We’re stunned by the valuations we are seeing in the casual dining industry. Is anyone even willing to buy casual dining names at these levels?

2013 Year-To-Date Casual Dining Statistics:

YTD Performance

- Casual dining stocks are up +47% versus +24% for the S&P 500

YTD Macro

- Conference Board Consumer Confidence is up +21.9%

- The US Unemployment Rate has improved from 7.9% to 7.2%

- US Initial Jobless Claims SA have improved from 373 to 340

- Daily National Average Gasoline Prices are down -1.8%

- US Disposable Income Per Capita is up +2.9%

YTD Fundamentals

- On average, casual dining EPS revisions are down -2.9%

- On average, calendar year revenue growth for companies in the Hedgeye Casual Dining Index is estimated to be +3.7%

- On average, calendar year EPS growth for companies in the Hedgeye Casual Dining Index is estimated to be +8.6% on a normalized basis (excludes RT and RUTH)

- On average, same-store sales for companies in the Hedgeye Casual Dining Index have declined from +1% in 1Q13 to +0.5% in 3Q13

- According to Knapp Track, casual dining traffic is down -2.6% through September

- According to Black Box, casual dining traffic is down -2.6% through September

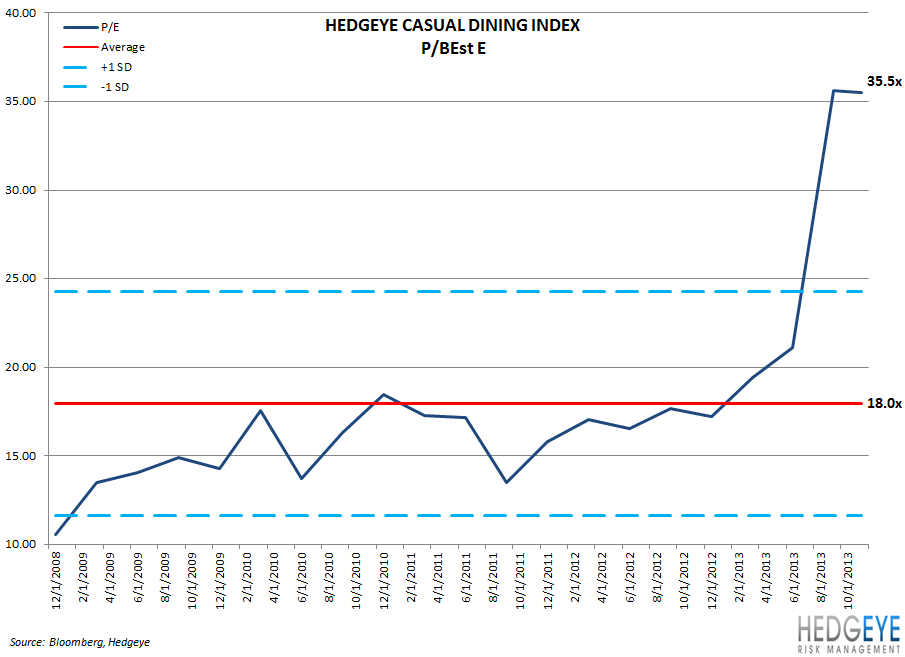

YTD Valuation

- On average, the EV/TTM EBITDA multiple for the Hedgeye Casual Dining Index is up +58.9%

- On average, the P/TTM E multiple for the Hedgeye Casual Dining Index is up +48.9%

- On average, the P/TTM CF multiple for the Hedgeye Casual Dining Index is up +50.5%

The late 1990s marked the beginning of a decade of growth for the casual dining industry. During this time, the average cash flow multiple was 7x. Today, we estimate the average cash flow multiple to be around 10.7x, as the majority of large, mature names have little to no growth.

Declining traffic, coupled with an earnings miss, used to instill fear in restaurant investors, often sending valuations for those companies to trade closer to 5x cash flow. This has not been the case lately. It is our view that the casual dining sector is in secular decline due, in large part, to the increased competition from fast casual restaurants and grocers. Valuations are stretched and appear to be approaching peak levels. We believe that the charts below are beginning to resemble a bubble.

*The Hedgeye Casual Dining Index includes BOBE, BWLD, CAKE, CBRL, DRI, EAT, RRGB, RT, RUTH, TXRH.

Howard Penney

Managing Director