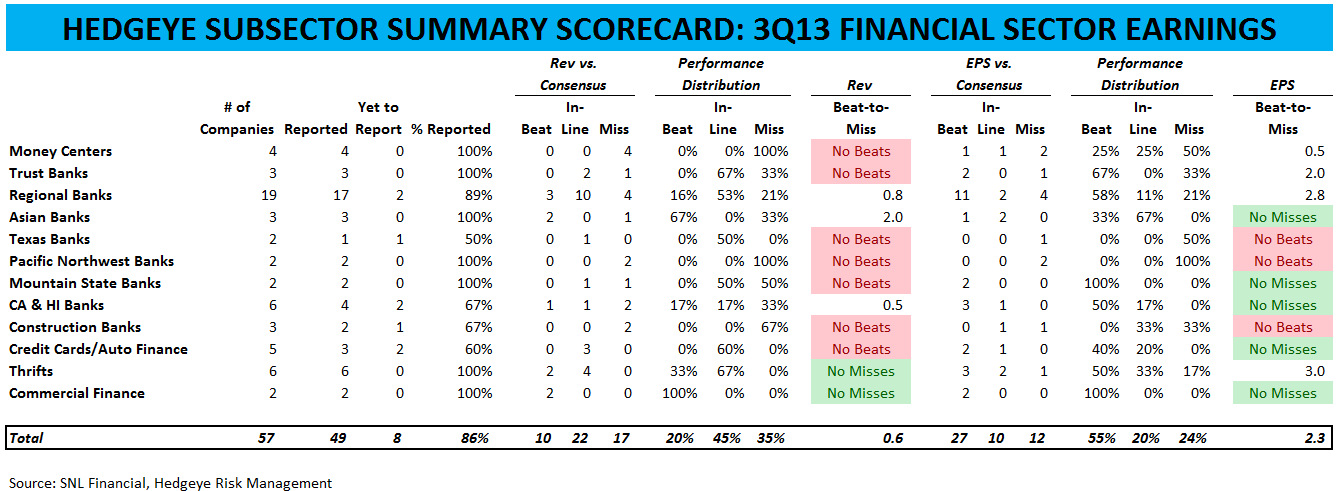

Not Beating Expectations, but Not Missing Either

As Financials earnings season starts to wind down, we find it useful to examine the trends that have emerged. Our Hedgeye Financial Earnings Scorecard below shows patterns in the results based on nine metrics and our own score of overall strength (from -10 to +10) for each issuer and in the aggregate. So far, the results have been quite mixed, with an overall score of zero, suggesting that, all things considered, things are coming in just about in line with expectations. The money center banks (-4), credit card companies (-2) and trust banks (-1) have generally disappointed, while the regional banks (+2) have been, on balance, more positive.

3Q13 Earnings Season Themes

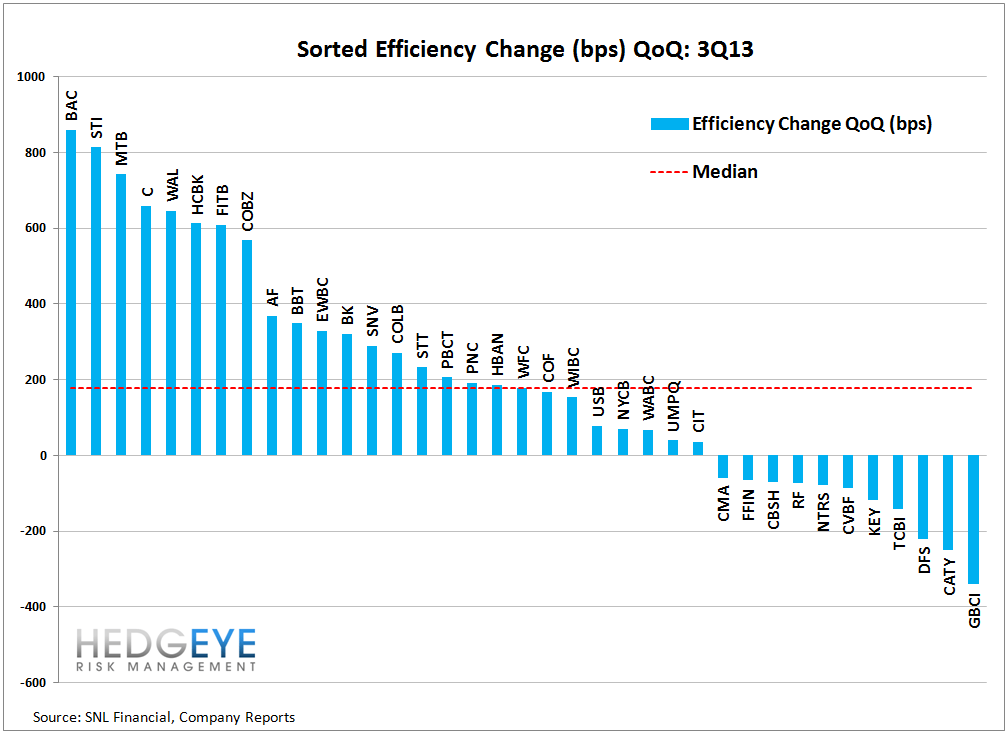

With the earnings season for Financials now largely in the rear-view mirror, it's clear that the strongest areas of contribution are still coming from credit with a preponderance of companies still showing sequential improvement in NCOs, NPAs and at least half of companies still seeing earnings contributions from reserve release. Efficiency actually deteriorated this quarter across the sector as well over half of companies have reported a sequential increase in costs relative to expenses. Regarding the top line, the news is generally positive. Almost three-quarters of companies are now reporting positive loan growth, albeit slow growth. The margin front also showed some improvement vs recent trends. Half of companies reported that NIM sequentially improved this quarter, up substantially from prior quarters.

- EPS: 26 out of 49 companies (54%) have beat consensus EPS estimates, while 11 have been in line, and 12 have missed (25%). Keep in mind that we are looking at the optical (unadjusted) numbers.

- Revenues: 10 out of 49 companies (20%) have beat consensus revenue estimates, while 22 were in line and 17 missed (35%). For reference, we consider +2%/-2% the threshold for a beat/miss on top line.

- Credit: 26 out of 49 companies have released reserves this quarter, or 53%. 13 of 49 (26%) have built reserves and the rest were essentially provisioning in-line with net charge-offs. NCOs were predominantly better again this quarter with 71% of companies reporting a sequential improvement in the level of net charge-offs. The data was better still on a forward-looking basis, where 88% of companies reported a sequential decline in NPAs.

- Margins: NIM pressure seems to be abating modestly. 49% of companies reported a sequential NIM increase while 51% reported a decline. On average, NIM was higher by 1 bps while the median NIM was unchanged sequentially. Some of the worst NIM changes came from ZION (-22 bps), CBSH (-10 bps), MTB (-10 bps), NYCB (-11 bps), PNC (-11 bps) and WFC (-8 bps).

- Loan Growth: 74% of companies reported positive loan growth this quarter, with the median company reporting +0.9% QoQ. The banks posting the most positive loan growth include HBAN, CBSH, GBCI (Acq-driven).

- Stock Performance: 48% of companies have seen their stock price rise on the trading day post earnings, and the average change has been +0.3%. Relative to the XLF, the average change has been -0.2%.

The chart below shows the percentage of companies that beat/missed earnings and revenue, the percentage that showed sequential improvement or deterioration by category, and the percentage that saw their stock prices rise/fall following earnings on an absolute and relative (vs XLF) basis.

The charts below show the best and worst performers in loan growth, NIM, and efficiency on a sequential basis.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT