidance."

Takeaway: More of the same from HBI. Financial engineering is creating value. Not our preferred way to drive the stock, but hey…it works. The accretion from the MFB acquisition is a bigger deal. The company continues to sandbag. Estimates are going higher.

INDUSTRY NEWS

Chinese Luxury Market Poised for Uptick

- "The luxury market in China is expected to regain momentum in 2014 as Mainland consumer tastes and spending habits continue to become more sophisticated, according to a new luxury forecast released by communications agency Ruder Finn in partnership with Ipsos Group, a market research firm."

- "Chinese consumers increasingly care less about brand names and more about the uniqueness of products, the study said. It also found that Mainland shoppers care more about customer service, with 92 percent of those surveyed expressing dissatisfaction with service offered by luxury brands within China, which is fueling more purchases overseas."

- "Nearly 40 percent of Chinese surveyed said they are turning to the Internet for luxury shopping, representing a 22 percent increase compared with 2012."