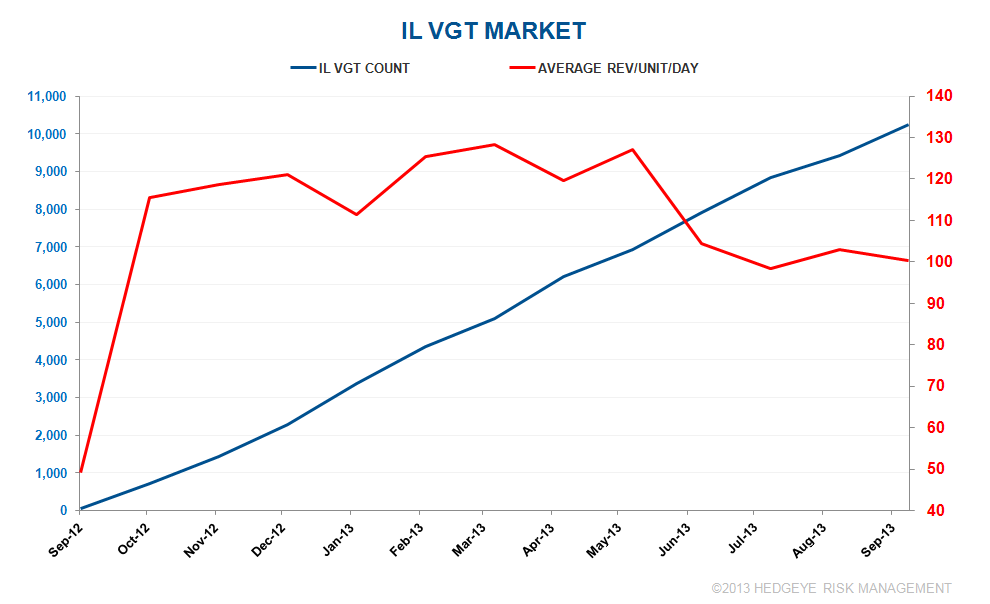

- At the end of September, there were 10,250 VGT’s up and running, up 9% (833 units) MoM

- Since the market opened last September, average monthly installations have trended at 849 units

- Using an average of the machines outstanding at the end of August and September, average daily win per device was $100/day in the month of September, in-line with the average for the last 3 months. As the chart below shows, despite recent added supply, daily win day has remained steady around the $100 level.

- As of October 24, there were still 1,554 establishments pending approval. If approved, these establishments can add a maximum of an additional ~7,770 machines. This implies a market size of roughly 18-20,000 VLTs, unless Chicago opts in. At the current pace of installations, we expect shipments to IL to taper off materially by the summer of 2014.

- Supplier impact:

- IGT has been shipping about 1,000/ Q to IL which translate to about 5 cents a year of EPS impact

- During the last 2 quarters, BYI’s shipped 1,369 to IL and 1,943 units over the last twelve months. An additional 2,000 VGT unit shipment to IL should translate to about $0.25 cents in earnings for BYI.