Summary

We have been looking to “buy” niche construction equipment companies at reasonable prices, in part to pair with “short” CAT. We “added” TEX in June, but we would turn to MTW here. We see the potential for MTW to transition from a Crane segment orders story to a break-up/activist story. A rough MTW sum-of-the-parts suggests a break-up value of around $27 - $44/share, indicating between 30% and 115% upside from the current price. While we are not the first to observe that a crane OEM and a foodservice equipment business make strange bedfellows at a mid-cap industrial, we think several factors have changed that could force a reckoning in coming quarters:

- Investors are having increasing difficulty finding undervalued investments with the market near all-time highs.

- Activism has more frequently entered the picture with just a whiff of value to unlock; close MTW peer OSK has proven a notable success.

- The M&A market is picking up, potentially facilitating transactions. The IMI PLC foodservice equipment unit sold this month to BRK competes with MTW.

- A rebound in non-residential construction activity into 2014 is likely to draw greater interest in and scrutiny of MTW.

- Europe is less of a mess, U.S. state/local finances have improved and developed market infrastructures spending may have some light at the end of the tunnel (e.g. ARTBA data).

There are buyers for both MTW divisions, likely at much higher prices than reflected in MTW’s current market value. While there had been an activist shareholder at Manitowoc until the middle of this year (they apparently switched to TEX), there was little motion and greater agitation seems likely unless the share price moves to better reflect a potential break-up. MTW is not risk free here, but the downside appears fairly limited relative to both the potential return and investment alternatives, by our estimates.

Key Points

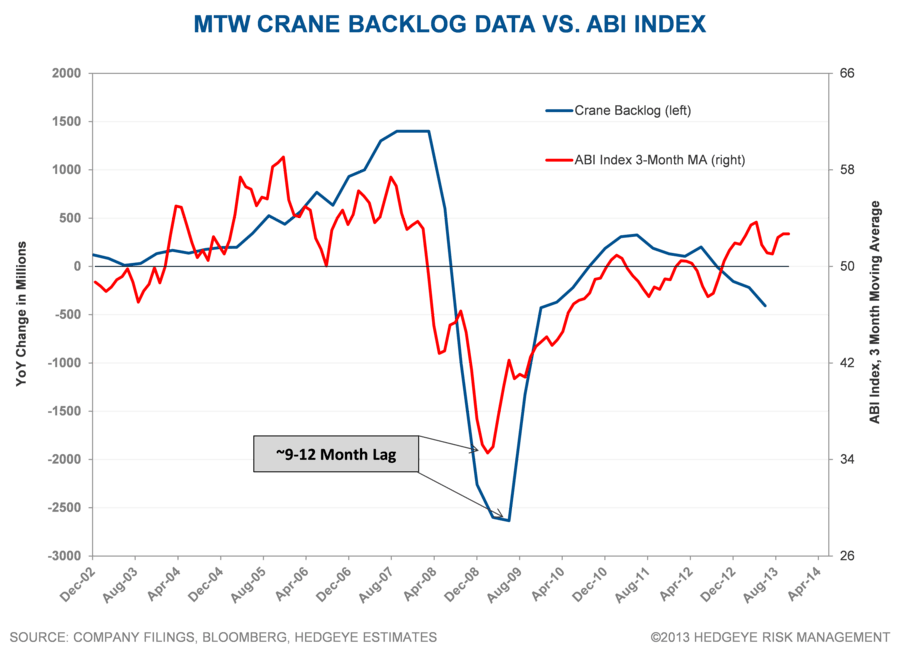

Response to Weak 3Q: MTW’s third quarter results last week were not exactly robust. We held off MTW into the release, figuring that the shares would decline following disappointing Crane segment order results. Implied orders in the Crane division fell 22.6% YoY, the worst showing since the financial crisis. Worse, management did not lower guidance, backend loading 4Q and setting up a probable 4Q shortfall. Inventories looked problematic. While there were some rumblings of increased quote activity and new products, the report was weak. However, MTW shares rallied. Maybe the market reaction was wrong, but we don’t think so. To us, this suggests that the focus is shifting to the broader MTW opportunity and has moved past the small ball of calling volatile quarterly crane orders.

Good Businesses, Good Price: Finding undervalued industrials with solid market positions in good industries has become increasingly difficult with the market near all-time highs. Manitowoc has two well positioned divisions in structurally favorable industries. The crane industry is consolidated and profitable through the cycle, even if highly cyclical. MTW is widely recognized as producing the Cadillac of cranes – no small benefit when operators have been criminally prosecuted for accidents. The crane recovery is likely to be fairly muted given the long life cycle for the equipment (say 15-50 years), but it is likely to be a recovery nonetheless. Foodservice equipment has many favorable characteristics that drive relatively high margins. Foodservice equipment customers are sophisticated buyers that pay for equipment with superior performance. That customer focus on product innovation and performance favors better resourced, larger competitors like MTW.

“We invest in cranes from leading manufacturers that have a wide market acceptance, such as Liebherr, Manitowoc/Grove, Terex, Kato and Tadano….[and] avoid investment in less recognised brands, one-off, specialised, prototype or unusual model cranes.” – Boom Logistics LTD, 2013 Financial Report

Scenarios to Consider

A benefit of a MTW break-up is the apparent flexibility in how it is executed. For starters, who really wants to watch MTW stumble through ERP implementation into 2016? Why are these two unrelated businesses supporting a chunky $70 million/year corporate line? Acquirers would have the infrastructure and platforms to operate these businesses without so much effort and overhead. On the other hand, if MTW were to sell one division and keep the other, it could build a better focused franchise. Capital from the sale of one division could be redeployed to build the scale and product portfolio to serve the remaining division’s markets.

“ITW is a conglomerate. They do a lot of other things. Foodservice is not their core competency. Manitowoc, even though they -- foodservice is a big part of their business, they still do cranes …and other stuff.” – Middleby on Manitowoc 3/12/12

Selling the Cranes Segment: Mining & construction equipment companies are desperately trying to refocus on construction as mining equipment sales evaporate. That is one reason pricing in many construction equipment categories has been weak (e.g. CAT’s Cconstruction Industries). Bucyrus long ago manufactured cranes; it doesn’t take a rocket scientist to see that there are likely to be synergies between the Bucyrus shovel business and MTW’s crane division - certainly more than between cranes and ice machines. We think CAT is a potential buyer, but Komatsu, Hitachi or other global construction equipment makers could also be interested. Chinese crane manufacturers are likely to increase competitive pressure over the next decade. A CAT or Komatsu might better manage those changing dynamics, and both would probably love a little more revenue right now. We would expect a sale to competitors like TEX or Liebherr to hit antitrust hurdles.

Selling the Foodservice Equipment Segment: While Middleby is not perfect, the roll-up strategy certainly seems to be working for investors. Middleby is focused on consolidating a relatively fragmented industry, while we are not quite sure what Manitowoc’s strategy is. Potential buyers for parts of this business include Middleby itself, ITW (competed for Enodis in mid-2008, but 'lost' to MTW), Marmon or Electrolux. This is not to say that Manitowoc is running the business badly, but rather that the assets would likely fetch a higher valuation if sold than what is currently reflected in MTW’s share price.

Keeping Foodservice: A Crane segment sale while retaining the Foodservice Equipment segment is not such a bad option. The proceeds of a Crane segment sale could be used to chase Middleby’s strategy. As the table below shows, if the market applied Middleby’s valuation to Manitowoc’s Foodservice Equipment revenue, just that segment’s valuation would substantially exceed MTW’s current enterprise value. We know there are differences in product categories, like refrigeration, and a MIDD valuation might be a stretch, but the potential is likely there.

Keeping Cranes: If MTW divested the Foodservice Equipment division, it could allow entry into adjacent niche construction equipment markets. While this may seem less attractive, MTW would still be investing or acquiring into a cyclically depressed market.

Worked for OSK: While it was a bumpy ride for investors, the value opportunity at Oshkosh was eventually forced on the market by activist involvement and broader recognition of the value opportunity. MTW could well be the next OSK.

Sum of Parts: While a sum of the parts based on related company or comparable transaction values can help frame the opportunity, we are not always big fans of the approach, only begrudgingly presenting one for FDX for instance. There are differences between MTW and the businesses shown, the valuation is subject to market volatility, and it is subject to the biases inherent in the selection of comparable companies – there are a number of potential complaints. However, when the gap between the estimated value and the current market value is large, as it is here, we think a sum of the parts can be very useful. In this case, the sum of the parts valuation range is not far off of our updated base-to-bull DCF fair value range of $19 to $32. It appears to us that this value will be unlocked one way or another.

Background & Risk: We have presented additional industry background in our Mining & Construction Equipment black book and expect to provide more detail on MTW. Feel free to ping us for more background as well. The most obvious risk is that we are buying into a likely 4Q Crane segment disappointment – and longer term, the crane cycle is likely to be fairly muted. However, weak results may prove oddly beneficial as an activist incentive. Our valuation highlights a favorable risk-reward tradeoff, but it is largely dependent on others accepting the re-framing of Manitowoc from an operating company traded on quarterly result to a prospective break-up, valued on a sum of its parts.

Implementation Challenges: We do not see provisions that would necessarily preclude activist involvement, but they could be implemented in an attempt to thwart such efforts. Manitowoc Crane segment distribution and service might be difficult to migrate to a CAT or Komatsu type dealer/distribution network. We do not view these as insurmountable challenges, but we could certainly be proven incorrect in that assumption.