This note was originally published October 23, 2013 at 17:00 in Macro

As many of you know, one of the most esteemed gold bugs of our generation is the venerable Eric Sprott of Sprott Asset Management in Toronto. Since 2000, he has obviously been spot on in his bullish call on gold, although this year has obviously been not quite so shiny (so to speak) for the gold bulls.

Yesterday, Sprott wrote a note to the World Gold Council effectively questioning their projections for short term supply and demand for physical gold. Admittedly, he actually raises some interesting points, in particular the idea that even though physical gold in ETFs has been in free fall this year, it appears unlikely to go much lower from current levels.

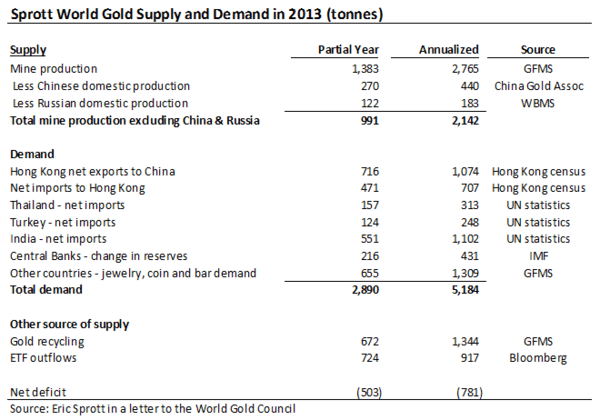

On a higher level, Sprott’s point that the available statistics on gold are misleading to the extent that they may be overstating the available supply of and thus negatively impacting the price of gold is an interesting one and worth investigating further. In the chart below, we’ve re-created Sprott’s table that was attached in his letter to the World Gold Council.

The table shows that demand for gold, according to Sprott, is clearly out stripping supply. In his analysis, Sprott nets out both Chinese and Russian domestic production from the world market, which he argues never leave the country and are consumed directly internally. He also excludes about 400 tonnes a year in technology demand, which he believes is double counted. On the flip side, Sprott excludes what the GFMS dubs “OTC investment and stock flows”, which is a name for a plug of sorts that represents the gold traded in the OTC market.

In summary, based on Sprott’s analysis there will be a deficit of supply this year of more than 780 tonnes. If he is correct, and if gold in fact trades off of supply and demand, then the sell-off in gold this year is truly because the consensus misunderstands the global supply and demand dynamics. Or, alternatively, there are other key factors driving the price of gold, which we will touch on shortly.

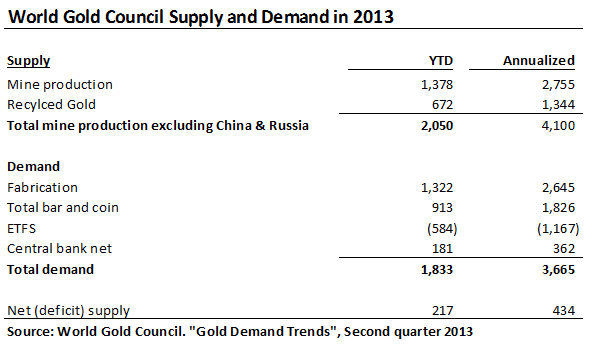

The counterpoint to Sprott’s case is that aggregate gold demand is down based on the World Gold Council’s numbers for the year-to-date. According to the World Gold Council, demand actually fell by 12% in Q2 2013 from Q2 1012 to 856.3 tonnes. This is just about 20% below the 5-year average quarterly demand for gold. Clearly, this is a very different story than Sprott’s numbers outline. In fact, as we show in the table below, the world gold council shows an over-supply of gold in the year-to-date.

Sprott’s full year estimates vary from the World Gold Council’s annualized numbers by 1,215 tonnes in aggregate. On a notional basis, the supply and demand difference between the two sets of estimates is $52 billion. This is a difference that is big enough to drive a very large truck through. So, who is right? Well, simply, the market seems to be saying the World Gold Council has nailed this one.

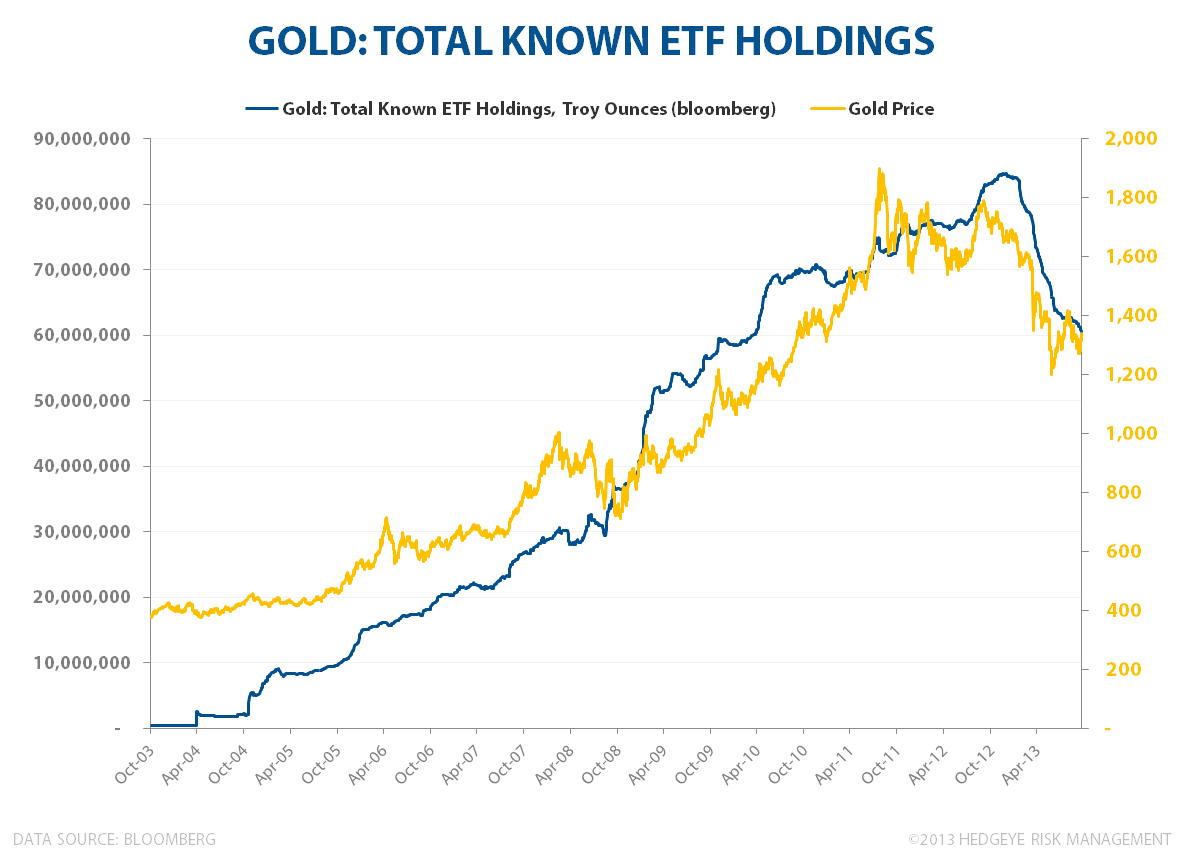

One point both groups agree on, which is very transparent data, is that the financial demand for gold via ETFs has fallen dramatically this year. Through the first two quarters of the year, the gold held by ETFs has declined by 579 tonnes.

But given the clear opacity in global supply and demand numbers for gold, we would actually posit another thesis, which is that perceived supply and demand is not the key driver of the price of gold at all and both sets of estimates are merely noise. In the chart below, we show one of the strongest correlations we’ve seen over the last five years, which is the gold price versus the Federal Reserve balance sheet.

From 2008 – 2012, this correlation was about as tight as we’ve seen in our factoring models with a r-squared of 0.90. The chart also shows that in 2013, this relationship broke down in emphatic fashion. Investors began to sell gold as economic data accelerated and in effect began front running a change in policy course from loosening to tightening.

The largest decline in demand for gold this year has come from a decline in demand from ETFs, or the financial markets. As the chart below highlights, the price of gold and value of gold in ETFs has increased in lockstep for the last decade and declined in lock step starting about a year ago with the initial correction in the price of gold leading the exit of physical gold from ETFs.

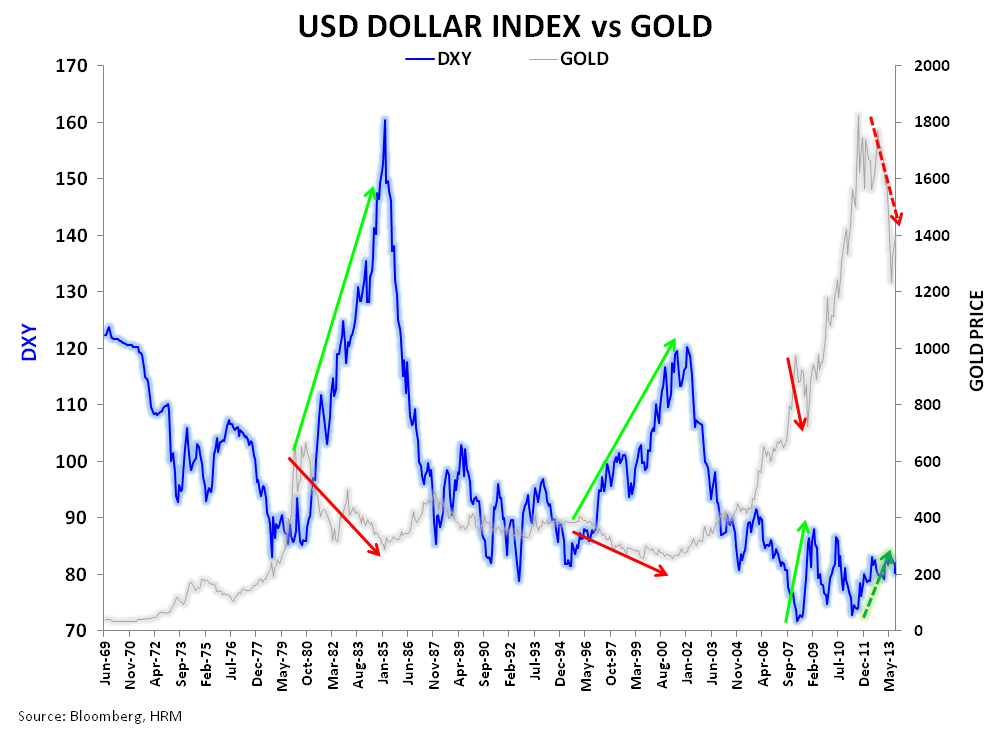

Ultimately, the true supply and demand dynamics for gold are difficult to determine, but we would argue that on some level they should likely be ignored. The best predictor of gold prices will continue to be the direction of monetary policy both in the United States. Loose monetary policy and a subsequent weak dollar, will create monetary inflation and inflate both the price of gold in real terms and lead to increased demand for gold as a store of value.

In the long term chart below, we see this relationship play out in spades going back to 1969. Consistently, a protracted increase in the value of the dollar has lead to a commensurate decline in the value of gold and vice versa. Interestingly, the recent spike we have seen in the value of gold in the last ten years coincides nicely with the advent of financial demand for gold via ETFs. But undoubtedly just as ETFs have created a multiplier on the way up, they have potential for creating a multiplier on the way down.

Daryl G. Jones

Hedgeye Risk Management Director of Research