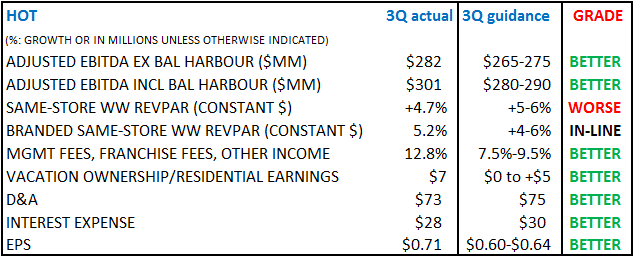

Please see the tables rating HOT’s Q3 performance and Q4 guidance below. The release was typical HOT: great quarter but low ball guidance for Q4. We won’t review the whole quarter but here are some takeaways:

OVERALL HOT THESIS

- We like the branded hotel business long-term – high ROIC, brands are underpenetrated overseas, asset light model, growth funded locally and not on HOT’s balance sheet

- The transactions market really heated up in Q3 – see our Transactions note from 10/11/13 – both in terms of price per key and number of transactions

- HOT should be more aggressive in selling assets next year

- HOT should be returning more cash to shareholders as it moves closer (but not all the way) to the MAR model. HOT raised its dividend, moved to quarterly dividend, and bought back a lot of stock (see chart below)

- Company can lever up by at least a turn without jeopardizing credit rating

- HOT’s European exposure is now a tailwind in our opinion and is likely contributing to HOT’s solid 2014 RevPAR guidance of 5-7% growth. Our research in Europe indicates higher consumer activity. The Hedgeye Macro Team is also bullish on the margin on the European consumer. HOT generates the highest % of EBITDA from Europe of the branded US hotel companies.

3Q TAKEAWAYS

- Non-room revenue consistently improving each of the last 3 quarters

- CostPAR only increasing at a rate of 0.7x of RevPOR the last 2 Qs.

- Fee growth was very good at 13% but 3% of that was termination fees

- Owned margins were better but VOI margins were weaker than expected

- Excluded one-time items were actually gains and usually are - unlike casino companies that only seem to exclude bad stuff

- Consistent with recent trend, Revpar gains are in direct order of price point – sadly, this is economic reality these days

- Looks like only a half of a turn of leverage – this is ridiculously low, especially with likely more aggressive asset sales upcoming. Leverage levels for Lodgers are near all-time lows.

- Solid 2014 revpar guidance of 5-7% - likely better than expected

- We expect them to be positive on the margin regarding Europe on the call