The benign commodity environment and DRI increasing focus on cutting out fat will leave the street focused on same-store sales for FY4Q09.

In FY3Q09, DRI blended same-store sales were down 3.2% at the three core brands largest brands; slightly better that the Knapp-Track industry average of 5.7%. Note we have adjusted the Knapp-Track industry average to comply with DRI fiscal quarter and include DRI's same-store sales trends.

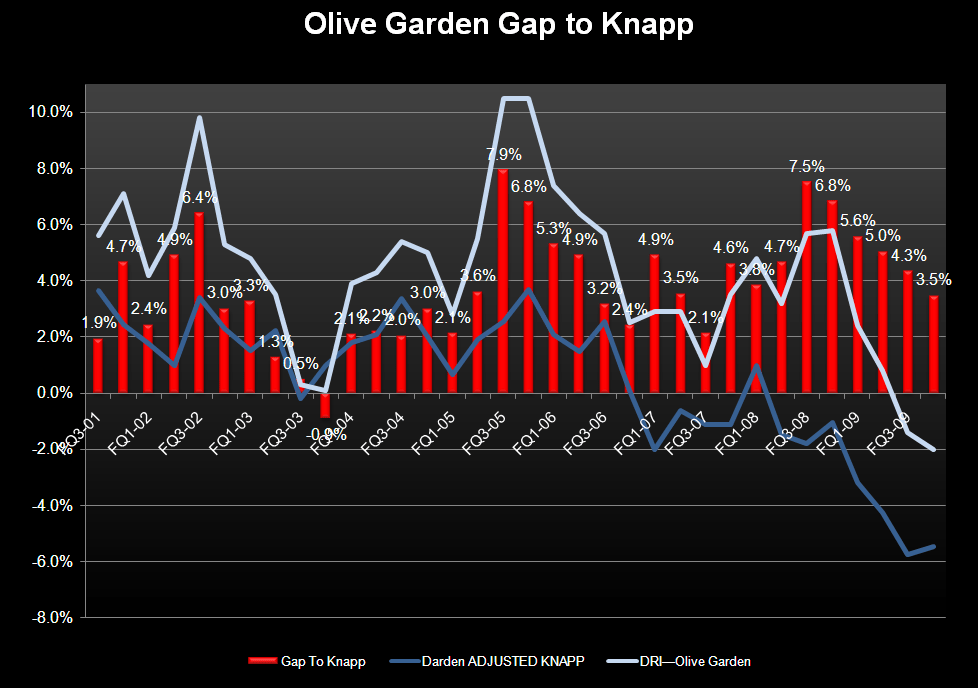

In FY3Q09, Red Lobster reported same-store sales decline of 4.6%, which was 1.1% above Knapp-Track. For the same period the Olive Garden reported same-store sales decline of 1.4%, which was 4.3% above Knapp-Track. Longhorn Steakhouse same-restaurant sales decreased 5.4% for the quarter, which was 0.2% above Knapp-Track.

In FY4Q09, we are looking for blended DRI same-store sales to be down 3.1% or 2.4% better the Knapp-Track. On a relative basis, LongHorn is likely to show the best sequential results on the back of a new media strategy put in place in FY3Q. The number of restaurants with advertising support increased from 45% to 60% and the media weight by 25% (at no incremental cost).

In FY4Q09, we are estimating that Red Lobster's same-store sales decline of 3.0%, which is 2.5% above Knapp-Track. For the same period the Olive Garden reported same-store sales decline of 2.0%, which is 3.5% above Knapp-Track. Longhorn Steakhouse same-restaurant sales decreased 3.5% for the quarter, which is 2.0% above Knapp-Track. Consensus estimates for Red Lobster, Olive garden and LongHorn are -2.2, -0.2 and -4.5%, respectively.

For FY4Q, I'm slightly - $0.01 - ahead of consensus at $0.87 and $2.72 for the fiscal year. Given what we are hearing, and confirmed by the stabilization in Knapp-Track trends, I don't believe there will be much deviation from the trend I have outlined. DRI's marketing muscle is clearly a benefit during difficult times. Benign commodity trends, incremental pricing and cost cutting will lead to a 70bps of sequential EBIT margin improvement to 10.6%.

Trading at 8.0x EV/EBITDA, DRI is relatively expensive - trading at two multiple points above the FSR group. Short interest is low at 7.6% versus 13% for the FSR group. While I don't think there is another $10 million surprise in FY4Q, DRI has further fat to cut out of its cost structure.

While things this quarter look good for DRI, longer-term I'm have issues with DRI pushing hard on the organic growth engine. As I measure how DRI is investing is cash, the trends are headed south. Over the past two years the company's ROIIC has been declining - never a great sign.