“Why do we have noses that run and feet that smell?”

-Unknown

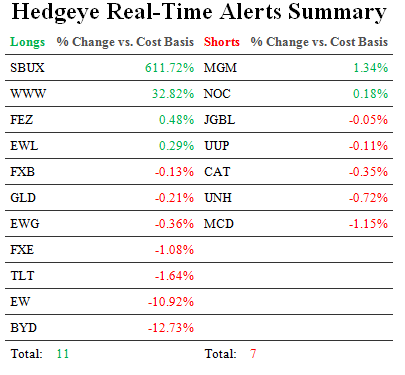

The Fed’s English can be confusing too. As you can see in our Chart of The Day, that’s what’s been driving unprecedented volatility in the US bond market this year. Confusion about @FederalReserve policy is starting to breed contempt.

But oh no, no, no – silly Mucker must have this all wrong. The Fed has a “study” that proves pretty much anything they want to prove. The latest data-mining propaganda coming out of the head of the anti-dog-eat-dog-Fed-Monetary-Affairs-Division, William English, insinuates that it’s time for Bernanke and Yellen to move the goal posts again on the unemployment target. #Wonderful

Huh? This is what Bush/Obama empowered - an un-elected and un-checked central planning agency that is trying to prove out their academic dogma versus well established forces (like gravity). The Fed can pretty much keep making up the rules as they go here until the entire Bond Bubble blows up. Isn’t that awesome? History will write plenty of English “papers” on this!

Back to the Global Macro Grind…

Since the Fed was wrong on its US growth forecast again (this time they and #OldWall were too low at the beginning of 2013, and the bond market started front-running them as tapering expectations perpetuated the 2-stroke engine of #StrongDollar + #RatesRising), and the unemployment rate is getting too close to their policy change target of 6.5%, they need to change the target.

#cool

Or is it? I’ll be doing another full day of institutional client meetings in NYC today and I’ll tell you that (especially for clients who aren’t in the business of being levered-long bonds that they can’t get out of) this expectations game isn’t cool.

Why?

- 1. Dollar Down + Rates Down = US Growth Expectations Down (see US economic history for details)

- For the last month, you’ve seen every growth “Style Factor” start to underperform slow-growth yield chasing

- If we’re going back to slow-growth yield chasing (long Gold, Consumer Staples, and Bonds) that’s a big shift

The Fed won’t have a “study” on this because that would prove that incrementally dovish policy does 2 things:

- Devalues America’s Currency (which they are supposed to be protecting)

- Represses rates and growth expectations (as Dollar Debauchery perpetuates inflation, not real-growth)

All the while, the same western academic dogma that we imported from Europe remains in parts of Europe. This morning’s central planning bureau headline out of Italy’s Finance Minister is begging Mario Draghi to cut rates and devalue the Euro!

To review, from December 2012 to August 2013, a #StrongCurrency policy (tapering):

- Crushed inflation expectations

- Ramped real (inflation adjusted) growth expectations

But these damn bureaucrats see that very Deflating of The Inflation (from the world’s all-time high inflation readings of Gold and Food prices in 2011-2012) as a threat to their failed policies!

Moving along, I bought more exposure to our #EuroBull Macro Theme yesterday via:

- Eurostoxx50 Index (FEZ) which tested and held my immediate-term TRADE line of support

- Swiss stocks (EWL) which were holding support and have bounced a full +1% this morning

Why buy US Growth anymore if we’re going to let these clowns at the Fed blow up our currency again? This all started with Keynes in Britain, and even the British have given up on the QE thing (thank God) at this point. Carney (the Canadian who doesn’t do crack cocaine) replacing Mervyn King at the Bank of England is like replacing Bernanke with me (or something like that).

#StrongPound in the United Kingdom continues to perpetuate rising UK growth expectations. When growth expectations rise, government bond yields rise (bonds go down). The 10yr UK Gilt Bond Yield is +10 basis points in the last 2-days as the UK printed the best Services PMI reading in 16 years (UK industrial production growth just accelerated to +2.2% y/y as well).

The final point to be made this morning is that after perpetuating Gold, Bond, and Utility Bubbles with his 0%-interest-rates-forever thing (formally known in a Hedgeye “paper” as Yield Chasing), Bernanke is probably going to get tagged with creating another US stock market bubble too. Today’s II Bull/Bear Sentiment Spread just clocked a fresh YTD high at +3960bps wide to the bull side.

I am still recommending prayer for those at the Fed who still don’t yet know about the “paper” on the definition of insanity. The summary of the paper is in plain English too – doing the same thing over and over again, and expecting different results.

Our immediate-term Risk Ranges are now:

UST 10yr Yield 2.55-2.69%

SPX 1

DAX 8

Swiss Market 8113-8299

Pound 1.60-1.62

Gold 1

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer