Finding a bottom always seems easy, in hindsight....

As measures by the NAHB Housing Market Index (HMI) home builders remain cautious and concerned about prospects for the housing market, but that was yesterday; today's key data point was Commerce Department numbers showing that U.S. builders broke ground on more houses than forecast in May, another sign of a "bottom" that the manic media has leapt on.

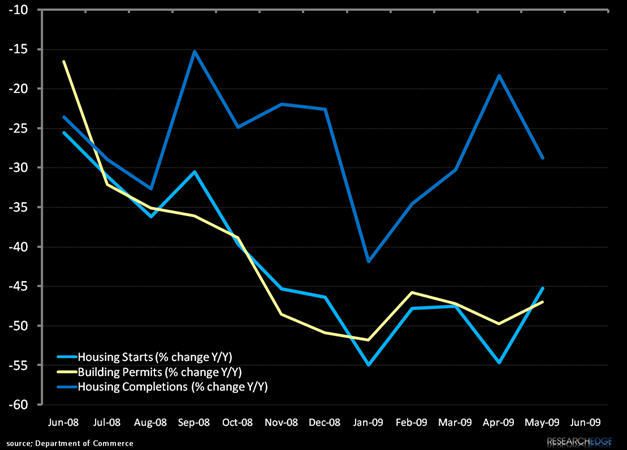

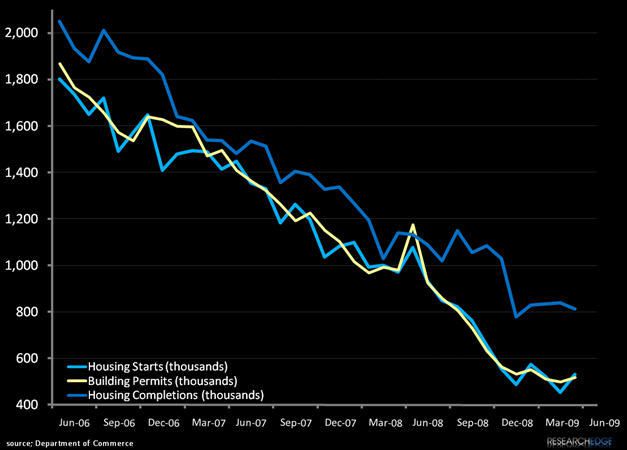

Since the end of Q408, our call on housing has been that it would bottom in 2Q and today's news provides further validation for our thesis. The 17% month-over-month increase in housing starts to an annual rate of 532,000 followed a 454,000 number last month, handily beating both consensus and our expectations. Last month we described the housing start numbers as an industry "acting rationally". This month's number is not strong enough to indicate that home builders are acting irrationally, but one has to wonder if the demand is really improving.

The divergence between starts and completions has narrowed by 35% from the high in November of last year -but at 280 thousand units the potential inventory overhang is still both significant and ominous.

While government tax incentives are helping to bring in first time buyers, the bulk of the benefit is in the rear view mirror. Last week average 30-year fixed mortgages jumped 30 basis points to 5.6% percent, (the highest since November 26, 2008) which suggests that the trends could slow as we head into the summer. At 5.6%, mortgage rates are 75 basis points higher since April, when the rates were 4.8%. Meanwhile, the Mortgage Bankers Association said total mortgage applications fell 7.2% last week.

With unemployment at a 25 year high and likely headed higher more consumers are likely to hold off on purchases of big ticket items and the savings rate is on the rise. The housing market has bottomed for now, that is for sure. The next move on the margin is less clear, as there is enough cold water to throw on an accelerating rate of improvements.

Howard W. Penney

Managing Director