This note was originally published at 8am on October 21, 2013 for Hedgeye subscribers.

“Ideas are incapable of confinement or exclusive appropriation.”

-Thomas Jefferson

One of the biggest push-backs I’ve been getting from both US stock market bulls and bears throughout the 2nd half of 2013 is one and the same – “I can’t buy that up here – I missed the move.” And my response continues to be that Mr. Market doesn’t care about what you did or did not miss. The market’s price is both dynamic and non-linear. As Jesse Pinkman would say, ‘it’s evolution, yo.’

Pinkman is not Jefferson. The aforementioned quote comes from a great book on the evolution of entropy economics that I’m still reviewing: George Gilder’s Knowledge And Power. If you are a growth investor (and/or you just want to be long growth as a Style Factor right now), read Chapter 10: “Romer’s Recipes and Their Limits” (Paul, not that raging Keynesian, Christina Romer).

“Still, change keeps coming, fueled by technology, as Romer’s 1990 paper reminded the economics fraternity. As productivity grows, technology keeps freeing people. And this … really is, in some sense, the scarcest commodity: the power of the human intellect.” (Knowledge and Power, page 96)

Back to the Global Macro Grind…

BREAKING: the Global Macro call of 2013 is basically baked into the cake. You were either long growth, or you were not. With the Russell 2000 closing at another all-time high on Friday (1114 = +31.2% YTD), long virtually anything growth has absolutely pulverized the #EOW (end of the world) “new normal” thing (Gold, Bonds, Utilities, etc.).

In terms of 2013 US Equity Market Style Factors, here’s how awesome growth, as a style, looks at the all-time highs:

- LOW YIELD (i.e. growthier stocks) = +35.2% YTD (vs High Yield Div stocks +14.9%)

- TOP 25% EPS GROWTH (Top Quartile of SP500) = +34.1% YTD (vs Bottom 25% = +20.8%)

- TOP 25% SALES GROWTH (Top Quartile) = +31.4% YTD

- HIGH BETA = +30.5% YTD

- HIGH SHORT INTEREST = +28.1% YTD

#awesome

To be clear, growth (as an investing style) can be very frustrating to A) embrace and B) capitalize upon. I think the reasons for that are bountiful (it’s called a cycle), but here are three big ones:

- STYLE: Growth Investing hasn’t worked like this since the 1990s – and few were positioned for an early 1990s style US recovery

- CYA: many equity investors are still fighting the last war of getting smoked in 2008 – consensus is long yielding income, not growth

- MULTIPLE EXPANSION: expensive gets more expensive on the way up

That last one is really tough for people to swallow, primarily because there are just so many people managing money these days. How many people do you know short stocks because they’re “expensive”?

I’d argue that part of Carl Icahn’s resurgence as an activist has a lot to do with being mucho long Style Factors 4 and 5 (HIGH BETA + HIGH SHORT INTEREST). With what was working locked into his sights, all he needed was Bill Ackman pumping those factors live @CNBC.

How many investors break the market down by Style Factors?

I’d say a lot fewer than you might think. And, to a degree, this makes Institutional Investing a lot like Moneyball was before Billy Beane did Moneyball. In the end, a chubby 1st baseman with a high on base % beats a pretty boy “highly concentrated” activist long ball hitter.

So what if my writing this note top-ticks growth vs. slow growth for 2013?

- That could very well happen – the performance divergences between growth and slow growth styles is at its YTD high

- That could very well not happen – if you started short selling growth in 1995 or 1996, let me know how that went by 1999

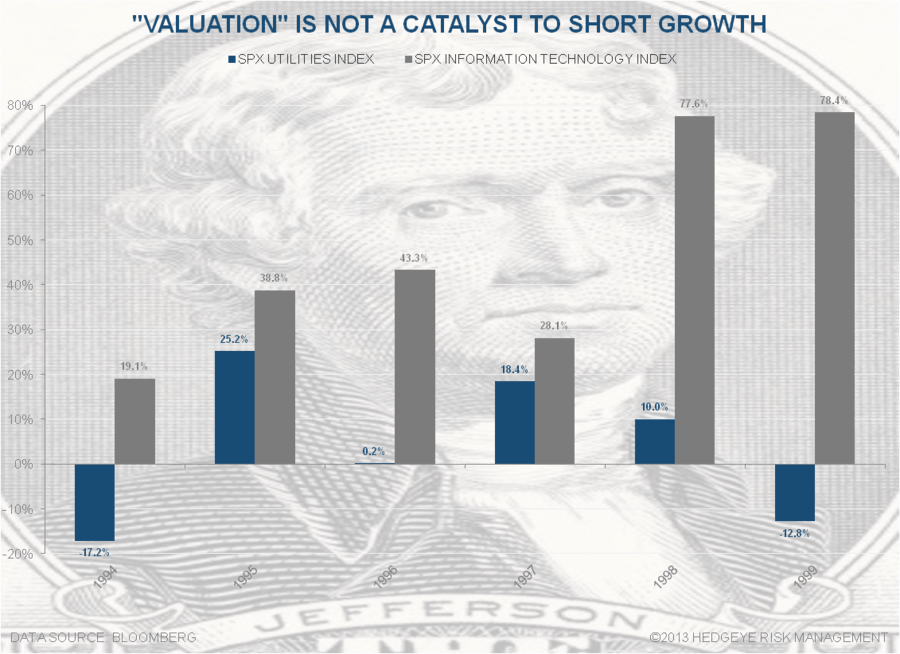

This is why the 1994 Global Macro Market metaphor (bond market blew up) really matters to me. As you can see in the Chart of The Day:

- Utilities (XLU) = -17.4% in 1994, 0.2% in 1996, -12.8% in 1999

- Tech (XLK) = +19.1% in 1994, +43.3% in 1996, +78.4% in 1999

How many investors are positioned for 2013 being 1993? How about 1995?

I don’t know if this is the top of growth investing. If it is, it ends with the Twitter IPO. But I do know that The Scarcest Commodity out there right now is being a raging growth bull. And that’s all I have to say about that.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.58-2.69%

DAX 8736-8968

SPX 1701-1760

VIX 11.55-15.19

USD 79.21-80.28

Gold 1267-1333

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer