That’s right, we believe now is a great opportunity to get long the EUR/USD on weakness [etf: FXE].

Draghi and some of his lieutenants (including ECB Governing Council member Ewald Nowotny) talked down the common currency mid-week, suggesting that the ECB was ready to issue liquidity measures to spur the broader economy. We heard whispers of another round of LTRO, and then the manic media ran with headlines that the ECB is going to cut rates, all of which sent the EUR/USD correcting over 2%.

By our score, the first two LTROs that Draghi issued were complete failures – banks either quickly repaid these loans and/or capitalized playing the spread on these cheap 1% loans, but in any case, did not lend to the real economy. This time around, we believe Draghi has 1). learned his lesson and will not issue another failed LTRO program to boost liquidity, and 2). has suggested in press conferences and other commentary that the data he’s tracking shows initial positive signs of a recovery across the Eurozone, which therefore suggests to us that neither liquidity measures nor a rate cut (why waste the powder now?) would be warranted over the near term.

Our #EuroBulls Purview: as we discussed as one of the team’s Q4 quarterly macro themes, #EuroBulls, we’re bullish on German and UK equities (see Keith’s latest video for that update) and bullish on the EUR/USD, built on a few central factors:

- Bernanke/Yellen continue to burn the USD via delaying the call to taper (note: we do not expect any update in the December meeting), #EuroBulls

- EUR strength reflects country strength: recent data continues to reflect that the Eurozone economy has stabilized and is beginning to accelerate, #EuroBulls

- The deflation of inflation across the Eurozone equates to more consumer purchasing power via lowering the consumption tax, #EuroBulls

- The ECB’s hawkish policy, which we believe is the decision not to cut rates or issue imminent liquidity, is #EuroBulls

- The Data: as we show below in a number of updated charts from our #EuroBulls Q4 themes deck, from PMIs and Confidence to Auto Sales and Factory Orders, the trend in the data is positive : this supports our conviction to be overweight European equities over U.S. equities.

- Further, we see a strong positive correlation between the EUR/USD and the DAX, encouraging us to be long the German DAX via the eft EWG. [We’re also bullish on the UK’s FTSE, via the etf EWU]

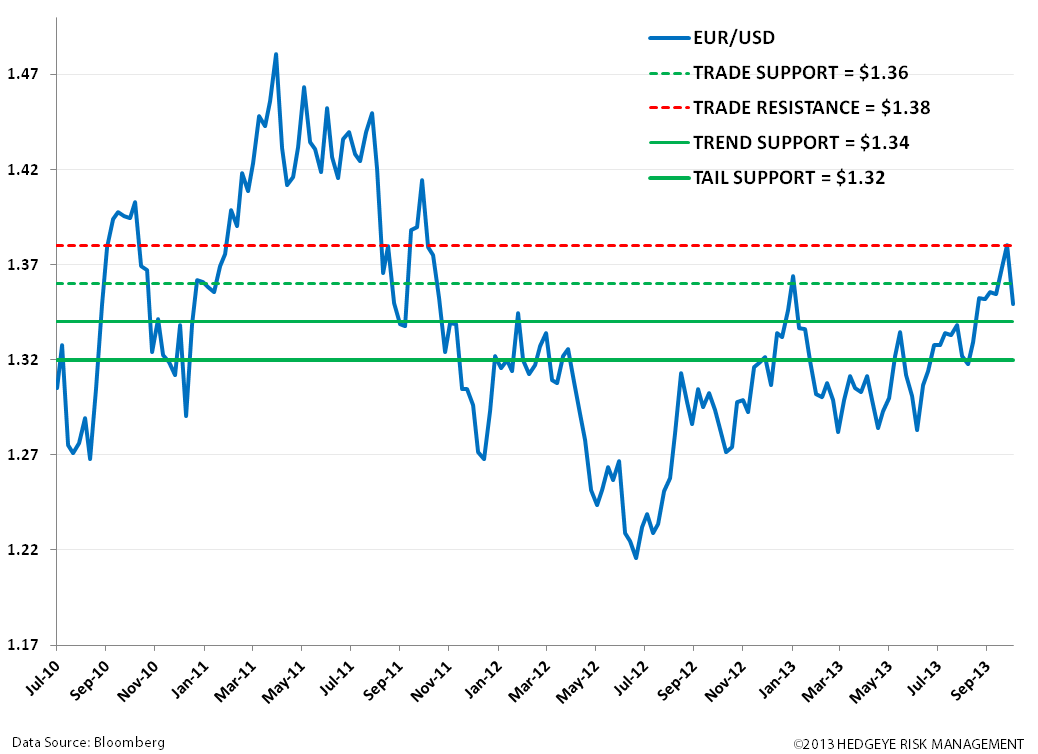

By the Charts:

- Our levels in the sand:

- PMIs bouncing: across the Eurozone, the majors have broadly held above the 50 level indicating expansion. While we don’t expect gangbuster moves in PMIs over the intermediate term, we expect them to indicate the acceleration in growth we’re seeing from low levels.

- Confidence Up: as we look out across Economic, Consumer, and Business Confidence, an upward trend is solidified. We expect this improvement to continue.

- Retail Sales: as a sign of the consumer’s health, and confidence, retail sales are even going up across the periphery: Italy Business Confidence 97.3 OCT vs 96.8 SEPT; Spain Retail Sales 2.2% SEPT Y/Y vs -4.4% AUG; Greece Retail Sales -8.9% AUG Y/Y vs -14.1% JUL

- Even Autos are getting a bounce: New Commercial Vehicle Registrations for the EU just recorded +6.1% Y/Y in September. Any increase in big ticket items is a signal to us of confidence.

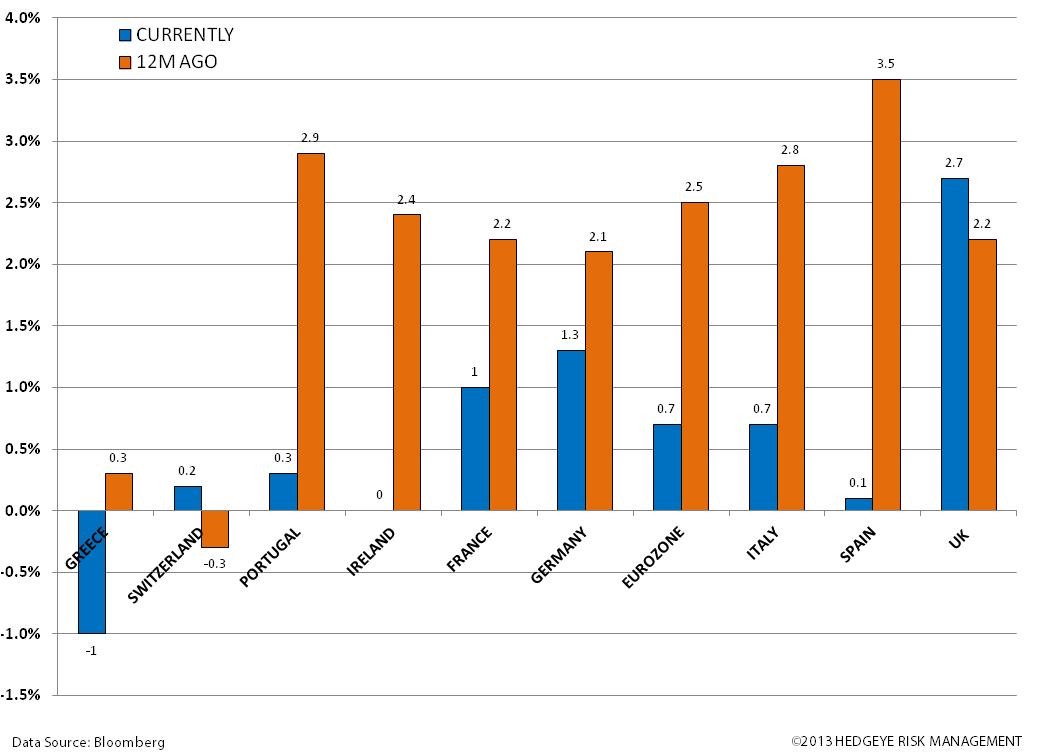

- Deflating the Inflation: anchoring improving retail sales and confidence is deflation of the inflation. While Draghi has “failed” to meet his 2% CPI target (currently at 0.7% Y/Y vs 1.1% in September), deflating the inflation equates to a lower consumption tax, which will boost real inflation adjusted growth.

- The CPI Turn Matters: the year over year changes are huge!

- German Preference: we continue to like the DAX, on a positive correlation to the EUR/USD. Fundamentals remain grounded with a low unemployment rate (6.9% vs 12.2% in the Eurozone), CPI at 1.3% Y/Y, strong PMIs and consumer and business confidence, and an inflection in factory orders to the upside. [Long German DAX via the etf EWG]

Enjoy the weekend!

Matthew Hedrick

Associate