TODAY’S S&P 500 SET-UP – October 28, 2013

As we look at today's setup for the S&P 500, the range is 36 points or 1.18% downside to 1739 and 0.87% upside to 1775.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.21 from 2.21

- VIX closed at 13.09 1 day percent change of -0.83%

MACRO DATA POINTS (Bloomberg Estimates):

- 9:15am: Capacity Utilization, Sept., est. 78.0% (prior 77.8%)

- 10am: Pending Home Sales m/m, Sept., est. 0.0% (prior -1.6%)

- 10:30am: Dallas Fed Manufacturing , Oct., est. 9 (prior 12.8)

- 11am: Fed to purchase $4.25b-$5.25b in 2017-2018 sector

- 11:30am: U.S. to sell $34b 3M bills, $30b 6M bills

- 1pm: U.S. to sell $32b 2Y notes

- 2pm: Monthly Budget Stmt, Sept., est. $67.0b (prior $75.2b)

GOVERNMENT:

- House, Senate in session

- FCC discusses rural comms., 700MHz commer. spectrum, 11:30am

- U.S. Mortgage Bankers Assn annual convention; speakers include former President George W. Bush, Fannie Mae CEO Timothy Mayopoulos, Freddie Mac CEO Don Layton, CFPB Director Richard Cordray, Sen. Elizabeth Warren, D-Mass.

WHAT TO WATCH:

- JPMorgan to pay $5.1b to settle w/ Fannie, Freddie: FHFA

- Provenge maker Dendreon said to be seeking takeover offers

- Obamacare insurance websites limited by Verizon data failure

- Snapchat financing round may value co. at $3.5b: AllThingsD

- Facebook said to be rebuffed by Snapchat over possible deal

- China signals “unprecented” policy changes at Plenum

- Pension funds move into reinsurance’s cat risk business

- DirecTV, Time Warner Cable said to consider Aereo-type services

- Disney to show new cartoon through iPad first, NYT says

- Numericable said to seek IPO valuation of up to $8.3b

- Twitter IPO test-run successful, WSJ says, citing NYSE

- GM looking to expand lead in China with Chevy SUVs

- Ford CEO doesn’t regret conservative China approach: SCMP

- Idaho debates use of private prisons, WSJ says

- U.K. storm leaves 220k homes w/o power: U.K. Energy Network

- “Bad Grandpa” takes first place at N. Am. wknd box office

- Retail sales probably slowed in Sept.: U.S. Economy Preview

- Fed Meeting, BOJ, Iran Talks, Apple: Wk Ahead Oct. 26-Nov. 2

AM EARNS:

- Biogen Idec (BIIB) 6:30am, $2.09

- CNA Financial (CNA) 6am, $0.76

- Loews (L) 6am, $0.77

- Merck (MRK) 7am, $0.87 - Preview

- Roper Industries (ROP) 7am, $1.45

- Scorpio Tankers (STNG) 7:56am, $0.01

- Tenneco (TEN) 8am, $0.94

PM EARNS:

- Allison Transmission Holdings (ALSN) 4:01pm, $0.38

- American Capital Agency (AGNC) 4:01pm, $0.81

- Amkor Technology (AMKR) 4:09pm, $0.10

- Apple (AAPL) 4:30pm, $7.91

- Arch Capital Group (ACGL) 4:01pm, $0.92

- CNO Financial Group (CNO) 4:03pm, $0.28

- Edwards Lifesciences (EW) 4:01pm, $0.66

- Extra Space Storage (EXR) 4pm, $0.52

- FMC (FMC) 4:15pm, $0.84

- General Growth Properties (GGP) 4:01pm, $0.28

- Hartford Financial Services (HIG) 4:15pm, $0.84

- HealthSouth (HLS) 4:30pm, $0.43

- Herbalife (HLF) 4:10pm, $1.14

- Integrated Device Technology (IDTI) 4:01pm, $0.08

- Macerich (MAC) Aft-mkt, $0.83

- Masco (MAS) 5:09pm, $0.25

- Norwegian Cruise Line (NCLH) 4pm, $0.85

- Oceaneering International (OII) 5:01pm, $0.94

- Olin (OLN) 6pm, $0.64

- Plum Creek Timber (PCL) 4:04pm, $0.42

- PMC-Sierra (PMCS) 4:05pm, $0.10

- Riverbed Technology (RVBD) 4:05pm, $0.23

- Seagate Technology (STX) 4:01pm, $1.31 - Preview

- Titan International (TWI) 4:30pm, $0.25

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Copper Rises for Third Day on Speculation Fed to Keep Stimulus

- Tin Advancing 8% for BNP as Indonesia Spurs Swings: Commodities

- Brent Rises From 11-Week Low Before Federal Reserve Meeting

- Gold Swings Near Five-Week High Before Fed Begins Policy Meeting

- Russia Cuts Gold Assets for 1st Time in Year as Prices Drop

- Palm Oil Gains as Much as 0.4% to 2,454 Ringgit, Erasing Losses

- LME Copper Premiums at Record High as Inventories Fall: BI Chart

- Crop Yields May Be Curbed by Australia Frost, GrainCorp Says

- Stocks Top Gold by Most Since ’97 on Fed Delay: Chart of the Day

- China Refinery Boom Cuts Margins for Asia Rivals: Energy Markets

- Zimbabwe Considering Structure of International Mining Bond

- Palm May Rally on Inverse Head-and-Shoulders: Technical Analysis

- Indonesia Coal Drowning Seaborne Market, Relief May Be Ahead

- Rubber Gains on Weaker Yen, Optimism Chinese Demand Will Rise

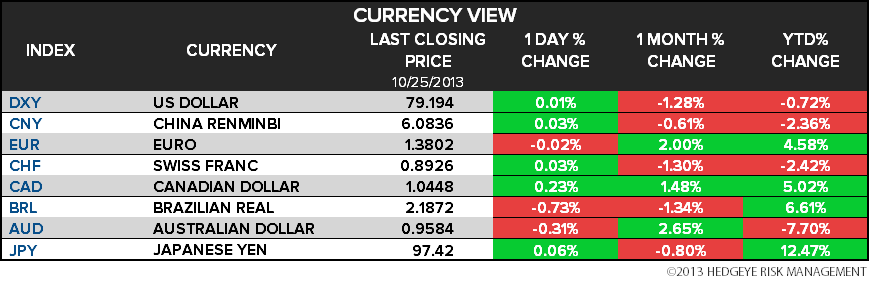

CURRENCIES

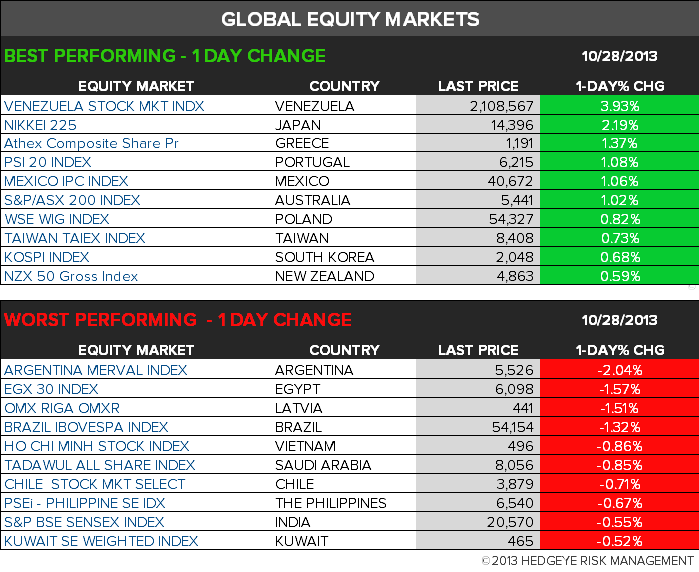

GLOBAL PERFORMANCE

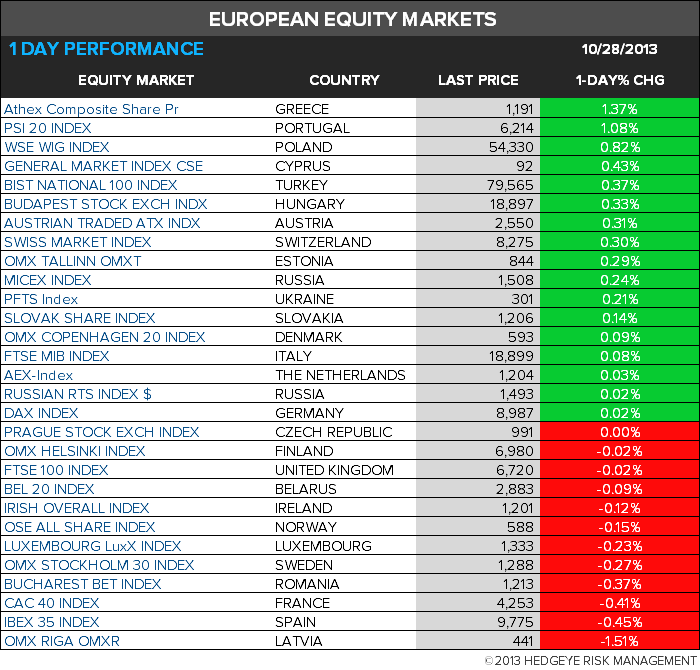

EUROPEAN MARKETS

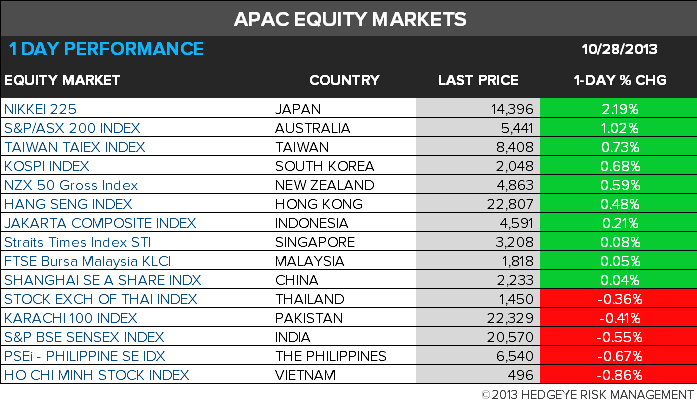

ASIAN MARKETS

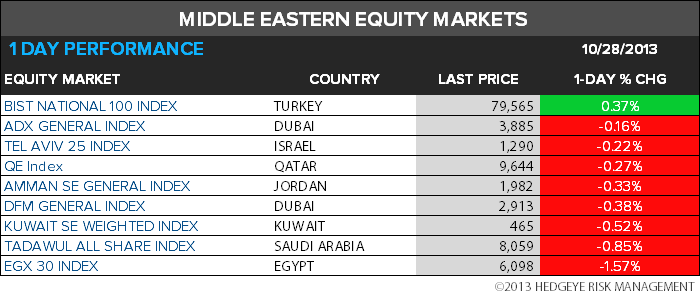

MIDDLE EAST

The Hedgeye Macro Team