UA might have a couple tough margin qtrs ahead of it. The good news is that its finally making progress outside the US.

UA is a great company that is coming into its own, but it may face a couple of tough margin quarters ahead. UA is one of the most expensive names in consumer, and we can find other stocks with higher quality growth at a lower price.

Given how hated UA's stock is (see our sentiment monitor in Exhibit 1) we suspected that material revenue beat followed by a better print on the EPS line would be enough to give this stock a shot in the arm.

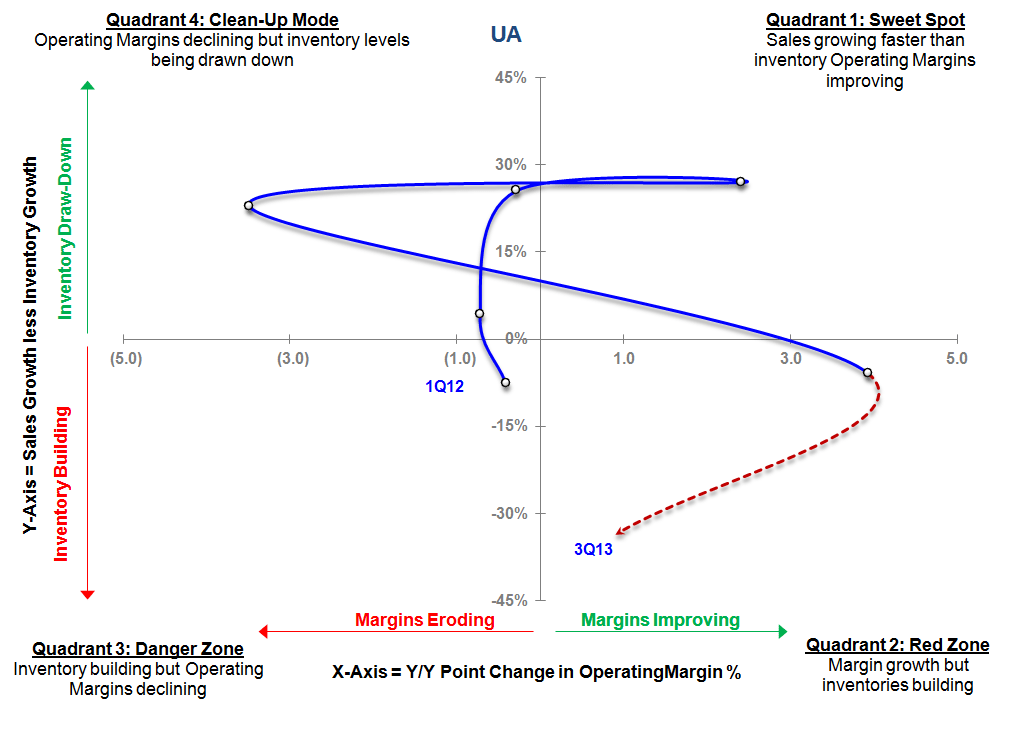

But then we flipped over to the balance sheet and a 59% boost in inventories (despite only a 25.7% boost in sales), and juxtaposed that against the -33bp erosion in Gross Margins in the quarter. Any way we slice the onion, bloated inventories and weakening gross margins hardly inspires confidence in any financial model. In fact it is almost always a precursor to additional gross margin weakness.

WHEN A BRANDS LINE SWINGS DOWN AND FLIRTS WITH THE LOWER RIGHT QUADRANT, IT'S NEVER GOOD

Also, footwear sales were up 28% in the quarter. Don't get us wrong -- that's a great number for most brands. This isn't most brands -- it's UnderArmour. A few years ago when the footwear product used to -- well…stink -- we'd expect sub par growth. But the brand has finally figured out its identity and has put out product that consumers actually want to wear -- -both men and women. But does this add up to 28% growth? We'd think something greater -- perhaps even 2x (at least if it wants to maintain a 48x forward multiple.)

Let's put that multiple into perspective for a minute… UA is expensive -- period. But some of the best stocks in the market are expensive (and some of the worst stocks are cheap). We're not a fan of PE/Growth multiples. But when looked at alongside other high growth peers it certainly puts things into perspective we can get a good sense as to relative value. SO let's do that…lets compare UA against a who's who of high-flying consumer growth names. We're talking everything from TSLA, CMG, AMZN, UA, NFLX, KORS, NKE, WWW, RL, FNP, FNP and RH. Unfortunately for UA, it tips the scale along with TSLA, AMZN and NFLIX at 2.0x PEG. As an aside, our favorite name is RH -- the cheapest name on the page.

There were definitely some things we liked this quarter, and those focused on the areas where UA has been damaged goods in the past -- The biggest of those is International where It just opened up a huge Brands experience store in Shanghai, which is a great idea no matter how you slice it. For the first time in…well, ever…it looks like UA can get 10% of its sales outside of these United States. That would be a big valuation kicker for US, because there's a fair sized contingent that thinks UA is forever rooted in the US. We disagree, by the way. Secondly, womens continues to outpace the company's overall growth rate, and now accounts for about 30% of total revenues. To put that into perspective, Nike announced last week that it's targeting its women's business to account for 24% of revenues by 2018. UA, already has a well established women's product, and if womens were to account for nearly half of the business in the years to come as company management indicated that could be a serious growth opportunity.