SBUX: FIRING ON ALL CYLINDERS

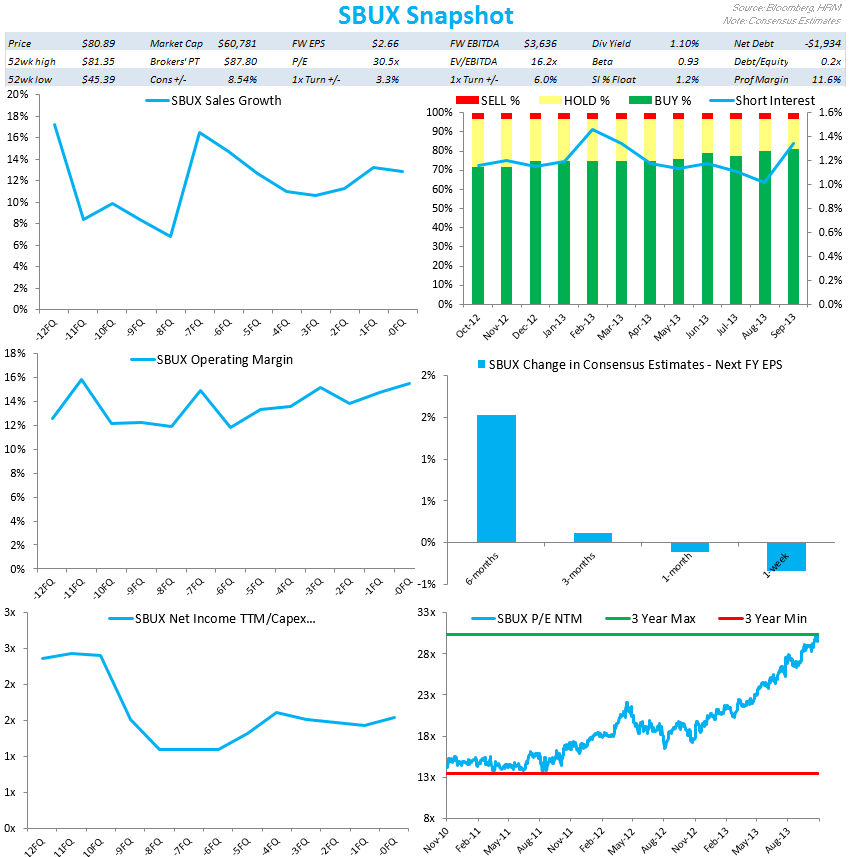

SBUX reported another all-star quarter in 4Q13 and appears to be firing on all cylinders heading into FY14. A strong commodity tailwind, international growth, the beginning of a recovery in the EMEA segment, and expansion into new segments of the global food and beverage industry are all bullish factors moving forward. The only slight negative stemming from what was, overall, a bullish conference call was management reigning in expectations for FY14, which, in our view, gives the company a better chance of surprising to the upside throughout the year.

Last night, Starbucks reported global same-store sales growth of 7%, marking the 15th consecutive quarter above 5%. Same-store sales in the Americas division grew 8% (including 5% traffic). Total revenue growth of 13% produced a 28% increase in operating profit and a 30% increase in EPS.

Americas:

- Revenues +11% y/y

- SSS two-year comp declined 50 bps sequentially

- Operating income +16%

- Operating margin +100 bps to 21.8%

- Food contributed ~200 bps to the comp

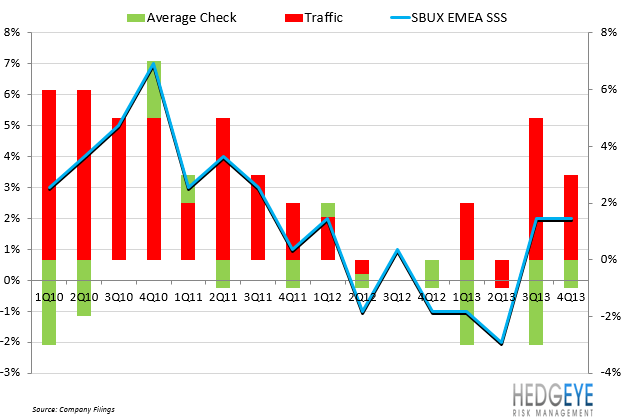

EMEA:

- Revenues +3%

- SSS two-year comp decelerated 50 bps

- Operating margin +1,170 bps to 9.3%

- Indicated that an early turnaround may be underway

CAP:

- Revenues +29%

- SSS two-year comp decelerated 150 bps

- Operating income +46%

- Operating margin +440 bps to 37.5%

- Consumers are embracing the SBUX experience

- Recent negative media attention appears to be a non-issue

Channel Development Segment:

- Revenues +13%

- Operating income +30%

- Operating margin +450 bps to 35.6%

- Exceeded aggressive growth plans for Evolution Fresh

- Will continue to rollout new K-Cup flavors and varieties to the market in partnership with GMCR

Despite reporting a great 4Q13, the bears do have several legitimate concerns:

- Sentiment is largely positive

- Rich valuation

- Ability to sustain such strong trends will be difficult

- Elevated expectations could become an issue

While management did their best on the earnings call to reign in expectations for FY14, by guiding to full-year global comparable sales in the mid-single digit range, we suspect that the street is looking for more. This guidance did appear to be fairly conservative but, as CEO Howard Schultz implied, it would be foolish to guide to high single-digit or double-digit comps.

All told, SBUX remains the best-run company that we follow and the long-term TAIL continues to seem unlimited. The company’s geographical reach and size is highly impressive and management continues to find feasible, innovative ways to drive comp growth accretive to the whole SBUX system.

Howard Penney

Managing Director