I’d like to have some of what Steve Wynn was eating during the conference call last night.

WYNN served up a tasty quarter and whet our appetites with hints of an impactful upcoming Board meeting. A smorgasbord of issues will likely be discussed at the meeting including a special dividend, whether to pull out of the MA and PA bidding, and potentially moving corporate headquarters to Asia (just our guess).

WYNN’s long-term prospects in Asia are delicious: Potential new menus in Japan, Taiwan, and South Korea, and the Cotai project that could open before Chinese New Year in 2016. Moreover, WYNN also announced a Phase II in Cotai. Over the near-term, Wynn Macau is finally hungry for potential market share gains in the Mass market. While the overall continued strength of Macau was discussed, management’s recent aggressive push into the Mass business was not.

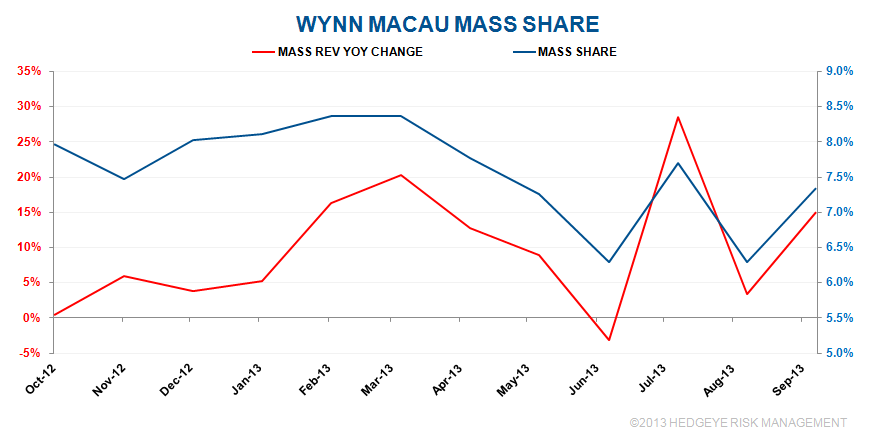

We think Wynn Macau will be more aggressive promoting its Mass business, something it really hasn’t done. Macau management was enhanced recently with some Mass focused personnel. Consistent market share losses have been a key tenant of the WYNN bear thesis. Any reversal will likely be rewarded by investors. As can be seen in the following chart, September produced a Mass revival for Wynn Macau. Our sources indicate that the property should show further gains in October and likely for the rest of the year.