Long GBP/USD (via the etf FXB)

Our bullish call on the British Pound vs the US Dollar was strengthen this morning with the ECB unexpectedly cutting its main interest rate by 25bps to 0.25%. In our minds, it’s now anyone’s guess how the central bank currency wars between the USD and EUR will play out. However, anchored on our Q4 2013 Macro theme of #EuroBulls (presented on 10/11/13), we continue to like British Sterling.

The Bank of England was also out this morning and announced no change to its interest rate (anchored at 0.5% since March 2009) and kept its asset purchase program target (QE) unchanged at £375B.

Here are the main factors underpinning our bullish GBP/USD Call:

- Regime: we are bullish on the regime change at the BOE, replacing Mervyn King with Mark Carney – we believe Carney has fresh ideas and a focus to use forward guidance to direct the economy to stable growth

- Fiscal Policy: we expect (and are already seeing signs of) the country’s decision to issue austerity before its regional peers during the global recession as paying off in spades via accelerated growth over its European peers. We’ve seen steady improvement in the country’s deficit (as a % of GDP), from -11.4% in 2009 to -6.1% last year and is forecast to hit -4.4% in 2014

- Monetary Policy: we do not expect rate cuts or additional QE over the medium term. In the last policy meeting (October), the BOE voted (9-0) to keep rates on hold and the asset purchase program unchanged

- Economic Data: we believe that the health of an economy is reflected in its currency – the data suggests continued improvement (more below) which should bolster the GBP versus major currencies

- Vs the USD: we see a very favorable comparison versus the U.S. Dollar as Bernanke/Yellen burn the Greenback via delaying the call to taper (likely pushed out to March 2014)

By the Charts:

- GBP/USD – the cross is trading comfortably above over our intermediate term TREND level of support

- GDP – we expect outperformance versus most of its European peers, built largely on choking down austerity first during the great recession. The European Commission in its autumn report this week raised UK GDP expectations, to +1.3% in 2013 from +0.6% and to +2.2% in 2014 versus a previous estimate of +1.7%.

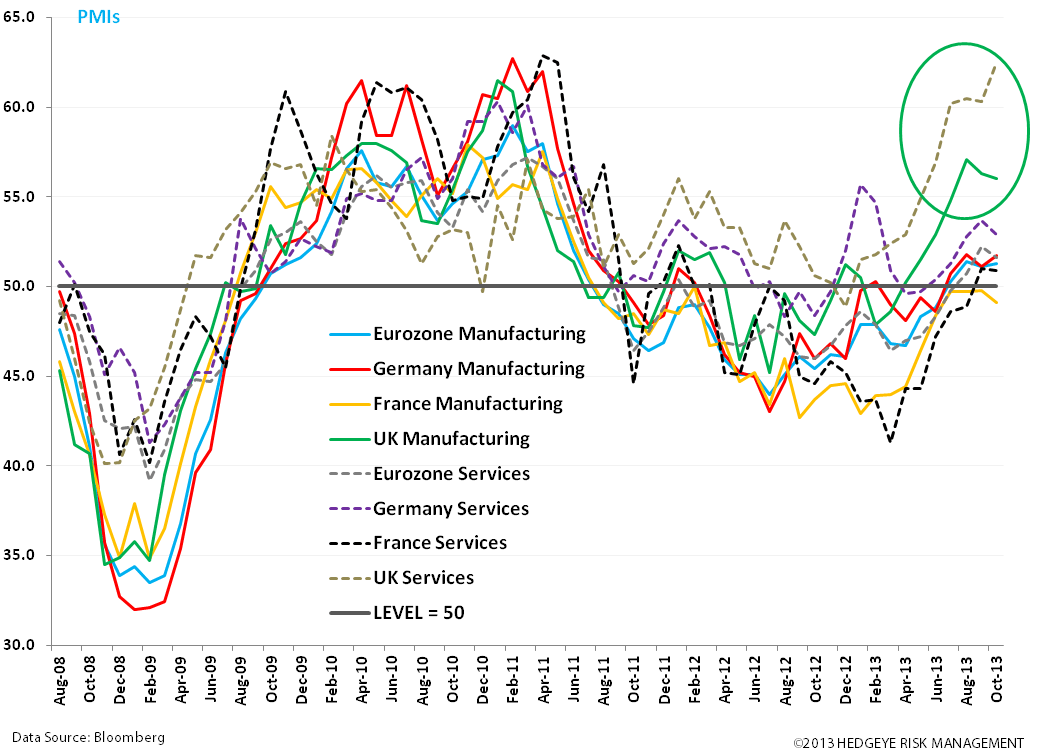

- PMIs – UK Services and Manufacturing PMIs continue to outperform continental Europe. UK Services PMI for October hit a 16 year high at 62.5! (above 50 = expansion). The UK PMI Construction also rose to 59.4 OCT (exp. 58.7) vs 58.9 SEPT

- Confidence– Below we show business and consumer confidence, both trending higher since mid 2012

- Manufacturing and Retail Sales – confidence is a huge piece of the consumption puzzle; we see the trend in manufacturing and retail sales moving positively over the intermediate term. UK Industrial Production popped to 2.2% SEPT Y/Y (exp. 1.8%) vs -1.5% AUG

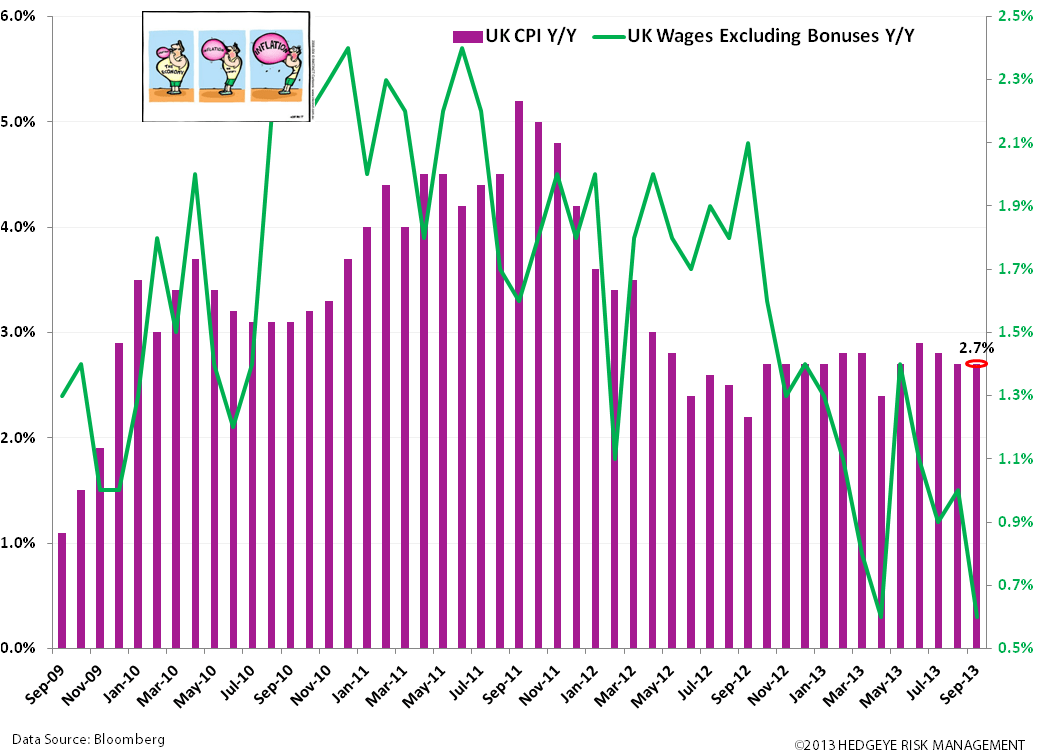

- CPI – Inflation remains sticky and high, however we expect a #StrongCurrency to increase purchasing power by deflating imported inflation

Matthew Hedrick

Associate