Today, Ruby Tuesday announced the resignation of its Chairman Matt Drapkin. Drapkin, who recently sold 1.45mm shares, joined the board of RT three years ago as an activist that, along with Carlson Capital, was intent on enhancing shareholder value.

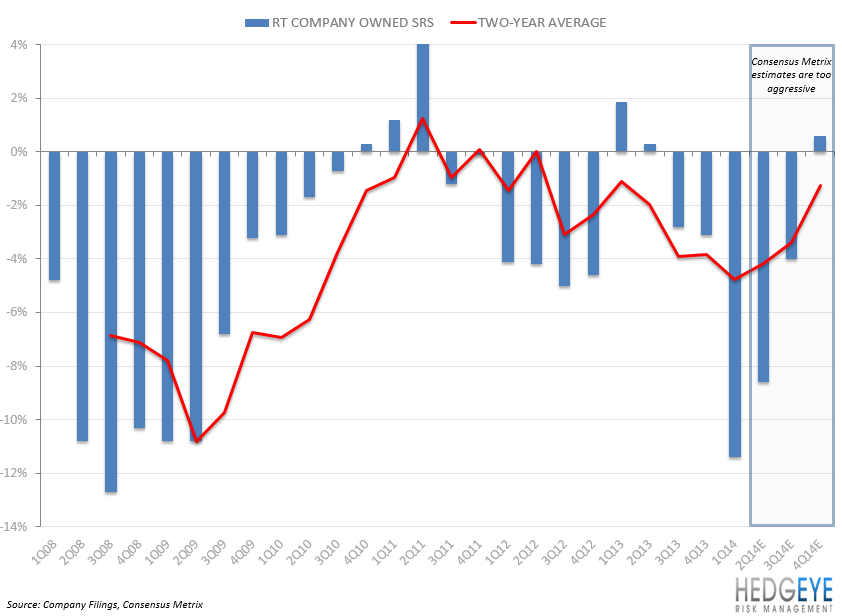

He is now being replaced by the company’s current CEO James Buettgen, who left Darden in December of 2012 in order to resuscitate the Ruby Tuesday brand. Despite an attempt to revive the business, RT’s operating fundamentals remain some of the worst in the casual dining industry. To make matters worse, there appears to be little hope for a turnaround – RT has only seen one quarter of positive same-restaurant sales, on a two-year basis, since FY3Q08.

Furthermore, we believe the largest impediment to the revitalization of this fourth tier Bar & Grill brand is Chili’s, which is run by a very strong management team. In EAT’s recent quarterly earnings call and our subsequent call with CFO Guy Constant, the company announced its intent to pursue an aggressive strategy in order to grow same-restaurant sales. This includes increasing TV media spend to support new products (including the upcoming Tex-Mex platform), implementing new online ordering for its “to go” business, and rolling out its delivery service.

Importantly, Chili’s will be moving its successful re-image program to the state of Florida in the coming months. Currently, 10.9% of RT’s system-wide domestic units are in the state of Florida, making it the company’s most important state. This means that RT is heavily exposed to any success that Chili’s may have in the region. If Chili’s is able to steal significant market share in Florida, RT’s business will suffer. If the past is any indication, this could very well happen. Look at BJRI’s recent quarterly results – they were downright ugly. We believe that Chili’s re-image program in California had a significant impact on market share trends in the region. On the margin, this is all good news for EAT and their core brand, Chili’s.

RT’s management team has guided to an improvement in sales directionally throughout the year and the street has reflected that in its estimates. We are highly suspect that this will unfold as planned, and believe that further disappointments are likely.

Capex has been reduced significantly since FY08, as the company is having a difficult time making ends meet. EBITDA was negative in 1Q14 and the company continues to lose money. We could see a major restructuring charge coming and believe that a significant number of store closings are needed. If not, the company could be headed for Chapter 11.

Howard Penney

Managing Director