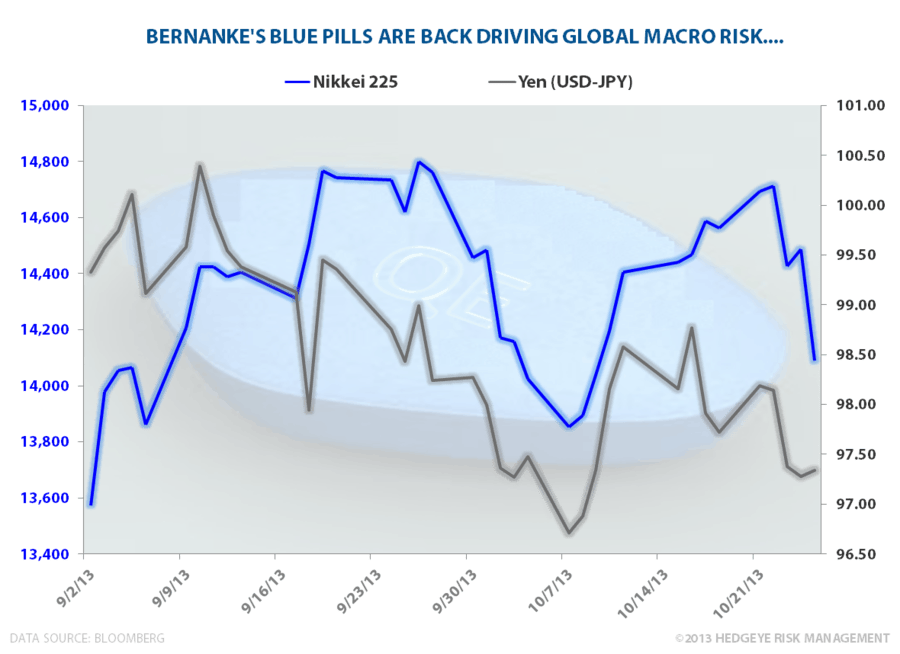

The Nikkei got smoked again for a -2.8% loss overnight. It's down -4.5% in the last 3 days. Got interconnected global macro market risk associated with Bernanke trying to bend economic gravity?

Expectations of global growth slowing are definitely bending now as the Fed’s balance sheet moves toward +$1 TRILLION year-over-year (+$998.1 billion in last night’s report). This is what happens when unelected central planners try to bend economic gravity using monetary Viagra.

Editor's note: This is a brief excerpt from Hedgeye morning research. For more information on how you can subscribe click here.