Investment Company Institute Mutual Fund Data and ETF Money Flow:

Total equity mutual fund flow broke to near all-time highs for the week ending October 23rd with a $13.5 billion total inflow into both domestic and world equity funds. Domestic equity mutual fund flow of $9.1 billion last week was an all-time record for U.S. stock funds in any 5 day period and eclisped the prior weekly record of $7.7 billion from the first week of 2013. As a result, total equity mutual fund trends in 2013 now tally a $2.8 billion weekly average inflow, a complete reversal from 2012's $3.0 billion weekly outflow

Fixed income mutual funds conversely continue to have persistent outflows. This week's tally, although a sequential improvement, measured another $2.3 billion withdrawn from bond funds which has pushed the 2013's weekly average fund flow to a negative $719 million. This compares to very strong trends which marked last year when bond mutual funds averaged a $5.8 billion weekly inflow

ETFs also experienced strong subscriptions last week, with inflows in both equity and fixed income products. Passive equity products experienced inflows of $13.0 billion for the 5 day period ending October 23rd with bond ETFs contributing $1.3 billion during the same time period. ETF products also reflect the 2013 asset allocation shift, with the weekly averages for equity products up year-over-year versus bond ETFs which are seeing weaker year-over-year results

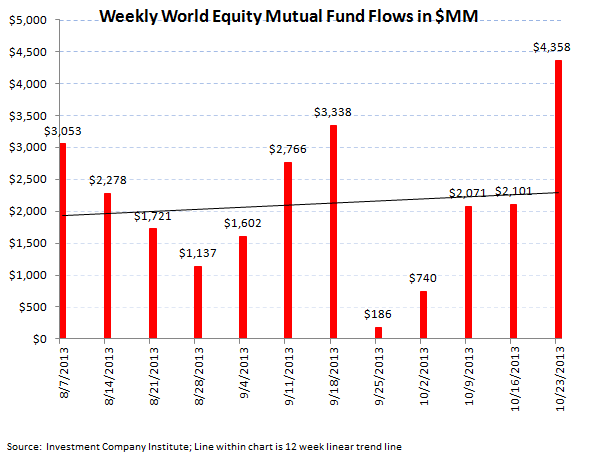

For the week ending October 23rd, the Investment Company Institute reported the second strongest weekly inflow into both domestic and world stock products in the history of the data set of $13.5 billion. The only other larger weekly inflow for total equities was during the first week of 2013 where $14.3 billion came into both fund classes. The domestic equity result of a $9.1 billion inflow was the largest U.S. weekly stock fund in history, larger than the prior record of $7.7 billion in the first week of the year and over 2.5x the best week in 2007. World stock fund inflows totaled $4.3 billion last week, the best 5 day result since the beginning of February 2013 and resulting in now 25 consecutive weeks of foreign stock fund flow. Including this week's new record high in domestic stock fund flows, the year-to-date weekly average for 2013 for all equity mutual funds has moved to a $2.8 billion inflow, a complete reversal from the $3.0 billion outflow averaged per week in 2012.

On the fixed income side, bond funds continued their weak trends for the 5 day period ended October 23rd with outflows staying persistent within the asset class. The aggregate of taxable and tax-free bond funds booked a $2.3 billion outflow, a sequential improvement from the $5.7 billion lost in the 5 day period prior, but still exhibiting weak trends. Both categories of fixed income contributed to outflows with taxable bonds having outflows of $1.3 billion, which joined a $1.0 billion outflow in tax-free or municipal bonds. Taxable bonds have now had outflows in 16 of the past 21 weeks and municipal bonds have had 21 consecutive weeks of outflow. While the sharp outflows that marked most of the summer and the start of the third quarter have moderated, the appetite for bonds has hardly rebounded. The 2013 weekly average for fixed income fund flows is now a $719 million weekly outflow, a sharp reversal from the $5.8 billion weekly inflow averaged last year.

Passive Products:

Exchange traded funds mirrored the trends in mutual funds with a strong result from equity ETFs and a weak performance from fixed income passives. Equity ETFs posted a $13.0 billion inflow, the third largest weekly inflow for equity ETFs all year. The 2013 weekly average for stock ETFs is now averaging a $3.3 billion weekly inflow, a 50% improvement from last year's $2.2 billion weekly average inflow.

Bond ETFs managed an inflow for the 5 day period ending October 23rd with a $1.3 billion subscription, breaking a trend of 3 consecutive weeks of passive bond outflows, but hardly a robust number. Despite this slight net new subscription in bond ETFs, 2013 averages are flagging with just a $275 million average weekly inflow for bond ETFs, much lower than the $1.0 billion average weekly inflow for 2012.

Jonathan Casteleyn, CFA, CMT

Joshua Steiner, CFA