In an effort to evaluate performance and as a follow up to our YouTube, we compare how the quarter measured up to previous management commentary and guidance

OVERALL

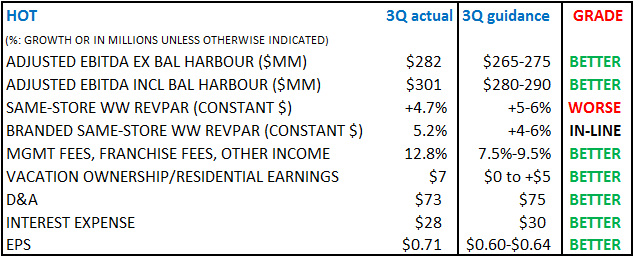

- BETTER: HOT delivers a beat driven by better margins on their owned & leased business and stronger fees growth. Buybacks and the steady quarterly dividend were also a bonus although not a surprise.

EUROPE

- SLIGHTLY BETTER: Absence of new supply has allowed occupancies to reach record levels and keep RevPAR steady in the 2-3% range. Mgmt expects that to continue. They had a good summer in Spain and strenght in Eastern Europe. They are optimistic regarding 2014.

- PREVIOUSLY:

- Turning to Europe, the economic picture is still anemic overall. But as before though, our business is holding up pretty well. We attribute this to tight supply and our ability to bring in global suppliers to Europe – global travelers to Europe with SPG, and our global sales team.

- Europe is steady but sluggish, as it has been for the past couple of years.

- We expect this 2% to 3% growth rate to continue into Q3 as leisure travel looks good for the summer and we may benefit from Ramadan ending earlier in August.

BAL HARBOUR

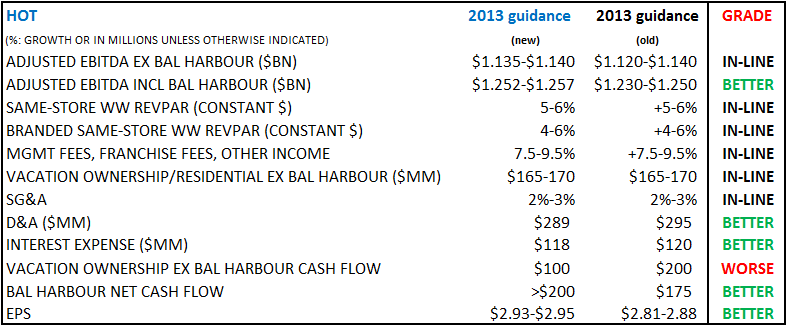

- BETTER: EBITDA of $19MM was ahead of 3Q guidance and HOT raised its 2013 net cash flow forecast to over $200MM from $175MM previously.

- PREVIOUSLY: At the end of the quarter, we only had 22 condos left to sell or close. We have been raising prices and recent square footage rates have exceeded $1,500. Unfortunately, this gift will stop giving by the end of the year since we will be sold out. We are raising Bal Harbour profit expectations by $20 million to $110 million, and cash flow to at least $175 million

RETURN OF CASH TO SHAREHOLDERS

- BETTER: HOT repurchased approximately 2.73MM shares for $180.7MM. Subsequent to the end of the quarter and through October 18, 2013, HOT repurchased an additional 1.14MM shares for $75.9MM. In addition, HOT's Board of Directors has an annual cash dividend of $1.35. There will be quarterly dividends starting in 2014.

- PREVIOUSLY: We will also discuss moving to a quarterly dividend starting in 2014. Stock buybacks remain a priority.

US

- SAME: North American RevPAR came in at 5.8% in 4Q, driven by strong transient revenues (up 8-9%), leisure travel and corporate demand

- PREVIOUSLY: North American REVPAR has been growing at about 6% through the first half and we are projecting that this will continue with rate accounting for 80% of the increase.

GROUP BOOKINGS

- SAME: Group pace remains in the mid-single digits and expect rate increases in the high to mid-single digits

- PREVIOUSLY: Group pace for 2014 and 2015 is currently tracking in the mid-single digits.

TRANSIENT

- SAME: Transient revenues were up 8-9% in the quarter

- PREVIOUSLY: Transient demand, especially corporate travel has remained robust. Helped by record low supply, occupancies hit new peaks.

MIDDLE EAST/AFRICA

- SAME: RevPAR declined to under 1% this Q. Owning to political turmoil, Egpyt and Syria dragged down performance. UAE had a good quarter.

- PREVIOUSLY: Middle East: We expect growth rates in Q3 to tick down in this region for a couple of reasons. Egypt, which was recovering nicely, is impacted by the recent turmoil and Saudi Visa restrictions are sharply reducing Ramadan-related travel. Things are expected to recover as we enter Q4.

LATIN AMERICA

- WORSE: REVPAR only grew 1%, below previous expectations. Strength in Mexico was not enough to offset weakness in Brazil.

- PREVIOUSLY:

- With the crisis in Argentina and now a slowdown in Brazil, Latin America has struggled this year. Brazil was down 6% in the quarter, but by the demonstrations, a slowing economy and the impact of major renovations at the Sheraton Rio, which remains in the same store set. Mexico is helping mitigate some of this as it grows from increasing business activity as well as the return of the American vacationer.

- As we enter Q3, we lap 16% declines in Argentina last year, so we might actually see Latin American REVPAR grow 5% to 6%.

CHINA

- WORSE: Mgmt is disappointed with results. Assume that RevPAR growth will be in the 2% range in 4Q.

- PREVIOUSLY:

- In China, REVPAR growth continues to track well below the expectations we had at the start of the year.

- As we enter the second half, we begin to lap the slowdown in China last year. As such, we expect REVPAR growth will pick up a bit to the 2% to 4% range.