“The powers delegated by the proposed Constitution to the federal government are few and defined.”

-James Madison

In other news, one of Bloomberg’s leading headlines this morning takes the other side of Madison’s Federalist Papers: “Yellen Poised to Rival Obama with Financial Power.” Isn’t that just terrific!

Have no #EOW (end of world) fear, yet. There are plenty of voices in America (and abroad) who still believe that an un-elected, un-checked, and un-accountable Federal Reserve is about to meet its maker – The People.

“Unlike the modern Statist, who defies, ignores, or rewrites the Constitution for the purpose of evasion, I propose that we, the people, take a closer look at the Constitution for our preservation.” –Mark R. Levin, The Liberty Amendments (pg 12)

Back to the Global Macro Grind…

I’m not a Tea Party person, but I often wonder why more dogmatic Democrats don’t show “folks” like Mark Levin some love. Some of these Constitutionalists hate the Republican party more than Dems do!

Irrespective of your politics or Sox/Cards affiliation, every morning in America is a great one where we can “take a closer look at the Constitution” and the un-precedented power both Bush and Obama have put in the hands of Bernanke and Yellen.

I read Levin’s new book in 8 hours. At a bare minimum, it was worth my time to re-realize what I didn’t remember about the US Constitution. At a maximum, it made me think. Unless Americans want their currency to burn, Venezuelan style, they better start thinking about this, and fast, too.

Last week’s US #GrowthSlowing signals in equities we’re definitely considering what Down Dollar, Down Rates means:

- Slow-Growth Indices led last week’s US stock market strength: Utilities (XLU) +2.0%, REITS +1.8%, MLPs +1.7%

- Pro-Growth Indices flashed their 1st major negative divergence of 2013: Russell2000 +0.3%, Financials (XLF) -0.2%

If you broaden your vantage point to currencies and commodities, you can see the causal Fed factor at work here:

- US DOLLAR: down another -0.6% last wk and down -3.4% in the last 3 months to now NEGATIVE -0.7% YTD

- GOLD: up another +2.7% last wk and up +1.7% over the same 3 month period as Mr. Market front-runs the Fed

All the while, what the Fed is really sponsoring here (volatility instead of price stability) flashed its 1st major divergence versus the “US stock market at all-time highs” thingy in 2013. Stocks up = VIX up.

Not to be confused with every other US equity market rally of 2013 that we were long of (we’re short this one):

- US Equity Volatility (VIX) is making a series of higher-lows (instead of lower-lows) now

- The 11-handles that the VIX saw in both March and August of 2013 were aligned with US #GrowthAccelerating

No, this has nothing to do with being a Republican or Democrat. It has nothing to do with social issues either. It has everything to do with Mr. Market’s expectations of what causal impact the Fed’s “no-tapering” decision could have on the slope of US economic growth.

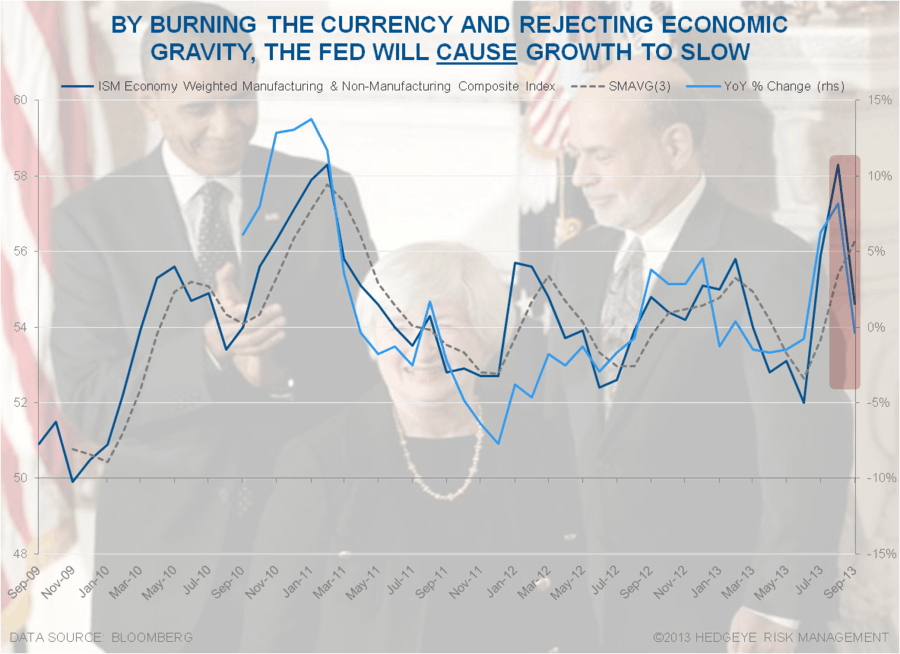

To review US economic growth’s slope in 2013:

- #GrowthAccelerating: Q4 2012 GDP of 0.14% accelerated to +2.48% by Q2 of 2013

- ISM and PMI “New Orders” pinned 60-handles in Q3 of 2013

- The first batch of OCT 2013 weekly and monthly US economic data has slowed, sequentially

“Sequentially” is an important word. How many of your favorite political market/econ pundits could even tell you what it means? *Hint: slope of the line.

And away from this week’s FOMC decision to pander to the Bond Bull Lobby, you’ll be getting more of what you saw in the US Consumer Confidence (U of Michigan survey) last week (73.2 OCT vs 77.5 SEP, #GrowthSlowing). Here’s the Macro calendar:

- Thursday: Chicago PMI for October should slow sequentially from September’s 55.7

- Fiday: ISM for October should slow sequentially from September’s 56.2

I know. Who cares? It’s all about the Fed right? Yeah, right.

More like it’s all about your investing Style Factors. To get those right, you need to get the slope of these growth lines right.

And if, god forbid, we take a few hours to consider the Constitutional conflict of interest in the Fed trying to “smooth” things embedded in the line (like gravity and/or growth), we might actually drive ourselves right nuts.

I can get nuts. I felt nuts selling at the all-time highs of October 2007 too.

Our immediate-term Risk Ranges are now as follows:

UST 10yr Yield 2.44%-2.60%

SPX 1

DAX 8

VIX 11.59-14.96

USD 78.72-79.71

Gold 1

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer