Processing, Processing, ...

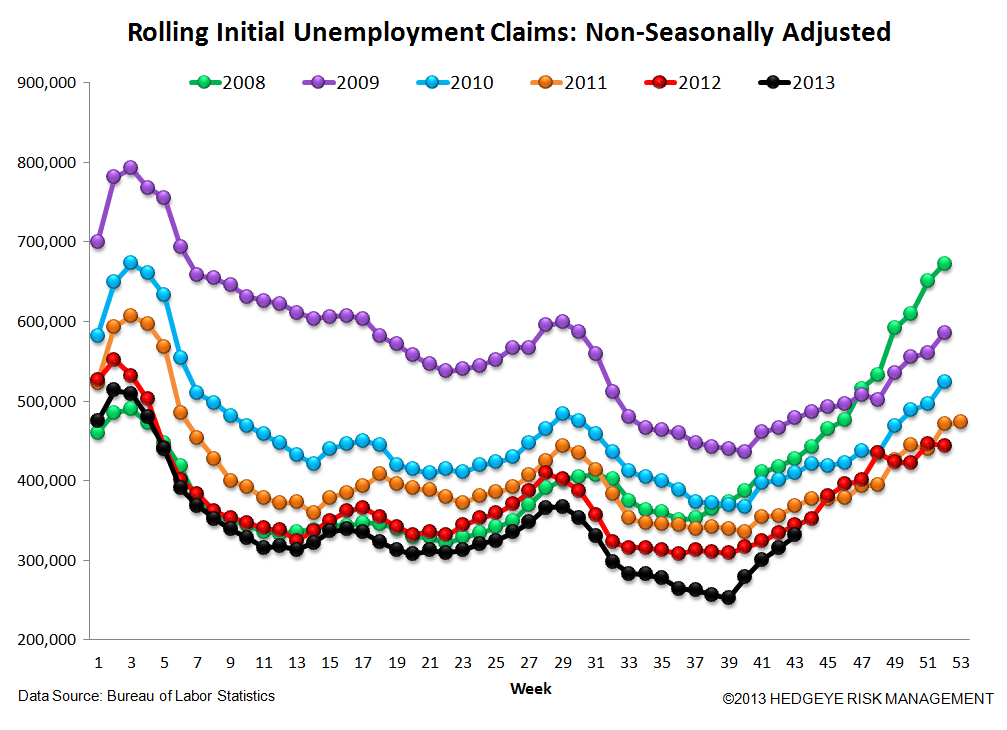

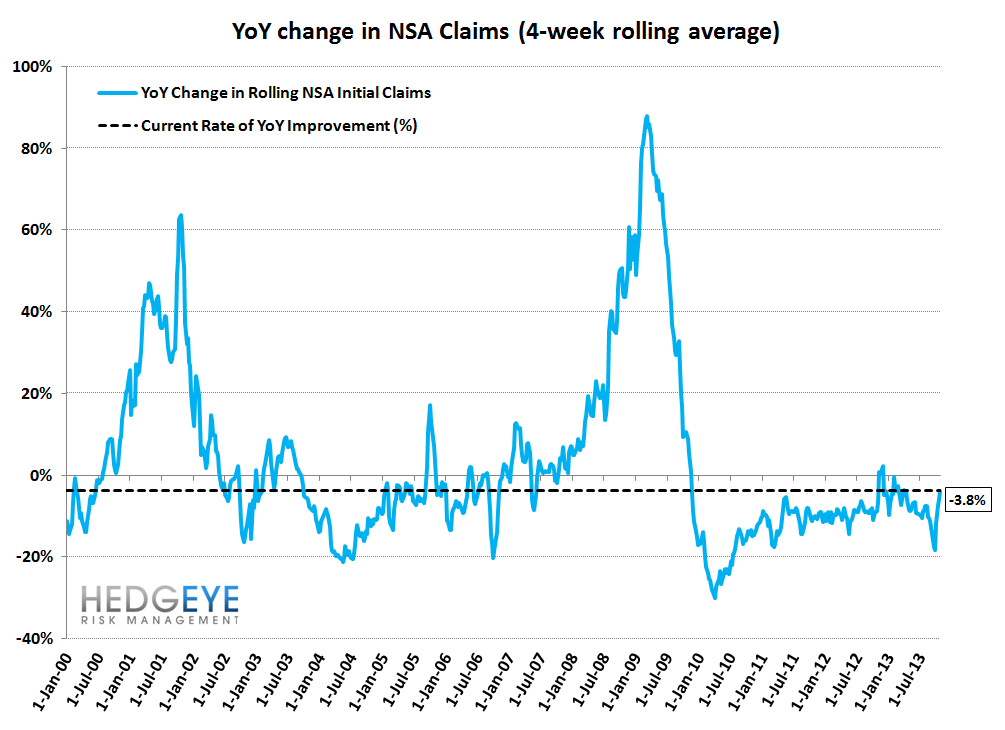

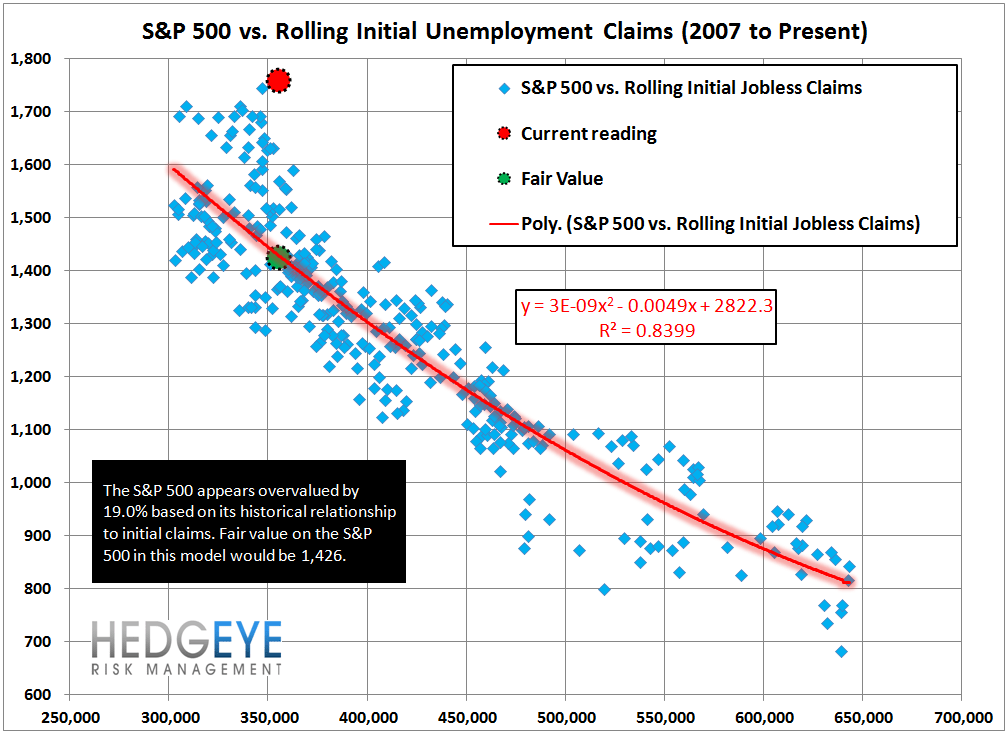

The labor market appears to have lost a step in the latest week, but conflicting reports over whether California's tech issues are finally out of the data make it hard to state definitively what is happening. The year-over-year rate of improvement in non-seasonally adjusted initial jobless claims slowed to 6.6% from 9.8% in the prior week. The state level California data, which is only available on a 1-week lag, is showing that CA claims were still running above the prior year level by ~15k. Assuming this 15k was still present in the data in the current week it would significantly alter the conclusion, as the data would instead appear to be resuming its pre-California/Govt shutdown run-rate. We expect greater clarity in the week ahead as we'll be able to see next week whether California's level of claims for this week were distorted.

Nuts & Bolts

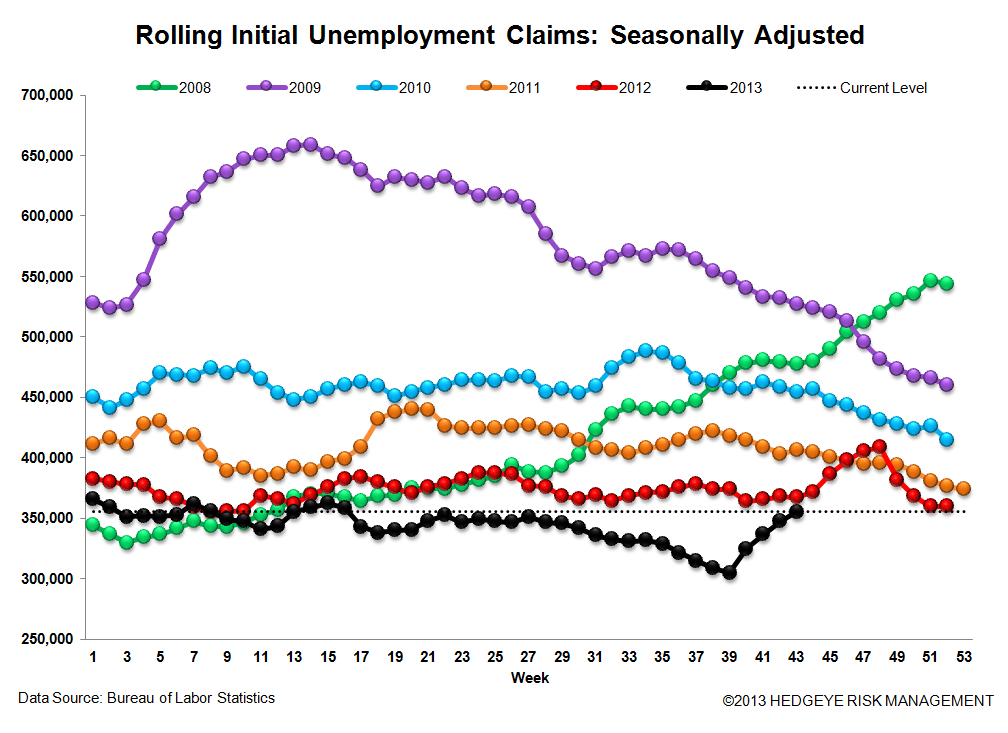

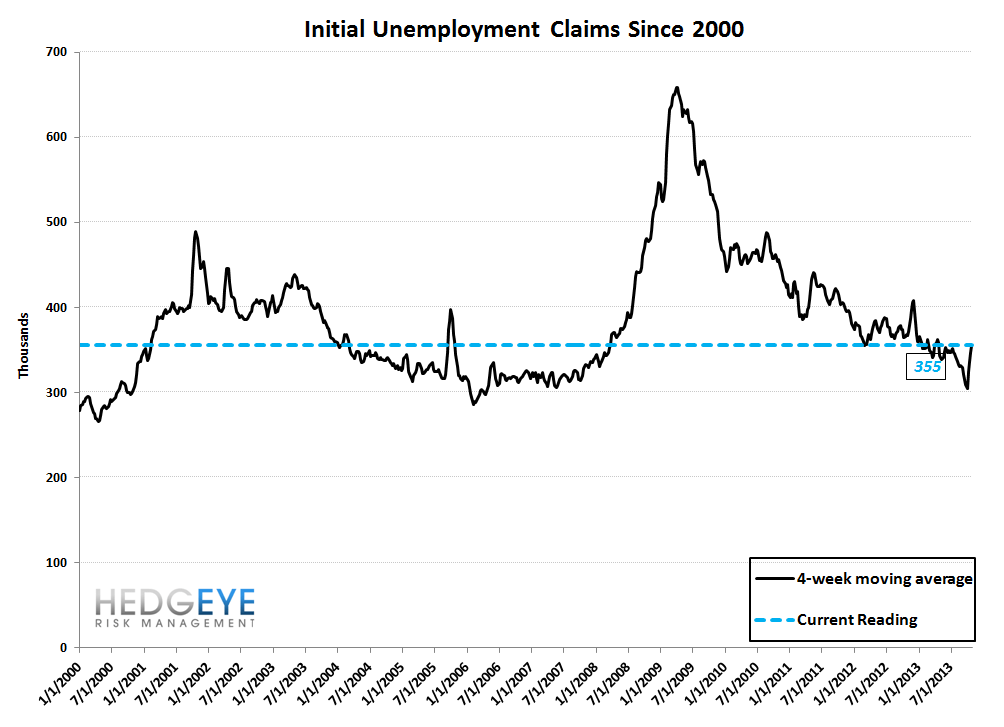

Seasonally adjusted initial jobless claims fell 10k to 340k WoW and there was no revision to the prior week's data. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 8k WoW to 355.25k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was lower by 3.8% YoY, which is a sequential deterioration versus the previous week's YoY change of -5.8%

Yield Spread

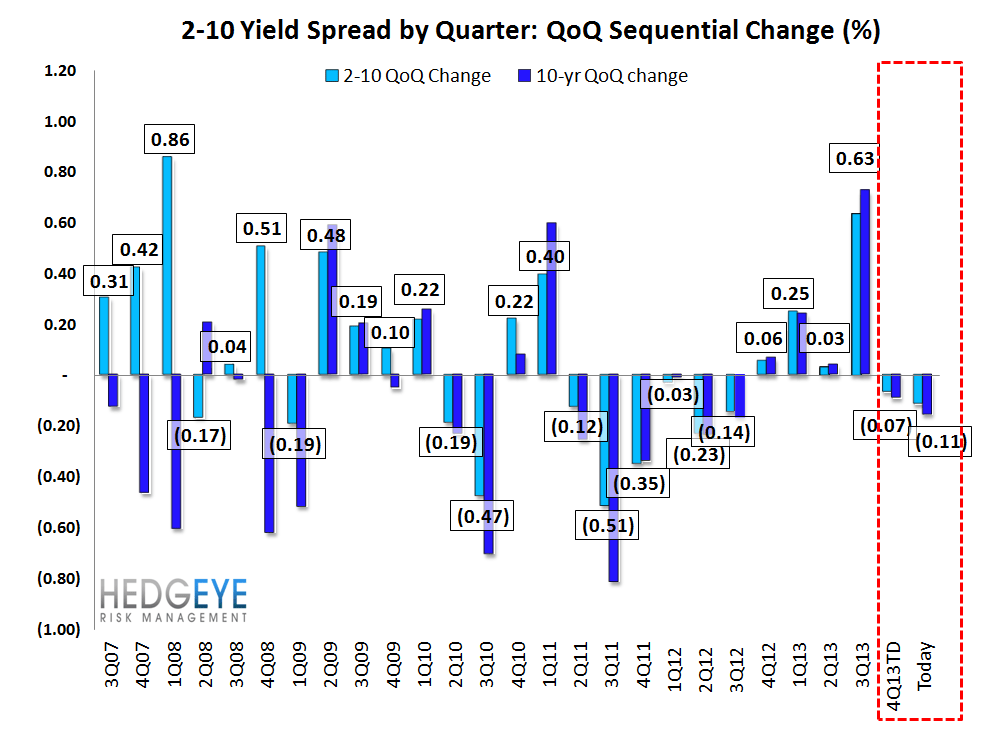

The 2-10 spread rose 4 basis points WoW to 223 bps. 4Q13TD, the 2-10 spread is averaging 227 bps, which is lower by 7 bps relative to 3Q13.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT