This note was originally published at 8am on October 25, 2013 for Hedgeye subscribers.

"Whoever fights monsters should see to that in the process he does not become a monster. And if you gaze long enough into the abyss, the abyss will gaze back at you."

- Nietzsche

Yesterday I was flying out to San Francisco and the United Flight I was on lacked two key things: access to the Internet and/or a choice in movies. As a result, I was stuck watching Monsters, Inc.

For those of you that have progeny perhaps you've seen it already? I'm still in the bachelor camp, so don't regularly watch Pixar cartoons. I also have to sadly report, it wasn't all that scary, though it was cute and funny.

The movie did, however, make me think about a few things that currently scare me about the U.S. economy. In no particular order, my biggest fears are:

1) The Federal Reserve - We certainly harp on the Federal Reserve and rightfully so as an un-elected and largely unaccountable body with the power to influence the global economy is very scary. Our biggest concern is the excesses that are being built into the system because of elongated, extreme monetary policy.

The economy is growing and the unemployment rate is in decline, but we remain at the zero bound in interest rates. Admittedly the policy has helped to inflate some asset classes, such as housing, that were a major anchor on the banking system. Unfortunately, this extreme monetary policy has created an economy and set of markets that are highly sensitive to central bank actions.

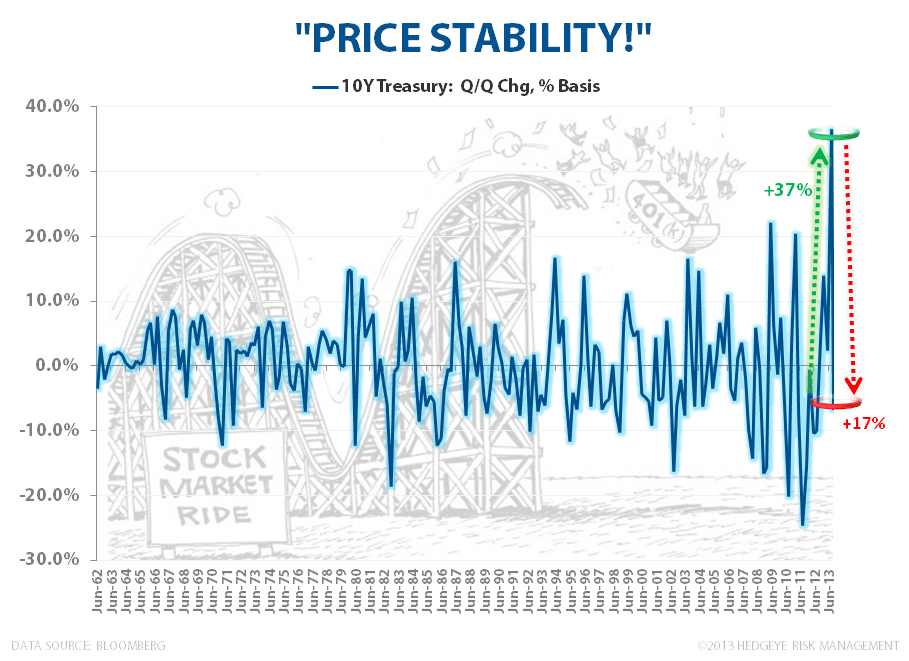

In the chart of the day, we highlight this point by looking at the volatility that is occurring in the interest rate market. As an example, rates on the 10Y spiked ~37% in 3Q13. This is as substantial a move we've seen on a percentage basis in fifty years. Further, in the wake of Bernanke’s confused policy communication on Sept 18th, we’ve seen a marked reversal in 10Y treasury yields with rates declining -17% off peak levels.

2) Macro Data - Admittedly it's odd for a macro analyst to be scared of macro data, but I am and here's why - it is often grossly inaccurate.

An example from our research earlier this week was a note I wrote on gold (somewhat of a meaningful asset class). The note took a deeper look at a letter gold bug Eric Sprott wrote to the World Gold Council on supply and demand in the global gold market.

Sprott's thesis is that the global supply and demand numbers for gold grossly overstate the excess supply of gold in the world. In fact, Sprott thinks that in the year-to-date we are running at a supply deficit of some 503 tonnes.

Meanwhile the World Gold Council's projections for the year-to-date suggest the world is over supplied by a tune of 217 tonnes. If we annualize both sets of projections, the difference between them is a notational value of some $50 billion dollars. Not exactly chump change !

If you are one of those people that like to invest based on concrete date, like me, you must be scared of some macro data at times as well. If you believe Sprott, then you should be buying gold hand over fist, and if you believe the World Gold Council, you should be selling.

While we do like it when we get concrete data that informs us, as it relates to gold we'll stick with our sneaky correlation models, which show a very tight correlation to the Federal Reserve balance sheet and prevailing, forward policy expectations. Interestingly, for the first time in a year, gold is actually looking like a buy in our quant model. Scary indeed!

3) U.S. Economy - Coming out of the Great Recession, the U.S. outperformed many of its western peers in both labor market and broader economic improvement. From here, though, there a few reasons to be scared.

The equity markets domestically have been on a tear and are literally registering new all-time highs – but, of course, with highs in equities and expanding multiples come high expectations for forward fundamentals. A few things that might not be so rosy on the U.S. over the next few months include:

1) Debt and debt ceiling - The uncertainty on the recent debt ceiling debacle led to a meaningful decline in consumer confidence and a slowing in economic activity. There is now a series of dates from December to February, that investors will be watching to see if there will be another debt ceiling scare or government shutdown. In markets, confusion breeds contempt.

- December 13th – the date when a House-Senate committee will report back on negotiations on a longer term budget deal;

- January 15th – the date on which the government is now open until subject to another budget agreement being reached; and

- February 7th – the next debt ceiling.

2) Corporate earnings – The results from U.S. corporate this quarter haven’t been terrible, but they certainly haven’t been gangbusters either. As of yesterday, 52% of companies are seeing sales accelerate, 51% are seeing earnings accelerate, and 47% are seeing operating margins expand. That sounds good, but the translation is that over half of corporate America is seeing earnings, revenue and margins decelerate.

3) Financials – We’ve already become more cautious on the financial sector over the last couple of days as we’ve taken Franklin Templeton off our Best Ideas as we see the outflow from bond funds slowing. More broadly, as the yield curve narrows, this is negative for banks generally. Borrowing short and lending long doesn’t pay in a narrow yield curve environment. In the year-to-date, financials has been a market leader up 26%, the second best sector after consumer discretionary. If this reverses, it will be hard for the SP500 to march higher.

Halloween is only six days away, so I don’t want to scare you too much . . . Boo! Or do I?

Our immediate-term Global Macro Risk Ranges are now as follows:

SPX 1733-1754

VIX 12.02-15.01

USD 78.81-79.74

Euro 1.36-1.38

Yen 97.06-98.63

Gold 1320-1363

Enjoy the weekend.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research