TODAY’S S&P 500 SET-UP – November 1, 2013

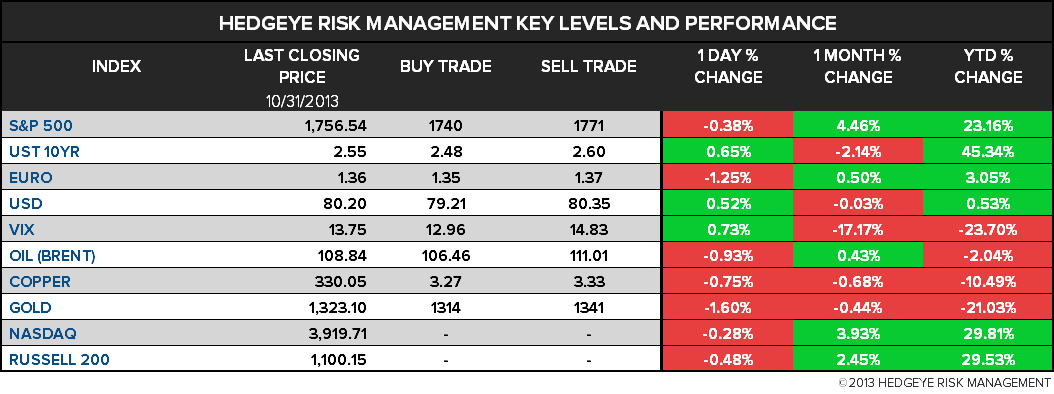

As we look at today's setup for the S&P 500, the range is 31 points or 0.94% downside to 1740 and 0.82% upside to 1771.

SECTOR PERFORMANCE

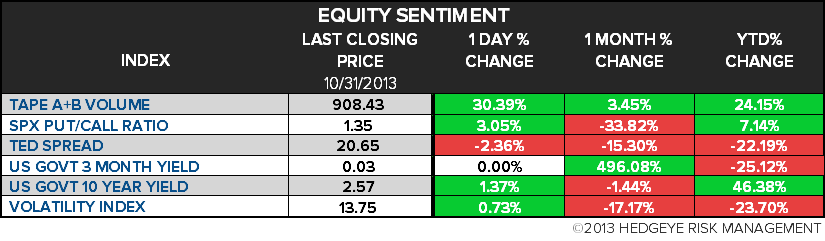

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.27 from 2.25

- VIX closed at 13.75 1 day percent change of 0.73%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:58am: Markit U.S. PMI Final, Oct., est. 51.1

- 9:10am: Fed’s Bullard speaks on monetary policy in St. Louis

- 10am: ISM Manufacturing, Oct., est. 55 (prior 56.2)

- 11:15am: Fed’s Kocherlakota speaks on health care in Minn.

- 12pm: Fed’s Lacker speaks in Philadelphia

- 1pm: Baker Hughes rig count

- 5pm: Total Vehicle Sales, Oct., est. 15.43m (prior 15.21m)

GOVERNMENT:

- Commerce Dept holds Day 2 of SelectUSA Summit with speakers incl. Commerce Sec. Penny Pritzker, Sec. of State John Kerry, Caterpillar CEO Doug Oberhelman; Ludwig Willisch, CEO of BMW North America

- President Obama meets with Iraq’s Nouri al-Maliki at White House to discuss defense, security issues

WHAT TO WATCH:

- FAA to let airlines apply for broader use of electronics

- Dutch govt selling $8.7b of ING’s U.S. mortgage bonds

- U.S. rule change allows $500 carryover in flex spending acct

- China manufacturing gauge tops ests. in recovery boost

- Nortel patent owner Rockstar sues Google, Huawei: Reuters

- U.S. tech leaders calling for data use laws: Washington Post

- Google, Red Hat, Oracle engineers deployed for Obamacare fix

- MasterCard momentum may build vs Visa as Europe rebounds

- Barrick may raise $3.45b in share sale to reduce debt

- RBS suspends 2 forex traders; would be first suspensions: FT

- Pemex may list some assets on exchange as early as 2014

- Oct. U.S. auto sales may disappoint; SAAR may hit 15.4m

- Macau casino revenue surged to record $4.6b in Oct.

EARNINGS:

- Allete (ALE) 8:30am, $0.73

- American Axle & Manufacturing (AXL) 8am, $0.56

- Buckeye Partners (BPL) 7am, $0.83

- CBOE Holdings (CBOE) 7:30am, $0.45

- Chevron (CVX) 8:30am, $2.70 - Preview

- Church & Dwight (CHD) 7am, $0.73

- Emera (EMA CN) 7:10am, $0.35

- Exelis (XLS) 7am, $0.41

- Fortis (FTS CN) 7am, $0.26

- Genesee & Wyoming (GWR) 6am, $1.22

- Madison Square Garden (MSG) 7:30am, $0.22

- Newcastle Investment (NCT) 6:30am, $0.12

- NextEra Energy (NEE) 7:30am, $1.39

- NorthStar Realty Finance (NRF) 7:30am, $0.24

- NV Energy (NVE) 6:31am, $0.89

- Oaktree Capital (OAK) 8:30am, $1.00

- Pembina Pipeline (PPL CN) Aft-mkt, $0.26

- SNC-Lavalin (SNC CN) 8:27am, $(0.47)

- Spirit Aerosystems (SPR) 7:30am, $0.61

- Telephone & Data Systems (TDS) 7:58am, $(0.10)

- Ultra Petroleum (UPL) 8am, $0.35

- United States Cellular (USM) 7:59am, $0.09

- Washington Post (WPO) 8:30am, est. N/A

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Palm Oil Enters Bull Market on Best Weekly Gain in Three Years

- Wheat Analysts Most Bearish in Year on Record Crop: Commodities

- Gold Heading for First Drop in Three Weeks on Fed Speculation

- Palm Oil Supplies in Indonesia Seen Disrupted by Prolonged Rains

- WTI Crude Heads for Longest Run of Weekly Declines Since 2012

- Copper Rises as China Manufacturing Expands More Than Estimated

- Wheat Poised for Worst Week Since June as India to Boost Supply

- China Refined Lead Market Seen by Antaike in Deficit in 2014

- India Iron Ore Exports to Remain Subdued, Morgan Stanley Says

- OPEC October Crude Production Climbs in Survey on Iraqi Gain

- U.S. Gulf Crude Sinks to Lowest Against Imports: Energy Markets

- Wal-Mart to Widows Will Feel U.S. Food Stamp Cuts Starting Today

- Founder of Top India Commodity Exchange Resigns Amid Probe

- China Gold Imports From Hong Kong Fall on Premium, Slow Demand

CURRENCIES

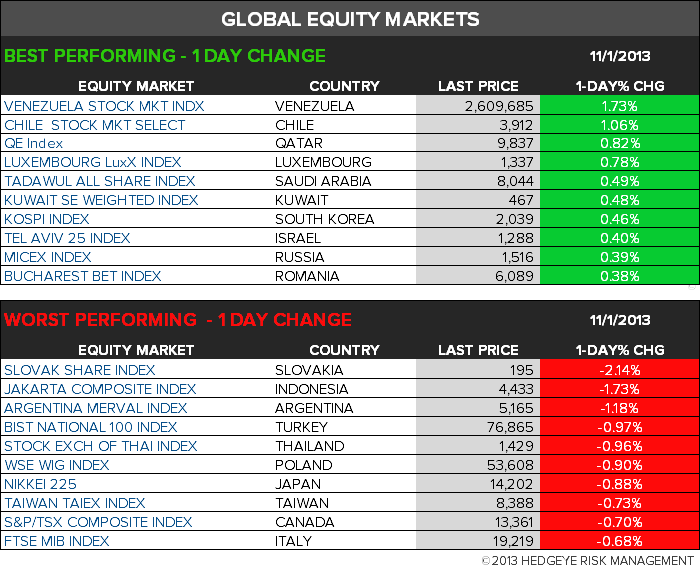

GLOBAL PERFORMANCE

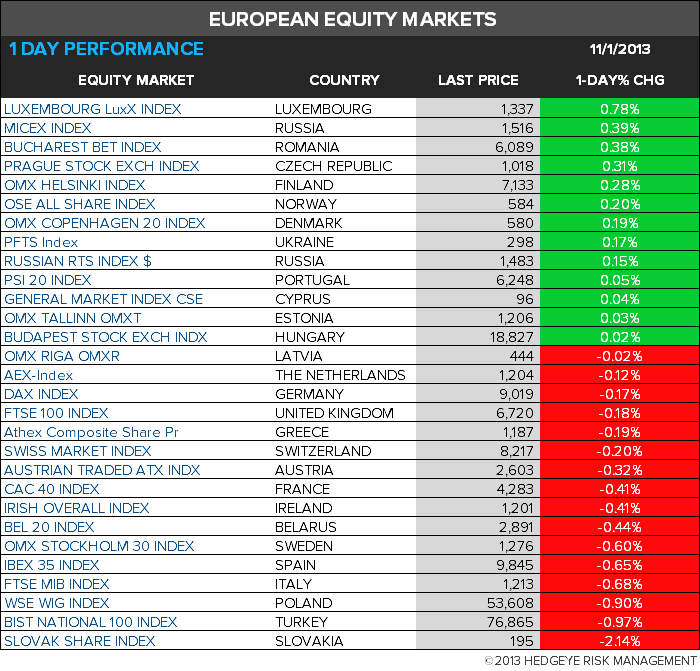

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team