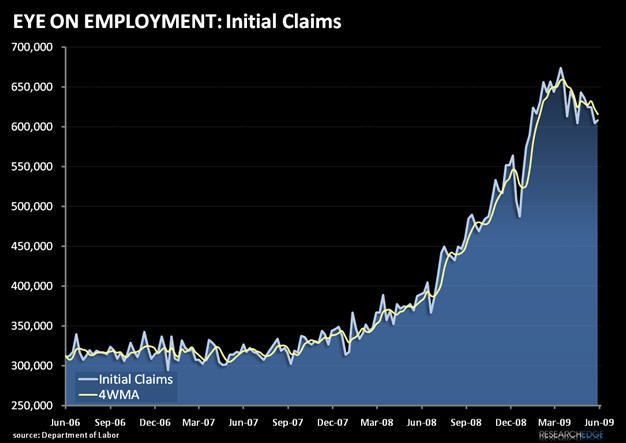

Initial claims continue to hover above the 600K line in the sand

Today's Initial claims number arrived at 608K; 3k higher than the prior week's number which was revised upwards by 4K, but still below the four week moving average by 8k. Since last week's bullish claims reading the S&P 500 has declined modestly on slightly increased volatility, while the US Dollar index has cut its decline for the year significantly from -7% to under -2% and the yield curve has narrowed with 2 year yields rising to close the gap with the 10 year by over 10 basis points.

With Claims still hugging the psychologically important 600k line, the "glass half full " crowd are left still looking for signs of a bottom here, with accelerating declines in benefits paid providing more clues that the rate of job losses has moderated sharply.

As always with the sometime conflicting employment data that the US government provides, interpretation is key: declining benefits paid to existing claimants could indicate a tightening job market for the newly unemployed, and could perversely cause the department of Labor Unemployment Rate metric (a lagging indicator -see our post on June 9) to rise. Despite this caveat, the declining pace of job losses is clearly evident and we currently anticipate that next month's unemployment release will likely register slightly below 10% -that critical double digit dam-buster that the bears are desperately seeking.

Our overall tactical outlook has not fundamentally changed from last week: We expect to continue to trade the equity market inside a narrow range for the near term, and while we have increased our domestic equity exposure to 15% from 12 % since last week, we have not seen enough supporting data for the equity market to join the glass half full crew yet.

Andrew Barber

Director